- What Is Payment Routing?

- Static vs. Dynamic Payment Routing

- How Intelligent Payment Routing Works

- Smart Routing vs. Cascading vs. Failover

- The Main Benefits of Intelligent Payment Routing

- Common Payment Routing Parameters

- Real-life Use Cases: How Akurateco’s Clients Benefit from Smart Payment Routing

- How to Get Started with Intelligent Payment Routing

- To sum up

With almost all goods and services delivered online today, a failed transaction isn’t just a technical hiccup — it’s lost revenue. Every declined payment can cost a business a sale, a customer, and long-term trust.

Intelligent payment routing, also known as smart payment routing, addresses this challenge head-on. By automatically directing each transaction through the optimal payment provider, businesses can boost approval rates, lower transaction costs, and ensure a smoother checkout experience. For merchants evaluating top credit card processing companies, intelligent routing is one of the key capabilities that can directly influence approval rates, processing costs, and overall payment performance.

In this article, we’ll explore what payment routing is, how it works, real-life use cases from our clients, and the opportunities it presents to payment service providers and merchants worldwide.

What Is Payment Routing?

Payment routing is a technology that automatically chooses the most relevant payment provider for each transaction, contributing to the company’s revenue and transaction approval ratio.

With advanced routing parameters, this technology replaced transaction processing prone to delays and declines on the payment processors’ side, internal limitations on certain types of transactions, their amount, blocked countries list, and other factors. It also enables card network optimization and supports multi-acquirer strategy for better authorization rates.

Watch the video below to better understand what intelligent payment routing is, how it works, and what benefits it brings for businesses.

Static vs. Dynamic Payment Routing

There are two main types of payment routing that businesses can rely on: static and dynamic. Let’s take a closer look at each of them.

What is static payment routing?

Static payment routing involves manual configuration of fixed routes. A transaction is always sent to a predetermined payment service provider, regardless of system performance or conditions. If that provider experiences downtime or high latency, transactions fail, leading to lost sales and customer frustration.

What is dynamic payment routing?

Dynamic payment routing uses real-time performance data to automatically choose the best available provider for each transaction. If a provider is down or declines a transaction, the system automatically redirects (cascades) the transaction to another provider within a single payment attempt, maximizing approval rates. This adaptive routing mechanism is key to approval rate increase and cost reduction.

In today’s fast-paced digital economy, dynamic payment routing is a must for businesses looking to optimize every transaction.

How Intelligent Payment Routing Works

Smart payment routing, a type of dynamic routing, allows businesses to manage payment orchestration efficiently via the system’s admin panel. The process begins with evaluating transaction data, such as BIN, currency, and amount, against various databases. Based on pre-set criteria, the system automatically selects the optimal payment provider for each transaction.

Once a customer confirms payment, the multi-step smart routing engine kicks in, identifying the most suitable MID or Acquirer, factoring in cost, location, currency, Application Programming Interface (API) performance, and more. While configurations may vary by provider, the goal remains the same: to maximize approval rates, reduce chargeback risk, and ensure compliance with local and international regulations.

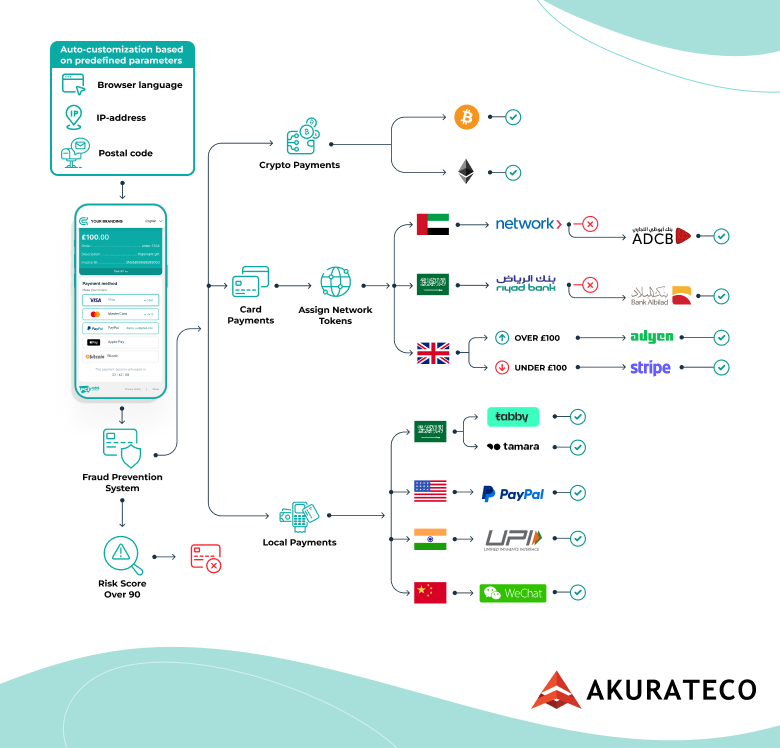

The diagram below shows how payment routing works step by step.

- After the client confirms payment on the website or application, the automated fraud prevention system verifies the payment.

- If the payment is verified, the process of intelligent payment routing determines which payment providers could potentially process this transaction according to the payment method (shown in the image) or another given parameter.

- Based on additional parameters, such as the geolocation of the billing address, transaction amount, or low interchange fee, payment routing identifies the most suitable payment provider to route payment to and directs the transaction there.

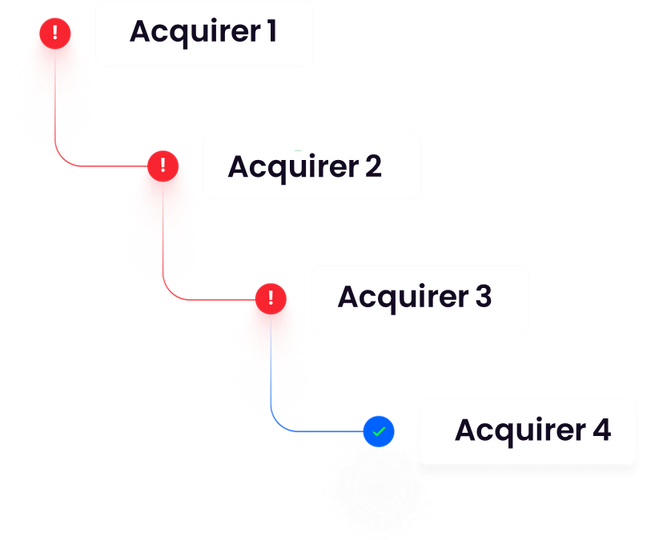

- In case the transaction is declined due to issues on the payment provider’s side, a cascading mechanism activates, redirecting the transaction to another payment provider for processing. This process continues through multiple providers as needed, ensuring a successful payment within a single attempt and contributing to chargeback reduction. Explore routing and cascading in real scenarios.

Smart Routing vs. Cascading vs. Failover

Smart routing, cascading, and failover are related payment optimization concepts, but they do not happen at the same moment in the transaction flow. Smart routing decides where to send a transaction before authorization, cascading retries a declined payment through another provider, and failover keeps payments running when a provider is unavailable.

| Concept | When it fires | Primary goal | Trigger |

|---|---|---|---|

| Smart / Intelligent Routing | Before the transaction is sent | Choose the best provider for each transaction based on approval rate, cost, geography, or other rules | Pre-authorization, rule-based, or ML-based decision |

| Cascading | After a soft decline | Recover a failed payment by retrying it through alternate providers | Soft decline returned by the first provider |

| Failover | During a provider outage | Maintain payment continuity by switching providers automatically | Provider unavailability, timeout, or technical failure |

The Main Benefits of Intelligent Payment Routing

Akurateco’s CEO and Co-Founder, Volodymyr Kuiantsev, shares his insights into the transformative benefits of smart payment routing.

Intelligent payment routing is crucial for businesses to optimize transaction success rates and enhance the user experience. It’s a revolutionary technology in the world of payments that ensures transactions are processed efficiently and securely, regardless of any issues with individual providers. By dynamically selecting the best payment path, businesses can reduce payment failures, improve risk management, and increase customer satisfaction.

Now, let’s delve into the major benefits of payment routing in detail:

Reduced processing cost

Payment gateway routing reduces processing costs by sending transactions to payment providers with the lowest Interchange + and Interchange ++ fees that merchants pay for transaction processing. The fee amount differs depending on many factors, such as card level, type of card used, the issuer, the issuer’s country, etc. Accordingly, if the payment provider routes the transaction to a MID with a lower interchange fee, it captures more revenue. The system may also use smart routing to evaluate real-time analytics and route transactions to the most cost-effective processor, capturing more revenue.

Increased approval rate

The approval rate rises when the transaction is sent for processing to the payment provider or bank that is most likely to approve it. This is because it considers each payment connector’s limitations in processing certain payment types, such as from users whose countries are blocked or from high-risk industries, and does not send transactions for processing to such providers in the first place. This approval rate increase is also achieved through machine-driven logic and AI-enhanced analytics.

Enhanced transaction flow management

Besides the payment routing process, some white-label payment gateway providers like Akurateco also provide prerouting. It is a technology that enables routing transactions to MIDs based on data unrelated to credit or debit cards. Prerouting is used to allow routing transactions to Alternative Payment Methods (APMs). Prerouting to APMs can be done by currency, payer’s country, and other parameters. Fundamentally, prerouting is an additional technology that helps users manage transaction flows. This allows for smart routing based on parameters like currency or payer’s country, and improves overall recovery rates for failed transactions.

Common Payment Routing Parameters

Payment routing can use different parameters to decide where a transaction should be sent. The exact setup depends on the business model, payment methods, regions, providers, and optimization goals, but most routing logic is based on a combination of transaction, customer, card, and provider data.

Geolocation of the billing address

Billing location can help route payments to local acquirers or payment providers. This may improve approval rates, reduce cross-border processing costs, and make the payment flow more relevant to the customer’s region.

Payment method

A transaction can be routed based on whether the customer uses a credit card, debit card, alternative payment method, wallet, bank transfer, or another payment option. This helps send each transaction to the provider best suited to process that payment method.

Customer segment or whitelist status

Some businesses route trusted customers, repeat buyers, VIP users, or whitelisted traffic through specific providers or MIDs. This can help manage risk, protect high-value traffic, or apply different rules to known customer groups.

Bank Identification Number (BIN)

BIN-based routing uses the first digits of a card number to identify details such as the issuing bank, card type, card brand, and country. This helps route transactions to providers with stronger approval performance for specific issuers or card profiles.

BIN country

The card’s issuing country can also influence routing. For example, local cards may be routed to local acquirers, while international cards may be sent through providers with better cross-border performance or lower processing costs.

Card brand

Routing can also depend on the card network, such as Visa, Mastercard, or other card brands. Some providers may offer better approval rates or lower fees for specific card brands, making this a useful parameter for cost and performance optimization.

Currency

Currency-based routing sends transactions to providers that support the relevant currency or offer better processing conditions for it. This can help reduce conversion costs and improve the payment experience for customers in different markets.

Transaction amount

Transaction amount can affect risk level, fees, and provider performance. Businesses may route high-value, low-value, or recurring transactions differently depending on approval history, risk rules, or processing cost.

Provider performance and availability

Routing logic can also consider real-time or historical provider performance, including approval rates, response time, downtime, decline patterns, and technical errors. If one provider is unavailable or underperforming, traffic can be directed to another available provider.

Custom routing rules

Businesses can also combine several parameters in one routing rule. For example, a transaction can be routed based on card brand, BIN country, currency, amount, and provider performance at the same time. This makes routing logic more flexible and allows businesses to adapt payment flows to different regions, customer segments, and operational goals.

Real-life Use Cases: How Akurateco’s Clients Benefit from Smart Payment Routing

The businesses we are about to review operate in diverse sectors and geographical regions. Their real names remain confidential.

Client A: Routing FTD and Whitelisted Traffic Separately

Challenge: A PSP supporting global e-commerce lacked routing flexibility for first-time deposits (FTD) and whitelisted traffic, risking false declines and revenue loss.

Solution: Akurateco set up smart routing payments to send whitelisted traffic and FTD transactions to different MIDs, with automatic cascading on FTD declines.

Result:

$150,000+ savings in system maintenance over one year.

11% increase in approval rate.

Client B: Balancing Transactions Across MIDs

Challenge: A global streaming service needed to distribute traffic evenly across two MIDs to avoid exceeding transaction limits.

Solution: Akurateco configured “Distribute by count” and “Distribute by percentage” modules for balanced transaction flow.

Result:

No velocity limit breaches.

Optimized merchant processing capacity.

Increased number of successful daily transactions without system failures.

Client C: Optimizing Local and International Traffic

Challenge: A Qatari telecom provider needed to route local and international payments to different acquirers for cost efficiency.

Solution: Akurateco routed local transactions to the local acquirer (lower interchange fees) and international transactions to a more affordable international provider.

Result:

0.5% cost savings on every cross-border payment.

Optimized interchange fees across all payments.

Would you like to know more about how we did it? Check out success stories below.

How to Get Started with Intelligent Payment Routing

Businesses typically start by reviewing their current payment flows, identifying where transactions fail, and defining routing rules based on provider performance, geography, card type, cost, currency, and approval history. From there, they can test different provider combinations and adjust routing logic to improve approval rates, reduce failed payments, and control processing costs.

To sum up

Every failed transaction is lost revenue, and that’s a cost you can no longer afford to ignore. Intelligent payment routing isn’t just a technical upgrade; it’s a business growth strategy. From cost reduction to customer satisfaction and operational efficiency, it empowers your business to turn payment processing into a competitive advantage.

In practice, intelligent payment routing and cascading can help businesses improve approval rates, reduce processing costs, and recover revenue that may otherwise be lost to failed transactions.

FAQ

What is payment routing?

Payment routing is the process of choosing where a payment transaction should be sent for processing. It can route transactions to different providers, acquirers, or payment methods based on rules such as geography, card type, currency, cost, risk level, or past approval performance.

What is smart payment routing?

Smart payment routing is a more advanced form of payment routing that uses rules, performance data, or machine learning to choose the best available provider for each transaction. Its goal is usually to improve approval rates, reduce failed payments, and control processing costs.

How does payment routing work?

Payment routing works by evaluating a transaction before it is sent for authorization. The system checks factors such as card BIN, country, currency, payment method, provider availability, cost, and approval history, then sends the transaction to the provider most likely to process it successfully.

What is transaction routing?

Transaction routing is the broader process of directing a transaction to the most suitable processing path. In payments, transaction routing often means sending each payment to the right provider, acquirer, or payment method based on predefined business and performance rules.