- What Does a Payment Gateway Company Do?

- Business Models for Gateway Companies

- Market Research: Understanding Your Ideal Merchant Base

- Compliance & Licensing Requirements

- Building the Foundation: Essential Departments & Teams

- Partnerships Required to Launch a Payment Gateway Company

- Technology Options for Launching a Payment Gateway Company

- Go-to-Market Strategy for a New Payment Gateway Company

- Scaling Your Payment Gateway Company

- Common Mistakes New Payment Gateway Companies Make

- Conclusion

- FAQ

The global shift toward digital payments continues to open new opportunities for payment entrepreneurs, PSP startups, PayFacs, ISOs/MSPs, and fintech founders that want to launch merchant-facing infrastructure under their own brand. Merchants now expect localized payment methods, multi-provider coverage, A2A options, wallets, and faster onboarding, which creates demand for gateway businesses that can offer control, customization, speed, and performance.

The barriers to launching a gateway infrastructure have never been lower if you take the right path. Founders often take “let’s build our own payment gateway” at face value and end up locked in development for months, burning budget and runway without any guarantee that the solution will actually be deployed. Many forward-thinking PSP startups choose white-label payment gateway solutions like Akurateco, which offer the shortest path to launching a gateway with enhanced customization, advanced tools, and support.

This article walks you through the business and operational aspects of starting a payment gateway, explaining essentials such as compliance, business model, technology, partnerships, and the strategic steps you need to take along the way.

What Does a Payment Gateway Company Do?

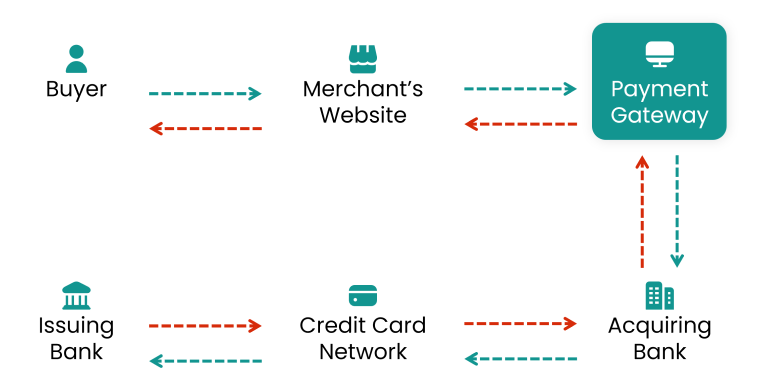

A payment gateway company serves as a commercial and operational engine behind online transactions. It delivers the technology that allows merchants to accept payments efficiently and securely.

A gateway operates as a central component of the payment processing workflow. The company offering this technology delivers the infrastructure that moves payment data between customers, merchants, acquiring banks, and processors, ensuring that every transaction is verified, encrypted, and transmitted in accordance with industry standards.

From a business perspective, creating a payment gateway means operating as the intermediary that connects payment methods (cards, wallets, A2A, alternative methods) to the merchant’s processing partners. It manages authorization flows, supports settlement processes, and handles merchant onboarding.

Beyond transaction handling, a gateway company also offers the tools its merchant clients need to operate more efficiently. This includes settlement reporting dashboards with real-time analytics, transaction routing logic to improve approvals and reduce fees, and built-in compliance and risk controls for dispute management and settlement visibility.

If you start a payment gateway business, you can earn revenue in the following ways:

- Per-transaction fee — a markup applied to each processed transaction, which is the most common and predictable revenue source for payment gateway companies.

- Subscription — a monthly or annual charge for access to the payment gateway infrastructure.

- Volume-based pricing — tiered pricing that scales with the merchant’s processing volume.

- Value-added services — receiving fees for using premium features that differentiate you on the market, such as fraud prevention tools, smart routing, network tokenization, encryption, etc.

Business Models for Gateway Companies

A payment gateway startup can adopt several business models based on different monetization strategies, operational scope, and the extent to which the company wants to participate in the payment lifecycle. Let’s explore each, highlighting its pros and cons.

Model 1: Full PSP / Payment Gateway Company

In this model, you build a full service for merchants that includes both gateway technology and the PSP layer (processing and settlement).

Pros:

- Full ownership of the payment stack

- Highest revenue potential across processing fees, FX margins, value-added services, and settlements

- Strong competitive positioning with full control over performance and merchant experience

- End-to-end merchant management, including onboarding, risk, authorization flows, and payouts

Cons:

- High development and maintenance costs if built internally

- Requires licensing, depending on the country of operation

- Heavier compliance burden, including PCI DSS

- Higher operational complexity, requiring multiple specialized teams

- Longer time-to-market owing to the prolonged development timelines

Building an in-house gateway is typically only chosen by organizations with extremely high transaction volumes and a strong, unique need for complete control over every detail of the payment flow, and who are willing to accept the high cost and risk of managing PCI compliance.

Model 2: Gateway-as-a-Service Company

You offer gateway infrastructure but don’t process funds, while merchants connect their own PSPs, acquirers, and APMs.

Pros:

- Faster time-to-market thanks to already built software by an expert team

- No financial licensing required, since you don’t handle or settle funds

- Immediate access to multiple integrations and connections

- White-label branding and customization options

- Lower operational overhead compared to full PSPs

Cons:

- Revenue potential may be lower, as monetization is focused on software rather than processing fees

- Payment performance depends on the merchant’s PSP partners, not the gateway

- Less control over settlement and payout experience

This model is ideal for financial entrepreneurs who want to quickly tap into the market and open a new payment revenue stream but don’t have the expertise or resources to build and maintain a complex, regulated payment infrastructure.

Model 3: Vertical-Specific Payment Gateway

Instead of operating a general PSP, this model focuses on specialized industries and their unique payment needs, including travel, betting, marketplaces, and subscriptions.

Pros:

- Clear product-market fit, with a solution addressing the exact needs of one domain

- Targeted compliance and risk management

- Stronger differentiation with industry-specific features

- Stronger readiness to invest in specialized capabilities that solve unique business challenges

Cons:

- Requires deep domain expertise to maintain a competitive edge

- Regulatory obligations vary greatly across different countries, depending on the industry

- Market size is narrower, limiting growth potential

If your focus is on a particular niche with its unique payment needs, a vertical-specific payment gateway helps cater to a defined customer base and solve their challenges.

Model 4: SaaS or Platform Adding Its Own Gateway Layer

In this model, a SaaS product or digital platform extends its core offering by adding a payment gateway layer. It basically means that the platform becomes a payments provider, gaining additional revenue while delivering a more integrated experience to its users.

Pros:

- Improved margins as payments become a new source of revenue

- Higher customer retention, since merchants rely on the platform for both payments and software

- Full control over the user experience, from checkout to reporting

- Stronger differentiation with an all-in-one solution

Cons:

- More operational responsibilities, including risk, compliance, and support

- Additional technical complexity, requiring engineering resources

- Financial licensing required

- Significant competition with global payment giants

This model allows existing SaaS and platforms to introduce new payment revenue, increase customer retention, and gain greater control over the user experience without becoming a full PSP.

Market Research: Understanding Your Ideal Merchant Base

Different merchant segments approach payments in their own way. Their risks, typical transaction flows, and day-to-day needs can vary a lot, so they depend on gateways for distinct reasons. As a payment gateway company, you need to understand these differences, which help you decide on features and integrations your payment gateway architecture should focus on first.

Ecommerce

Ecommerce merchants typically look for smooth checkout experiences and a variety of ways for customers to pay. They also care about approval performance and being able to accept international shoppers. Payment gateways help them address these areas by improving conversion, reducing drop-offs, managing fraud risk, and ensuring the system can handle high-volume periods.

Travel and airlines

Travel payments are usually large in value, often cross-border, and tend to generate more disputes. Because of this complexity, plus additional 3DS and SCA requirements, merchants in this niche rely heavily on gateways that enable them to reduce international declines, manage fraud exposure, support multiple currencies, and diversify processing through several PSPs.

High-risk verticals

As a rule, high-risk industries face higher fraud and chargeback rates, stricter underwriting, and fewer willing acquirers due to the essence of the industry, which carries additional operational, financial, and compliance risks for banks and PSPs. Because of these challenges, many operators seek high risk payment processing companies to use payment gateways to reach specialized PSPs, manage risk more effectively, handle disputes faster, and stay aligned with compliance requirements while still keeping their approval rates at a workable level.

Marketplaces and platforms

Marketplaces work with many different sellers, split payments, and scheduled payouts. That’s why they rely on payment gateways to onboard sellers (KYB), handle multi-party transactions, manage payout flows, and give both buyers and sellers clear, consolidated reporting.

Subscription businesses

Subscription businesses focus heavily on keeping customers over time. That’s why they need robust technology for recurring billing, tokenization, and reliable retry flows. Many companies use payment gateways to store customer details securely, help recover failed renewals, manage subscription updates, and make daily billing tasks easier to keep under control.

Digital banks/fintech apps

Fintech companies handle sensitive information every day, so their payment operations need to be extremely secure and stable. For them, payment gateways are core components that support their flows. This includes processing transactions, verifying identities, and making quick authorization decisions across different payment rails.

Compliance & Licensing Requirements

When exploring how to start a payment gateway company, you need to understand the core foundations for any gateway startup: compliance and licensing. In practice, they define the regulatory framework within which your company can operate and are necessary to launch and maintain a functional gateway in the market you target.

Let’s examine the fundamental payment gateway licensing requirements that are strategically important for launching and operating a gateway business.

PCI DSS

PCI DSS is the primary requirement for any company that stores, processes, or transmits cardholder data. Typically, the level of responsibility depends on the gateway architecture.

But there’s a nuance many new founders miss. Even if you rely on third-party providers, you still must comply with the appropriate PCI level and ensure the flow stays outside your environment. For the majority of startups, obtaining this certification means taking on significant time and resource commitments.

Local regulations

Whether you’re operating in the EU, GCC, LATAM, or Africa, each has its own local regulations a payment business must adhere to. Depending on the target region, you’ll need to understand how government officials define payment services and what requirements apply. Getting this right early helps you choose the fastest way into the market, shape your commercial approach, pick the right tech setup, and avoid unnecessary risks or costs.

Contracts with acquiring banks and PSPs

You can’t operate as a payment gateway without establishing legal partnerships with your acquiring banks and PSPs. The one fact that you need to realize is that it’s the fundamental requirement for processing transactions, supporting multiple payment methods, or giving merchants access to the providers they need.

AML/KYC expectations

When onboarding merchants, you are responsible for applying AML/KYC checks to confirm who the merchant is and whether their activity is legitimate. This is often a requirement from banking partners and helps prevent fraud, chargebacks, and regulatory issues later.

Due to numerous challenges in payment gateway development, primarily around licensing and compliance nuances, new payment gateway companies decide to take a smarter, more efficient path.

To accelerate time-to-market and reduce regulatory complexity, many startups rely on support models such as:

- White-label payment gateway platforms, which allow businesses to avoid building the entire infrastructure and logic from scratch, as well as eliminating the need to obtain PCI compliance.

- Outsourced PCI or compliance certification, where a specialized firm manages your PCI DSS audit and documentation if your business model requires certification.

- Compliance-as-a-service providers that take over ongoing operational tasks, such as merchant onboarding, AML checks, transaction monitoring, and regulatory reporting.

Each approach simplifies the launch of a payment gateway for founders. As a result, founders can focus on going live and merchant acquisition.

Building the Foundation: Essential Departments & Teams

If you are exploring how to start a payment gateway company, it’s important to understand what actually happens behind the scenes. In most early-stage setups, this comes down to building a small but capable team that can cover the fundamental processes.

Compliance & Risk (2-4 people)

This group manages your regulatory obligations and keeps merchant activity under control. In practice, they handle licensing issues, review AML/KYC documents, and monitor risk on an ongoing basis.

Technology & Product (6-12 people)

This team drives the payment gateway development and evolution of your payment gateway. They coordinate product updates, support new integrations, and ensure the platform remains reliable as volume increases.

Customer Support & Merchant Operations (2-5 people)

These are the people who stay close to your merchants day to day. They answer questions, solve operational issues, and help keep transaction flows running smoothly.

Sales & Partnerships (2-6 people)

This function focuses on bringing new merchants on board and building relationships with PSPs, acquirers, and APMs. Their work shapes your commercial pipeline and partner network.

Finance & Settlement Operations (1-3 people)

The finance team oversees reconciliation, invoicing, and settlement-related checks. In simple terms, they work to ensure money movement and reporting remain accurate and timely.

Account Management (1-3 people)

Once merchants go live, this team looks after them. They help optimize performance, support feature adoption, and work to maintain long-term relationships and retention.

Marketing (1-3 people)

This team becomes the voice of your brand in the market. Through thought leadership, targeted campaigns, and SEO-focused marketing, they position the company as a trusted authority and continuously attract qualified prospects that need the business’s payment solutions.

Partnerships Required to Launch a Payment Gateway Company

A payment gateway can’t function in isolation. In fact, a gateway succeeds by offering breadth. To operate effectively, you need to secure relationships with several key players across the payments landscape:

- Acquiring banks, which authorize and settle card transactions.

- PSPs, giving your merchants access to additional processing routes and geographies.

- Local APMs and digital wallets, needed to support region-specific payment habits.

- Fraud prevention providers, to strengthen security and reduce operational risk.

- KYC/KYB vendors, who help you verify merchants during onboarding.

- BIN sponsors (if required by your business model), enabling you to issue or tokenize cards.

- Infrastructure providers such as AWS, Azure, or Oracle Cloud, which host your platform and support uptime.

It’s an entire ecosystem of partners that makes a payment gateway work. No single provider can realistically build every payment method, integration, or fraud tool in-house without slowing growth or increasing cost.

This brings us to a key point: a modern gateway creates value by giving merchants options in payment routes, methods, and ways to optimize performance. In the long run, this allows you to expand coverage quickly, support different merchant segments, reduce costs, and stay competitive.

Technology Options for Launching a Payment Gateway Company

When exploring how to start a payment gateway company, you ultimately choose among three technology paths: in-house building, a white-label payment gateway, and a hybrid approach. Each comes with different levels of control, cost, and speed to market. Let’s take a closer look at each.

Option 1 — Build a custom gateway (longest, most expensive)

There are multiple business implications that come with payment gateway development. The first is the payment gateway cost and time. An average setup usually takes up to a year and requires an initial investment of $500,000, while a more advanced system can cost up to $1M and take years of development.

That’s why it’s typically chosen only by companies with very high volumes, unique requirements, or the need for control and proprietary processing logic. For most early-stage PSPs and startups, the time-to-market and cost barriers are difficult to justify.

Option 2 — White-label payment gateway solution

With a white-label payment gateway, startups take the shortest path to launch. Basically, in a few weeks, compared to in-house building. The infrastructure, security layers, PCI DSS compliance, and dozens of integrations are already built and maintained by the vendor. What this really means is that founders can focus immediately on merchant acquisition, partnerships, support, pricing, and operations.

Given these advantages, a white-label gateway is the most common approach for PSP startups, SaaS platforms adding payments, regional providers, and entrepreneurs who want to open a gateway business quickly with minimal upfront cost.

Option 3 — Hybrid approach

Many modern PSPs adopt a hybrid strategy: launch using a white-label solution, validate demand, build revenue, and then gradually extend the platform with proprietary modules where differentiation is needed.

In practice, this approach offers a combination of the two previous variants. It includes rapid market entry and the option to evolve into a more customized or partially in-house stack over time. Importantly, it also reduces risk by ensuring the business model is validated before major engineering investments are made.

Launching a payment gateway startup allows you to tap into the growing payments industry. However, developing your own solution can cost you time and financial resources you didn’t anticipate.

To ensure a secure, efficient launch that stands out in the market, choosing a white-label gateway is often the most strategic move for teams that need fast go-live, predictable costs, and a competitive product from day one.

Go-to-Market Strategy for a New Payment Gateway Company

Launching a payment gateway is only half the story. You need a sustainable flow of clients to make your business successful. Winning merchants requires a targeted strategy. What you need to understand is that early-stage payment businesses operate most successfully when they plan their marketing carefully.

Here are recommendations that can help a new payment gateway company shape an effective go-to-market strategy.

Define your ICP (Ideal Customer Profile)

You can’t build a compelling offer without knowing what your customer is trying to fix. Picture your ideal client, their day-to-day workflow, and the things that slow them down. That’s where you find the real triggers for building a gateway that feels right for them.

In practice, this means mapping out their payment flows, understanding where they lose revenue today, and identifying which integrations, onboarding experience, or approval-rate improvements would deliver the fastest, clearest wins.

Target high-value verticals first

Payment gateway startup teams should prioritize verticals with high processing volume and unavoidable payment complexity. The reason for this is that they already struggle with several challenges they can’t deny: multi-PSP setups, cross-border flows, recurring billing, and elevated dispute rates.

A new gateway can easily serve digital goods, marketplaces, subscriptions, travel, or even financial apps. These sectors move fast, so when they see a tool that helps them solve real payment friction, they’re usually among the first to try it.

Choose local-first or global-first expansion

Your early market focus, whether local or worldwide, shapes which integrations and partners you need:

- Local-first works best if you specialize in one geography or regulatory zone (EU, GCC, LATAM).

- Global-first fits gateways focused on cross-border commerce, currency diversity, and PSP aggregation.

It’s best to decide based on how fast you want to go live and which partners you can secure.

Design a commercial routing strategy

There are reasons why transactions take the specific route. Commercial routing strategy is the logic that drives it. In practice, it’s an area you need to design intentionally, based on a deep understanding of your merchants’ needs and processing patterns.

When researched and done well, it helps unlock cost savings, higher approvals, PSP failover, broader coverage, and new payment methods. In many cases, this becomes a core part of your pitch, especially for merchants frustrated with single-PSP limitations.

Focus on the features merchants expect in year one

Merchants evaluating a newly launched gateway look for these four non-negotiables:

- Fast onboarding (KYC/KYB and technical)

- Strong dashboards and reporting

- Smart routing and multiple PSP options

- Reliable settlement visibility and transaction monitoring

If any of these are missing, sales cycles drag on.

Differentiate where it actually matters

It’s true that the fintech industry offers opportunities for startups, but it also faces significant competition. What it actually empowers new gateways to do is think differently and win by focusing on experience. Put simply, your differentiation should center around:

- Speed across onboarding, integration, and deployment.

- Wide coverage with access to various PSPs, APMs, currencies, and regions.

- Operational efficiency with automation, risk tools, and alerting.

- Commercial transparency by offering pricing models that merchants actually understand.

- Data clarity through dashboards, reconciliation, and dispute-handling visibility.

In short, smart market positioning is what moves you from “another PSP” to a platform merchants rely on for daily operations.

Scaling Your Payment Gateway Company

Once your payment gateway is live and supporting its first merchants, the next step is scaling. As your clients grow, their expectations evolve. Over time, they’ll ask for stronger performance, faster transactions, broader coverage, and more sophisticated tools.

Focusing on these core areas will position your gateway to meet growing payment demands, strengthen performance, and scale far more efficiently.

Expand geographic coverage (PSPs / acquirers / APMs)

Scaling starts with broadening your processing network. Adding new PSPs, local acquirers, and APMs helps you unlock new markets, increase approval rates, and support merchants with region-specific payment habits.

Add A2A and open banking rails

Account-to-account and open banking payments are becoming mainstream. Introducing these rails strengthens your offer with lower-cost transactions, faster settlements, and regulatory alignment across Europe, GCC, and APAC markets.

Add tokenization and network tokens

As merchants grow, so does their expectation for advanced retention tools. Tokenization and network tokens help reduce friction, boost recurring acceptance rates, and improve security for subscription-heavy verticals.

Introduce risk scoring and automation

A scalable gateway must handle risk without adding manual workload. Automated decisioning, transaction scoring, and real-time monitoring reduce fraud exposure and streamline operations, which is a key differentiator for enterprise merchants.

Grow your merchant base

Growth compounds when you expand your portfolio. Strengthen inbound sales motions, refine onboarding flows, and double down on high lifetime value verticals that experience payment friction the most.

Move to multi-PSP routing to increase approval rates

As volume increases, merchants expect performance. Multi-PSP routing helps optimize costs, reduce declines, and provide redundancy. This is what makes your gateway more resilient and commercially attractive.

Expand into new verticals

Once core verticals are stable, you can extend coverage to segments such as e-learning, mobility, B2B SaaS, iGaming, or cross-border ecommerce. Each segment opens new revenue streams and increases your total addressable market.

Common Mistakes New Payment Gateway Companies Make

When you are just exploring how to start a payment gateway company, you’ll inevitably hit a few bumps along the way. Below are the most common pitfalls early-stage gateway teams run into to avoid from day one:

- Starting with tech instead of partnerships. Many founders begin coding before securing acquirers, PSPs, or APMs. Without partners, even the best gateway cannot process a single transaction.

- Underestimating compliance costs. PCI, licensing, AML/KYC, and banking requirements take more time and budget than you might expect, slowing the launch and draining resources.

- Poor merchant onboarding flows. Long KYC/KYB checks, unclear instructions, or slow integrations eventually result in early churn and lost deals.

- Failing to differentiate in a saturated market. New gateways often come out generic, without a clear go-to-market strategy. It’s actually what causes them to get overshadowed by existing PSPs.

- Hiring developers before product managers. Building without a product roadmap leads to unnecessary features, slow releases, and misalignment with merchant needs.

- No monitoring or visibility tools. Gateways that don’t show clear reporting, alerts, and real-time transaction status quickly lose merchant trust.

- Scaling infrastructure too late. Traffic spikes or expansion to new verticals can quickly uncover gaps if the infrastructure wasn’t sized for growth from day one.

Many of these mistakes happen simply because early teams try to own too much too soon. A strong white-label payment processing foundation removes this overhead and lets founders focus on growing the merchant base, which actually moves the business forward.

Conclusion

Starting a payment gateway company is a lucrative opportunity to tap into the growing market. However, it requires more than it seems. To launch a payment gateway company successfully, designing business, compliance, partnerships, and product strategy is essential. That’s why modern companies choose modular, scalable, cloud-ready setups that provide pre-built infrastructure for fast time-to-market and future-proof growth.

Akurateco’s white-label payment gateway provides access to a PCI-compliant solution with 700+ connectors, smooth merchant onboarding, customization capabilities, reporting, analytics, and other advanced features through a single API integration. As a result, new payment gateway companies go to market faster with compliant, ready-to-scale infrastructure.

FAQ

How much does it cost to start a payment gateway company?

The cost varies widely based on the approach. A fully custom-built gateway typically requires from $500,000 up to $1M in development. In contrast, a white-label payment gateway can reduce initial costs at least in half, allowing startups to launch quickly without compliance overhead.

Do I need a license to start a payment gateway business?

It depends on your payment gateway startup model. If you process or settle funds, you must obtain local financial licensing (EMI, MSB, MTL, PCI). However, if you operate a technology-only gateway and merchants bring their own acquirers, licensing is typically not required, though PCI compliance still applies.

How long does it take to launch a payment gateway company?

It takes 12-24 months to start a payment gateway business, depending on the complexity of routing, reporting, and integrations. On the other hand, with a white-label solution, companies typically launch in several weeks, depending on the integrations and setup they want.

Do payment gateway companies need their own acquiring bank?

Not necessarily. Many gateways operate via merchant-provided PSPs and acquirers, simply facilitating transactions between them. However, gateways that act as full PSPs or provide settlements must secure acquiring partnerships and, in many regions, licensing.

Can a startup launch a payment gateway using a white-label solution?

Absolutely. It’s now the most common and efficient path to start a payment gateway. White-label platforms allow startups to launch quickly, meet PCI compliance requirements, access dozens of integrations instantly, and focus on sales, partnerships, and operations rather than multiyear engineering work.