- Key Points to Know Before Starting a Payment Processing Company

- Why Start a Payment Processing Company?

- How to Start a Payment Processing Company: Step-by-Step

- Build vs. White-Label: Payment Processing Infrastructure Options

- Optimizing Payment Processes for Efficiency and ROI

- How much does it cost to start a payment processing company?

Last updated: June 2026

In today’s digital economy, payment processing has become a major opportunity for PSP founders, PayFacs, ISOs/MSPs, fintech teams, and entrepreneurs that want to help merchants accept online payments under their own brand.

Starting a payment processing company is not just about processing card transactions. It requires a clear business model, reliable payment infrastructure, acquiring or banking relationships, compliance readiness, merchant onboarding processes, fraud prevention, and a plan for scaling transaction volume.

In this guide, we explain how to start a payment processing company in 2026, including the key business models, required partnerships, compliance steps, technology options, startup costs, and launch process.

Key Points to Know Before Starting a Payment Processing Company

Before you start credit card processing for businesses, you need to know the basics of this industry, the key players, and the roles they perform.

What is a credit card processing business?

A credit card processing business facilitates transactions between merchants and their customers by processing digital credit or debit cards. Simply put, credit card processors provide merchants with a technical layer to accept card payments on their websites.

Their essential functions include:

- Verifying whether a card is valid and has enough credit for the transaction.

- Facilitating the transfer of funds from the customer’s bank to the merchant’s account after processing the transaction successfully.

- Implementing fraud prevention measures to protect sensitive cardholder data.

- Providing software and infrastructure for merchants to process card transactions through their websites or applications securely.

- Offering hardware and software solutions for card processing, which is why some entrepreneurs also research this market as a credit card machine business or a credit card terminal business.

What is a payment processing company?

A payment processing company can provide credit card processing within its operations. However, it is not limited to card transactions. Payment processing companies handle all forms of digital transactions to enable businesses to accept payments from their customers, including credit and debit cards, electronic funds transfers (EFTs), e-wallets, Buy Now Pay Later (BNPL), cryptocurrencies, etc.

If you’re considering entering the fintech market, understanding the role of these companies is essential for anyone exploring how to create a payment processing company that can compete on a global scale.

What is a payment service provider?

With such a variety of key players in the digital payments field, here’s where it gets tricky.

Payment Service Provider (PSP) offers payment services for facilitating digital payments between businesses and customers. PSPs provide their clients with various services, including payment processing itself and advanced technologies for improving transaction approval rates and minimizing declines.

What is a payment facilitator?

Another major player in the digital payments arena is a Payment Facilitator, also called PayFac. PayFac is a type of financial service provider that simplifies the process of accepting electronic payments for smaller businesses. Previously, the main task of PayFacs was to enable companies to quickly set up and start accepting payments without the need for a traditional merchant account that involves more complex underwriting and approval processes. However, PayFacs have evolved over time to meet the diverse needs of merchants, now providing a comprehensive range of services to enhance the overall payment experience. Learn more about PayFacs in our comprehensive guide.

What is a merchant processing company?

A merchant processing company specializes in providing payment processing services to merchants. It is often called MSP. MSPs and PSPs are related terms in the payment processing industry, but they refer to different types of entities with distinct roles and focuses. MSPs work directly with merchants to set up and manage merchant accounts, acting as middlemen between businesses and acquiring banks.

How does a payment processor work?

Being responsible for managing transaction processing, the payment processor holds a pivotal role within the electronic payment ecosystem. Here’s how a payment processor works.

When a customer makes a purchase, they enter their payment information. Then, the merchant’s payment system receives it and sends an authorization request to the payment processor. In turn, the payment processor processes the authorization request, verifying the customer’s sensitive information. Once verified, transaction details are sent by the processor to the issuing bank to check the customer’s account for sufficient funds and fraud alerts. If the issuing bank approves the transaction, it sends approval back to the payment processor. Lastly, the payment processor sends it to the merchant’s system. After that, the transaction is finally authorized.

Knowing these inner mechanics is crucial for those planning to get into the credit card processing business, as it forms the foundation of technical and financial operations.

Why Start a Payment Processing Company?

Now that you know the fundamentals of the key players in the digital payments arena, let’s look at how to start a credit card processing business and why companies enter this market.

As per the 2022 McKinsey Global Payments Report, electronic transactions saw a remarkable 19 percent growth rate in 2021, which indicates that the need for reliable payment processing solutions also continues to rise, making the time just about right to learn how to start a credit card company.

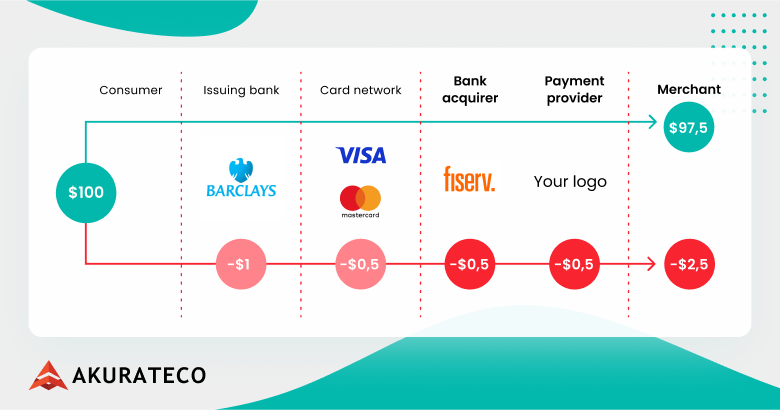

The second major factor is revenue consistency. Merchants rely on payment processors to accept payments from clients. Consequently, credit card processing business benefits from the recurring nature of their revenue streams, driven by transaction fees, monthly charges, and value-added services.

Here’s how credit card processors earn their revenue on transaction fees:

Profit potential is another good reason to start a credit card processing company. Payment processing companies can charge their clients not only for transaction processing but also for value-added offerings, such as white-label payment solutions, new integrations with new banks and payment providers, assistance with Payment Card Industry Data Security Standards (PCI DSS) certification, etc.

Lastly, credit card processors can quickly expand globally. Credit card processing for businesses allows a company to participate in cross-border transactions and attract business overseas.

If you are wondering how to become a credit card processor by now, let’s take a look at the options you have.

How to Start a Payment Processing Company: Step-by-Step

Starting a payment processing company requires more than choosing software. You need to define your market, understand regulatory requirements, build partnerships, prepare payment infrastructure, and create operational processes for onboarding and supporting merchants.

Step 1. Research the market and choose your niche

Start by analyzing the payment processing market, target regions, merchant segments, and industries you want to serve. Decide whether your company will focus on e-commerce merchants, high-risk industries, SaaS platforms, marketplaces, local businesses, cross-border payments, or another niche.

Step 2. Define your business model

Choose how your payment processing company will make money. Common revenue streams include transaction fees, monthly account fees, setup fees, gateway fees, fraud prevention services, merchant management tools, routing features, and other value-added services.

Step 3. Choose your operating model

Decide whether you want to operate as a PSP, PayFac, ISO/MSP, merchant services provider, or payment technology provider. This choice affects your licensing requirements, partnerships, risk responsibility, merchant onboarding process, and technical setup.

Step 4. Prepare your legal and compliance framework

Choose a legal structure, define your target jurisdictions, and research applicable payment processing regulations. Depending on your business model and markets, you may need licensing, bank sponsorship, PCI DSS compliance, AML/KYC processes, data protection policies, and risk management procedures.

Step 5. Build acquiring, banking, and provider relationships

Payment processing companies need reliable relationships with acquiring banks, payment providers, card networks, technology partners, compliance vendors, and fraud prevention providers. These partnerships determine which payment methods, currencies, regions, and merchant categories your business can support.

Step 6. Choose your payment infrastructure

Decide whether to build payment software from scratch or use white-label payment infrastructure. Your technology stack should support transaction processing, payment gateway functionality, merchant onboarding, routing, cascading, reporting, fraud prevention, reconciliation, and scalability.

Step 7. Set up merchant onboarding and risk management

Create a structured process for merchant applications, document collection, KYC/KYB checks, AML screening, underwriting, risk scoring, website review, and approval. This helps protect your payment business from fraud, chargebacks, regulatory issues, and unreliable merchants.

Step 8. Test the system before launch

Before going live, test payment flows, provider connections, settlement logic, reporting, fraud rules, routing behavior, merchant dashboards, and support workflows. Make sure your system can handle successful payments, failed payments, refunds, chargebacks, and provider downtime.

Step 9. Launch, monitor, and scale

Once your payment infrastructure, compliance processes, partnerships, and merchant onboarding workflow are ready, you can launch your payment processing company. After launch, monitor approval rates, failed transactions, processing costs, chargebacks, merchant satisfaction, and system performance to improve profitability and scale safely.

Build vs. White-Label: Payment Processing Infrastructure Options

When it comes to how to start a payment processing company, there are two main options. This also applies to those exploring how merchant processing companies are built, since the core choice is usually the same: develop payment software from scratch or use a ready-to-use white-label solution. Let’s examine each in detail.

Building payment software

Creating your payment system offers an unmatched level of flexibility, enabling you to customize it precisely to align with your business’s unique requirements. This approach allows you to gain complete control of your system, craft software that perfectly caters to your merchants’ needs, and ensure scalability for future growth. Yet, constructing your own software relies on three essential pillars: time, money, and expertise.

Developing your own payment system will require lots of resources. Furthermore, the work continues when the system is ready, as ongoing maintenance and improvement demand a significant dedication of resources.

For a thorough insight into the costs associated with developing your own software, dive into our in-depth article.

White label solution

There is a viable alternative to developing your own payment system for starting a payment processing business – a white-label solution. It is a pre-configured customizable payment software that can be branded in your company’s name. It offers significant cost efficiency and a quick setup process, allowing entrepreneurs to start their business operations within a couple of weeks and begin capitalizing on it in no time.

White-label payment solutions can incorporate multiple technologies and integrations, which vary based on the provider. For instance, we at Akurateco offer white-label payment software equipped with cutting-edge technologies and over 300 integrated banks and payment providers via one integration to the platform. Among the supported technologies much needed to operate a payment processing business are:

- Intelligent routing

- Payment cascading

- Payment fraud prevention

- Tokenization

- Built-in payment analytics

- Optimized checkout

.. and more.

For many entrepreneurs launching a payment processing business, a white-label system dramatically reduces time to market and initial capital risk.

To learn more about a white-label payment gateway, check our in-depth guide.

Optimizing Payment Processes for Efficiency and ROI

After launching your credit card processing business, shifting focus toward operational efficiency and long-term profitability is essential. Optimizing payment processes helps reduce costs, improve transaction speed, and enhance the user experience — all of which contribute directly to ROI.

Key strategies include:

- Implementing Intelligent Payment Routing to automatically choose the most cost-effective and reliable acquiring bank based on geography, currency, or risk profile.

- Utilizing automated reconciliation and reporting solutions for reducing manual errors, saving time, and ensuring financial accuracy.

- Using AI-based fraud detection and chargeback management to protect revenue and prevent losses.

- Interpreting payment data to understand customer behavior, optimize conversion rate, and make informed business decisions.

- Ensuring scalability and multi-currency capability for surviving growth and expanding into new geographies without disrupting operations.

- High Revenue Potential: Payment processors stand to gain substantial revenue through transaction fees, setup fees, and value-added services, which together form the foundation of the payment processing business model.

Staying on top of it and streamlining your payment stack will give your business a competitive edge and drive long-term success. Consider ready-made white label payment processing solutions to quickly launch your business by customizing them to fit your brand.

How much does it cost to start a payment processing company?

When searching for how to start a payment processing business, the financial question is significant. Costs can vary greatly when it comes to starting a payment processing company. It depends on several factors, including the scale of your operation, the services you plan to offer, regulatory requirements in your region, technology infrastructure, and others. However, the main cost factor is whether you develop your own software or leverage a white-label system.

In-house payment software

If you decide to develop a payment system on your own, the costs associated with it will include developers’ salaries, technology and infrastructure you’ll build independently, regulatory and compliance costs, security measures, and ongoing system maintenance. On average, moderately complex software with additional features and security measures could cost from $300,000 to $500,000. Yet, a highly advanced and fully customized enterprise payment orchestration platform may cost way over $500,000.

It’s one of the main factors to consider when asking how much does it cost to start a credit card company, especially if customization and proprietary technology are key to your model.

White-label payment software

Alternatively, if you opt for a white-label solution, you’ll get ready-to-use software with licensing fees and customization costs. Generally, the price of a white-label solution customized to meet your specific branding, feature, and integration requirements may vary widely, ranging from $10,000 to $50,000 or more. It’s worth emphasizing that you will generate revenue much faster with a white-label solution since it’s pre-built and ready for use.

Our customers often note that a white-label solution allows them to go to market quickly without sacrificing flexibility. They can adapt the functionality to their business processes and scale the platform as their company grows.

FAQ

What is a payment processing company?

A payment processing company helps businesses accept digital payments from customers. It can process credit and debit cards, bank transfers, e-wallets, BNPL, and other payment methods by connecting merchants with acquiring banks, card networks, issuing banks, payment gateways, and other payment infrastructure providers.

How do I start a payment processing company?

To start a payment processing company, first define your target market, business model, and operating role, such as PSP, PayFac, ISO, or payment technology provider. Then, prepare your legal and compliance framework, build relationships with banks and payment providers, choose your payment infrastructure, set up merchant onboarding and risk management processes, test the system, and launch your services.

How much does it cost to start a payment processing company?

The cost depends on your business model, target markets, licensing needs, technology setup, compliance requirements, and whether you build software from scratch or use white-label payment infrastructure. Building a custom payment system can require hundreds of thousands of dollars, while white-label software can reduce initial costs and help launch faster.

Do you need a license to start a payment processing company?

In many cases, yes, but the exact licensing requirements depend on your country, business model, payment services, and whether you hold funds, onboard merchants, or work through licensed partners. Some companies operate through acquiring banks, sponsors, or licensed payment providers, while others need their own payment institution, money transmitter, or similar license. Legal guidance is strongly recommended before launch.

What is the difference between a payment processor, PSP, PayFac, and ISO?

A payment processor handles the technical movement of transaction data between merchants, banks, card networks, and payment systems. A PSP provides merchants with payment acceptance services, often including multiple payment methods, gateway access, reporting, and risk tools. A PayFac onboards sub-merchants under its own payment structure, while an ISO usually sells or manages merchant services on behalf of acquiring banks or processors.

Can I start a payment processing company with white-label software?

Yes. White-label payment software allows a company to launch payment services under its own brand without building the full payment infrastructure from scratch. This approach can reduce development time, lower upfront technical costs, and give PSPs, fintechs, and payment businesses access to ready-made features such as merchant management, routing, reporting, fraud prevention, and payment integrations.

How do payment processing companies make money?

Payment processing companies usually make money through transaction fees, merchant discount rate markups, setup fees, monthly account fees, gateway fees, chargeback fees, and value-added services. Their revenue often grows with transaction volume, but profitability also depends on processing costs, risk management, infrastructure expenses, provider agreements, and merchant retention.