- What Is the Credit Card Life Cycle?

- What Are the Key Stages of the Credit Card Customer Life Cycle?

- What Is the Credit Card Transaction Lifecycle?

- Why Is Credit Card Life Cycle Management So Complex?

- What Are the Hidden Costs of Managing the Lifecycle In-House?

- What Are the Different Approaches to Credit Card Life Cycle Management?

- Why Orchestration Is Emerging as a Better Approach

- How Payment Orchestration Improves Life Cycle Management

- Key Takeaways

- Conclusion

Credit cards look simple to the user, but the operating model behind them is complex. The credit card lifecycle is the full sequence of events around a card relationship: onboarding, issuance, activation, usage, transaction processing, billing, fraud controls, credential updates, renewal or reissue, and closure. Managing it well means standardizing data, controls, routing, retries, and reporting across those stages.

The scale of that challenge is significant. In the U.S., 80% of adults had a credit card in 2022, and total credit card debt reached $1.13 trillion by the end of 2023. Boston Fed research also shows that credit limits change frequently over the lifecycle, while debt tends to move with available credit. In other words, cards, limits, and credentials do not stay fixed over time.

For teams focused on recurring payments and card-on-file performance, the main lever is better lifecycle control. That means managing credentials, routing, retries, reconciliation, and reporting through one consistent operating model. In this context, Akurateco’s payment orchestration platform becomes relevant by helping you manage payment flows, routing, reconciliation, and lifecycle complexity through one control layer.

What Is the Credit Card Life Cycle?

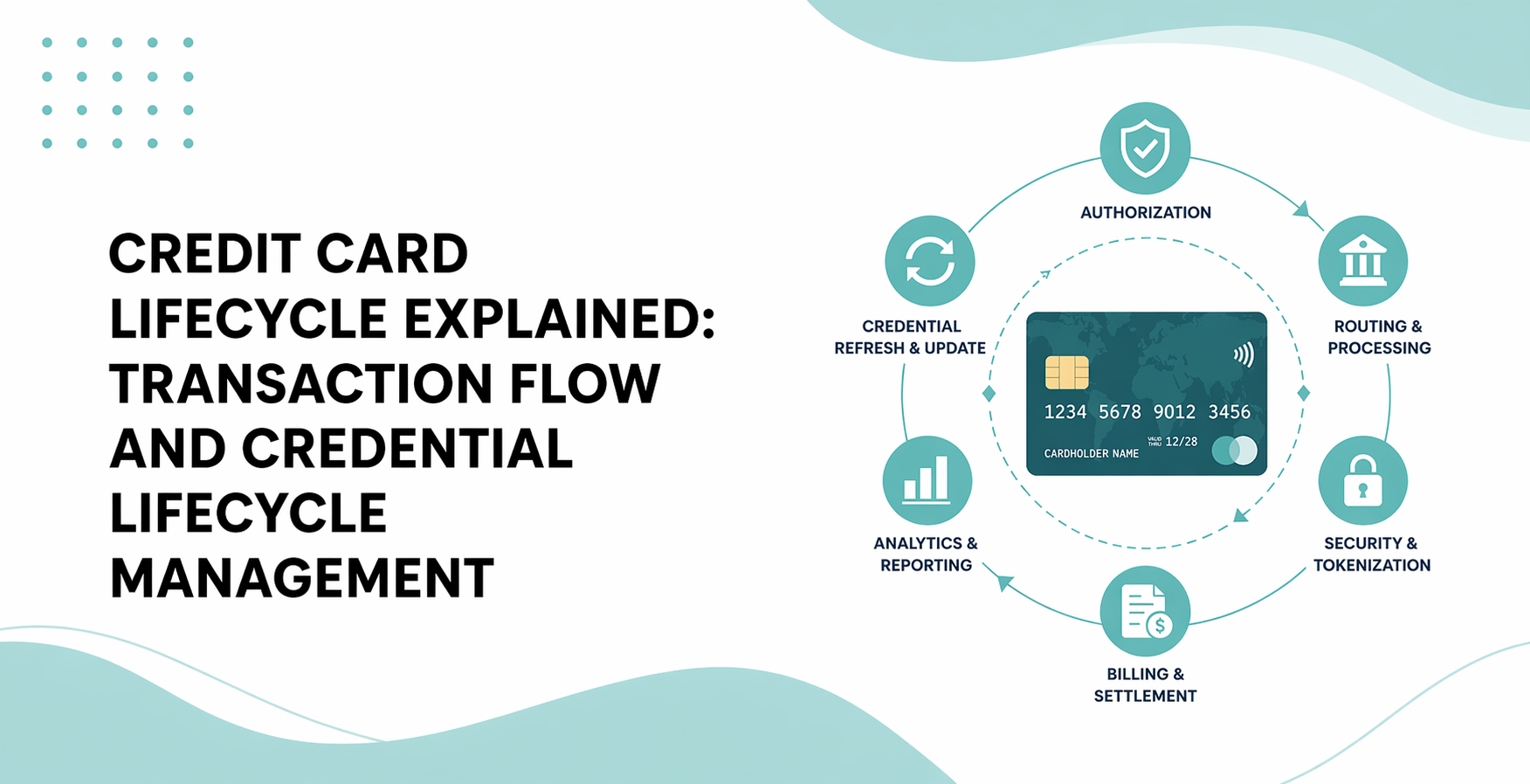

The credit card life cycle is broader than one payment. It covers the full customer, transaction, and credential journey from onboarding and issuance to settlement, renewal, and closure.

In payments operations, the term often gets used too narrowly. Many teams use it as shorthand for the credit card transaction lifecycle: payment authorization, batching, clearing, and settlement. That is correct for transaction processing, but it misses what happens after the first successful payment, especially when you store card details for future use.

A more useful definition for merchant-side payment and product teams is this: the credit card lifecycle has three connected layers:

- Customer lifecycle: acquisition, onboarding, issuance, activation, billing, retention, closure.

- Transaction lifecycle: authorization, batch submission, clearing, settlement, reconciliation, disputes.

- Credential lifecycle: keeping stored credentials, tokens, expiry dates, and account references current so future payments still work.

That broader view matters because a payment can fail even when your checkout is technically fine. The issue may sit in an expired card, a reissued PAN, a suspended network token, or poor recovery logic after a decline. Lifecycle management is how you prevent those problems from leaking into revenue loss.

What Are the Key Stages of the Credit Card Customer Life Cycle?

The credit card customer life cycle starts before the first payment and continues long after it. Operators need to map the full sequence, not just the moment of authorization.

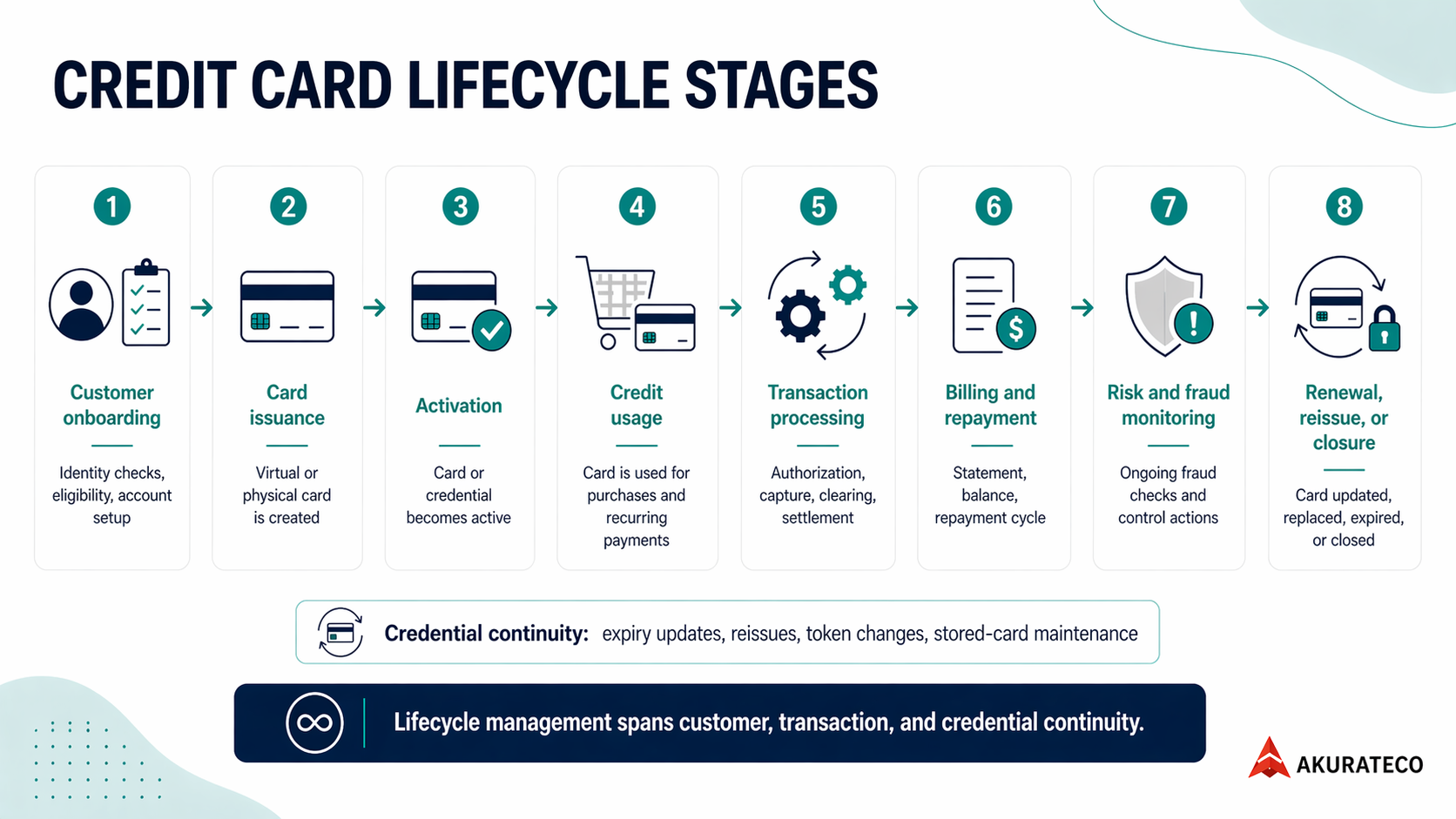

A credit card program does not begin when a transaction is approved, and it does not end when a statement is paid. It moves through a sequence of connected stages that shape customer experience, risk exposure, operational workload, and long-term profitability. Each stage has its own purpose, systems, and controls, but all of them affect how the card performs over time.

Customer acquisition and onboarding

This is the stage where the future cardholder enters the lifecycle. The issuer or provider attracts the customer, collects application data, verifies identity, checks eligibility, and decides whether to approve the account.

In issuer-led models, this usually includes:

- Application review

- KYC and identity verification

- Underwriting

- Credit limit setting

- Terms acceptance

In merchant and PSP contexts, the operational equivalent is customer signup, payment method capture, consent collection, and preparation for future billing. This stage matters because weak onboarding can create fraud, servicing, and repayment problems later.

Card issuance: virtual and physical

The provider issues a physical card, a virtual card, or both, and links the credential to the customer’s account, limits, and security settings.

A virtual card can often be used almost immediately, while a physical card adds production and delivery steps. This stage is important because the form of the card affects later activation, wallet provisioning, replacement, and card-on-file usage.

Activation

Activation is the point at which the card or credential becomes live for spending. It confirms that the cardholder has received the card or is ready to use the credential.

For physical cards, this often means confirming receipt and completing security checks. For digital-first programs, activation may happen during first use or wallet provisioning. In merchant environments, the parallel moment is when a stored credential becomes valid for repeat billing or future checkout.

Credit usage and authorization

The customer begins using the card for purchases. Each time the card is presented, the issuer decides whether to approve or decline the transaction based on available credit, account status, fraud signals, and policy rules.

This is the most visible stage to the customer because it directly affects whether a payment goes through. Operationally, it is only the beginning of the processing chain, not the end of it.

Transaction processing

This is the technical core of the lifecycle. It covers what happens after the card is used, including authorization, capture, batching, clearing, settlement, reconciliation, and possible disputes.

It determines how transaction data moves, how funds are posted and transferred, and how payment teams investigate failed, delayed, or mismatched revenue events. For many payment operators, this is where most infrastructure complexity lives.

Billing and repayment

The issuer posts transactions to the cardholder’s statement and the customer repays the balance according to the card terms. The customer may pay in full or carry part of the balance forward.

This stage includes statement generation, balance updates, minimum payment logic, interest application, and delinquency monitoring. It is important because repayment behavior affects available credit, future authorization performance, and portfolio risk.

Risk and fraud monitoring

This is the continuous control layer that runs across the life cycle. Fraud and risk checks do not happen only once. They can be applied before authorization, during transaction processing, and after a payment is completed.

Suspicious behavior may trigger step-up verification, token suspension, card reissue, transaction blocking, or even account closure. This stage is essential because it protects both payment performance and long-term account health.

Retention and life cycle extension

This stage focuses on keeping the card active, useful, and profitable over time. It includes renewals, reissues, credit line changes, product upgrades, credential refreshes, token updates, and continued card-on-file usage.

For subscription businesses, platforms, and marketplaces, this is also the stage where revenue continuity matters most. Good lifecycle management here helps reduce involuntary churn and keeps existing customers transacting smoothly.

Card closure

This is the final stage of the lifecycle. The card or account is closed, replaced, suspended, or otherwise taken out of active use. Closure may happen because of customer choice, expiration, fraud, delinquency, portfolio strategy, or product migration. Operationally, this stage still requires control, because future billing may fail, stored credentials may need updating, and unresolved disputes or balances may remain after active use ends.

Taken together, this is the credit card customer lifecycle that operators actually need to manage. It spans issuance to deactivation, while recurring revenue teams also need active control of stored credentials, renewal events, and reissue recovery.

What Is the Credit Card Transaction Lifecycle?

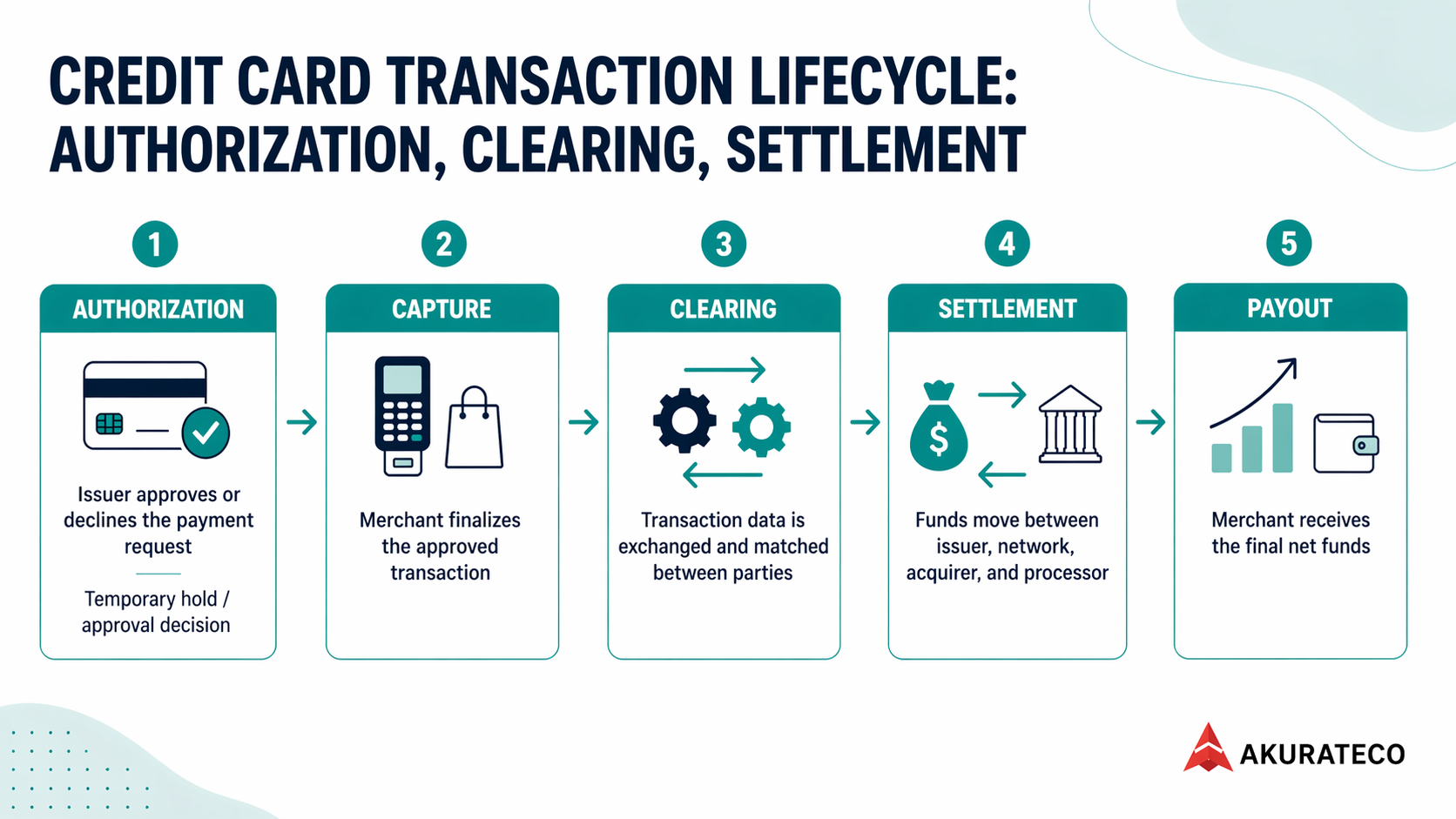

The credit card transaction lifecycle is the operational path of a single card payment. It starts with authorization and ends only after funds, fees, reporting, and any disputes are fully reconciled.

A card payment may look instant at checkout, but operationally, it moves through several distinct stages. An approved transaction still needs to be captured, cleared, settled, reported, and sometimes disputed. For PSPs, payment operators, and enterprise merchants, the transaction lifecycle matters because it determines not just whether a payment is approved, but whether revenue is actually realized, recorded correctly, and protected from later loss.

![]()

Authorization flow

Authorization is a real-time approval or decline decision. The merchant sends the transaction through the gateway, processor, acquirer, and card network to the issuer. The issuer checks available credit, card status, fraud signals, authentication results, and internal rules, then returns an approval or decline.

An approval is not final funding. It usually means the issuer has reserved funds or credit for the transaction. The payment can still fail later if capture, clearing, or settlement does not happen correctly.

Batching process

Authorized transactions do not become settled funds automatically. They usually remain pending until the merchant or provider submits them for downstream financial processing. That submission step is batching.

Batching groups capture transactions and send them forward for clearing and settlement, often on a schedule. If batching is delayed, fails, or contains errors, it can cause funding delays, reporting mismatches, and reconciliation issues.

Clearing process

Clearing is the formal exchange of finalized transaction data between the relevant parties. It confirms what happened in the transaction and prepares it for posting and fee calculation.

At this stage, the transaction moves through the acquirer, processor, network, and issuer so it can be recorded properly. Clearing is not the same as merchant payout. It is the structured data exchange that supports financial posting and downstream settlement.

Settlement mechanics

Settlement is the fund movement stage. After clearing, funds move through the issuing and acquiring sides so the merchant can be paid, net of interchange, scheme fees, processor fees, reserves, and other deductions.

Settlement timing varies by provider setup, batch cutoff, risk controls, and commercial model. That is why approval should never be treated as the same thing as cash received.

Reconciliation

Reconciliation is the process of matching transaction and financial records across systems. This is where payment teams confirm that the lifecycle events and money movement are consistent.

In practice, reconciliation means matching:

- Authorizations

- Captures

- Batches

- Clearing records

- Settlement files

- Fees

- Reserves

- Refunds

- Payouts

- Chargebacks

This stage is critical because different providers often expose different statuses, timestamps, and report structures. Without reconciliation, teams cannot reliably explain missing funds, delayed payouts, or reporting discrepancies.

Chargebacks

Chargebacks happen after the main payment flow, but they still belong in the transaction lifecycle. They can reverse revenue and create new operational work after a transaction appears complete.

A chargeback may result from fraud, customer disputes, recurring billing complaints, service issues, or issuer action. For payment teams, chargebacks are not separate from lifecycle management. They are a downstream stage that affects reporting, recovery, merchant exposure, and net revenue.

For a deeper look at post-authorization money movement, see Akurateco’s guide to how the payment settlement process works.

Why Is Credit Card Life Cycle Management So Complex?

Credit card lifecycle management is complex because one card program depends on multiple parties, disconnected data, different processing speeds, and strict compliance obligations. What looks like one payment journey is actually a chain of systems and decisions that must stay aligned from onboarding to closure.

A credit card lifecycle is not managed in one platform or by one team. It runs across issuers, processors, gateways, acquirers, fraud tools, billing systems, and reporting layers. Each of them handles a different part of the lifecycle, which makes coordination difficult and creates gaps between operational events and financial outcomes.

Multiple systems across the payment chain

A single card event can pass through several parties before it is completed. The issuer manages the account and credit decision. The gateway transmits the payment request. The processor and acquirer handle transaction routing and financial processing. Each party sees only part of the lifecycle, not the whole picture.

That fragmented structure creates operational complexity. A transaction may appear successful in one system, still be pending in another, and fail later in settlement or reconciliation. Without a unified view, teams spend more time matching statuses than improving performance.

Data fragmentation

Each system generates its own records, timestamps, statuses, and reports. Authorization data may sit in one dashboard, settlement data in another, and dispute records somewhere else. Even when all systems are technically working, the data is often not organized in one consistent lifecycle view.

This makes it harder to answer simple operational questions with confidence:

- Was the transaction only authorized or also settled?

- Did the refund reduce the original payout or post separately?

- Is the issue a processor delay, a reporting mismatch, or a real revenue loss?

That is why lifecycle management is not just about processing payments. It is also about connecting fragmented data into one usable operating model.

Real-time vs. batch processes

Some parts of the lifecycle happen instantly. Authorization decisions are made in seconds. Other parts happen later, often in scheduled or batch-based workflows, such as capture, clearing, settlement, billing, and reconciliation.

This difference in timing is one of the biggest sources of confusion. A payment can be approved in real time but still remain unsettled, delayed, or mismatched later. In other words, customer-visible success does not always mean operational completion.

Compliance requirements

Credit card lifecycle management also carries a heavy compliance burden. Payment data, authentication, dispute handling, and reporting all operate within card-network rules, security standards, and regulatory expectations.

The more lifecycle stages you manage directly, the more responsibility you take on for controls, data handling, audit readiness, and operational governance. That makes lifecycle management not only a technical problem but also a security and compliance challenge.

What Are the Hidden Costs of Managing the Lifecycle In-House?

The hidden cost of in-house credit card lifecycle management goes beyond the initial build. The bigger burden comes from maintaining integrations, handling recovery logic, keeping reports consistent, and proving compliance across the full payment lifecycle.

Many teams budget for payment acceptance, but not for everything around it. The higher cost appears after launch, when the business has to keep the lifecycle stable, traceable, and scalable across multiple providers, transaction events, and reporting systems.

The hidden costs usually appear in the following five areas.

1. Maintenance overhead

In-house lifecycle management requires continuous maintenance, not a one-time delivery. Teams have to keep gateway, acquirer, processor, account updater, token, and reporting integrations current as APIs, network rules, and partner requirements change.

The result is a permanent engineering load. Even when transaction volume stays steady, the lifecycle still needs fixes, monitoring, version updates, and support for edge cases.

2. Scaling challenges

Scaling does not only mean handling more transactions. It also means supporting more lifecycle variations.

Each new PSP, acquirer, geography, or payment method adds another model for authorization, retries, settlement timing, token updates, reporting, and disputes. As the stack grows, the business has to normalize more statuses, more files, and more provider-specific logic.

3. Compliance burden

In-house lifecycle management increases the compliance workload tied to payment operations. Teams must retain consent records, stored credential logic, audit trails, and evidence showing how payment events were handled across systems.

The burden grows over time. The more life cycle stages you manage directly, the more responsibility you carry for traceability, control, and audit readiness.

4. Integration complexity

Lifecycle management is difficult because payment events rarely arrive in one standard format. Account updater events, retries, routing decisions, token changes, reporting files, settlement records, and dispute updates may all come from different systems with different structures.

So the challenge is not only building integrations. It is also translating and aligning fragmented life cycle data so it can be used reliably across operations, finance, and support.

5. Operational inefficiency

When lifecycle data is fragmented, teams spend time proving what happened instead of improving performance. They investigate missing settlements, compare provider reports, trace retry paths, check token status changes, and explain revenue mismatches across systems.

That creates hidden costs across finance, support, risk, and payment operations. The problem is not only the time spent processing payments but also the time spent explaining them.

What Are the Different Approaches to Credit Card Life Cycle Management?

You can manage the lifecycle in-house, through provider-native tools, or through an orchestration layer. The best choice depends on how many providers, entities, and recovery scenarios you need to control.

There is no single model that fits every payment business. The right approach depends on the shape of your operation: how many PSPs you use, how often credentials change, how much retry and intelligent routing logic you need, and how important unified reporting is across entities or markets. A setup that works for a single-processor business can become restrictive once payment flows, recovery paths, and lifecycle data start spreading across multiple providers.

That is why credit card lifecycle management should be treated as an operating-model decision, not just a tooling choice. Some businesses prioritize full control and are willing to build internally. Others want speed and rely on provider-native features. Others reach a point where lifecycle controls need to sit above individual providers so routing, retries, credential updates, and reporting can be managed more consistently.

Approach | Pros | Cons | Best for |

| In-house stack | Full control, custom logic, direct ownership of data model | Slow to build, expensive to maintain, hard to scale across PSPs | Large teams with deep payment engineering resources |

| Third-party provider tools | Faster start, less initial build, native access to one provider’s features | Fragmented across providers, uneven reporting, limited portability | Single-processor or low-complexity setups |

| Orchestration layer | Centralized controls, shared reporting, easier multi-PSP recovery, and routing | Requires design discipline and operating rules | High-load, multi-PSP, recurring, or cross-entity environments |

In-house control gives you flexibility, but also the highest maintenance burden. Provider-native tools reduce the initial build, but often make the lifecycle harder to govern once you expand beyond one processor. An orchestration layer sits between those two extremes. It does not remove complexity from payments, but it gives you a more structured way to manage that complexity across providers, entities, and lifecycle events.

That is why the best approach is usually the one that matches your future operating model, not only your current setup. If your payment environment is simple, provider-native tools may be enough. If lifecycle logic, reporting, and recovery flows are already spread across multiple systems, a more centralized orchestration approach becomes easier to justify.

Why Orchestration Is Emerging as a Better Approach

Orchestration is gaining ground because credit card lifecycle management usually spans multiple providers. A central control layer is often more effective than adding isolated tools one by one.

Payment orchestration is a software layer that connects multiple payment providers and lets you manage routing, retries, failover, reporting, and other payment logic from one place. As payment operations grow, those controls often end up scattered across gateways, acquirers, PSPs, fraud tools, and reporting systems. What starts as a workable setup can become fragmented over time.

Orchestration is emerging as a better approach because it brings those controls together and makes the lifecycle easier to manage as one system:

- Centralized control. Manage routing, retries, decline recovery, credential logic, and reporting rules from one layer instead of splitting them across provider setups.

- Unified visibility. Bring authorizations, updater events, settlements, payouts, and disputes into one operational view.

- Improved routing and approvals. Apply recovery and routing logic more consistently, which helps reduce avoidable declines and revenue loss.

- Easier integrations. Add new PSPs, acquirers, or payment methods without rebuilding lifecycle logic each time.

- Scalability. Support higher volumes, more entities, more geographies, and more recovery scenarios with a more repeatable operating model.

Orchestration does not remove lifecycle complexity, but it makes that complexity easier to manage. When payment flows and recovery logic span multiple systems, a central orchestration layer becomes easier to justify than another disconnected point solution.

How Payment Orchestration Improves Life Cycle Management

Payment orchestration improves life cycle management by giving you one layer to control routing, cascading, monitoring, reconciliation, and multi-PSP operations. Instead of managing payment events in separate provider systems, you manage them through one operating model.

Payment orchestration is a software layer that connects multiple payment providers and lets you control payment logic from one place. In lifecycle management, that matters because card payments do not fail or succeed in one moment alone. They move through routing, retries, settlement, reporting, and recovery stages that often sit across different PSPs, acquirers, and tools.

A payment orchestration platform improves life cycle management in five main ways:

- Intelligent routing. Payment orchestration routes each transaction to the most suitable provider based on business rules, geography, BIN, payment method, or performance conditions.

- Cascading. Payment orchestration can retry a failed payment through an alternative provider or path when recovery logic allows it.

- Monitoring. Payment orchestration gives teams one place to track approvals, declines, retries, settlements, and provider performance.

- Reconciliation. Payment orchestration helps match transaction records, settlement data, fees, and payouts across multiple providers.

- Multi-PSP strategy. Payment orchestration makes it easier to run several PSPs at once without rebuilding lifecycle logic for each integration.

A simple way to think about it is this: payment orchestration chooses the best path for the transaction, while lifecycle orchestration manages what happens when the payment state changes over time. One focuses on transaction flow. The other focuses on payment continuity, recovery, and control.

Akurateco’s payment orchestration platform is built for businesses that need centralized routing, cascading, monitoring, reconciliation, and multi-PSP control. That makes lifecycle management easier to scale, easier to govern, and easier to explain across operations, finance, and product teams.

Key Takeaways

- Map the full credit card lifecycle, not only the transaction itself.

- Treat authorization, clearing, settlement, and payout as separate operational stages.

- Maintain credentials and tokens to protect recurring payment continuity.

- Standardize reporting and reconciliation across providers.

- Plan for the hidden cost of maintenance, compliance, and fragmented data.

- Use orchestration when lifecycle logic starts spreading across multiple systems.

Conclusion

The best way to think about the credit card lifecycle is not as one pipeline, but as two connected systems. One system moves payments from authorization to settlement. The other keeps future payments possible by managing credentials, token states, retries, and recovery paths.

For that reason, lifecycle management becomes an architectural decision, not just an operational task. If you run recurring payments, multi-PSP traffic, or high-volume card-on-file flows, the question is not whether lifecycle complexity exists. It is whether you manage it in fragments or through one control layer.

Akurateco is built for this kind of payment complexity: it brings routing, cascading, monitoring, reconciliation, and multi-PSP control into one orchestration layer, making lifecycle management easier to govern and scale.

FAQ

What is the credit card lifecycle?

The credit card lifecycle is the full sequence of events around a card relationship. It includes onboarding, issuance, activation, transaction processing, billing, repayment, fraud controls, credential updates, and closure. For merchants and PSPs, it also includes the controls that keep future card-on-file payments working.

What is the difference between clearing and settlement?

Clearing is the exchange and finalization of transaction data, including fee logic. Settlement is the movement of funds between the issuer and acquiring sides. Funding or payout is when your business receives the net deposit. They are linked, but they are not the same operational event.

What is credential lifecycle management for card-on-file payments?

Credential lifecycle management means keeping stored payment credentials usable over time. It covers expiry changes, reissued cards, closed accounts, payment tokenization, and recovery controls for recurring billing. The goal is to reduce preventable declines and protect repeat revenue without relying on customers to manually fix every credential.

How does the card account updater work?

A card account updater checks for issuer-reported account changes and returns updated details where available, such as a new PAN or expiry date. Visa and Mastercard both offer updater programs for card-on-file and recurring scenarios. These tools help with credential-change problems, but they do not fix every decline type.

What is network token lifecycle management, and why does it matter?

In a network tokenization model, network token lifecycle management keeps tokenized credentials aligned with underlying account changes. It can include status events such as ACTIVE, SUSPENDED, and DELETED, plus updates like new expiry dates or PAN changes behind the token. It matters because token continuity can improve recurring payment resilience and reduce manual recovery work.

What should you do when a recurring payment fails because the details are outdated?

Start with updater or token lifecycle checks. If the credential can be refreshed, update it before retrying. Then use controlled retry logic, apply rerouting only where appropriate, and prompt the customer only when automation cannot fix the failure. This sequence is usually more effective than blind resubmission.