Recurring businesses don’t lose revenue only because customers cancel. A significant share of failed payments happens silently—when card credentials change.

Cards expire, get replaced after fraud, or updated by issuers. According to industry data, a large portion of cards change every year, which directly affects businesses relying on card on file billing. As a result, companies experience more expired card declines, lower authorization approvals, and growing involuntary churn.

This is exactly where a card account updater becomes critical.

In this guide, payment teams at subscription, marketplace, and card-on-file businesses will learn what a card account updater is, how it works, how it improves acceptance rates, and how to implement it as part of a complete revenue recovery strategy.

What is card account updater?

A card account updater is a service that automatically refreshes stored card credentials when issuing banks update or replace a customer’s card. It ensures that saved payment details remain valid for recurring payments, subscriptions, and one-click checkouts—without requiring any action from the customer.

In practice, when a card expires, is reissued due to loss or fraud, or is replaced with new details, the updater connects to card networks (such as Visa or Mastercard) and retrieves the updated information. This allows merchants to continue billing customers seamlessly, avoiding failed transactions and unnecessary churn.

Beyond simple convenience, card account updaters play a critical role in revenue protection. They help reduce declined payments, improve authorization rates, and maintain continuity in subscription-based business models. For merchants operating at scale, this translates into higher retention, fewer involuntary cancellations, and lower operational overhead lower operational overhead associated with manual data updates.

In short, a card account updater acts as a behind-the-scenes reliability layer keeping payment credentials current so that recurring transactions can proceed without disruption.

Visa: visa account updater (vau)

The visa account updater (vau) allows merchants to receive updated card details when cards are reissued, expired, or replaced. It supports both scheduled batch updates and real-time updates at the moment of transaction.

Importantly, it can also return signals like account closed or opt-out status, helping merchants avoid unnecessary retries and optimize billing logic.

Mastercard: mastercard automatic billing updater (abu)

The mastercard automatic billing updater (abu) is designed to maintain continuity for card on file and recurring transactions. It helps reduce payment failures caused by outdated credentials and supports higher approval rates for card-not-present payments.

For subscription businesses, this translates directly into fewer interruptions and improved billing consistency.

How an Account Updater Improves Acceptance Rates

A card account updater addresses one of the most common and preventable causes of payment failure: outdated card credentials.

When cards expire, are reissued, or replaced due to fraud or loss, stored payment details quickly become invalid. Without an updater, businesses depend on customers to manually update this information—a process that often doesn’t happen in time, leading to failed transactions and lost revenue.

An account updater removes this dependency by automatically refreshing card details through card network integrations. As a result, transactions are submitted with up-to-date credentials, significantly reducing declines связаные с expired or replaced cards.

The impact goes beyond fewer failures. By ensuring that valid credentials are used at the moment of authorization, updaters directly contribute to higher approval rates and more stable payment performance. This is particularly critical for subscription-based models, where even small improvements in acceptance can compound into meaningful revenue gains.

Consider a subscription business processing 10,000 monthly renewals with an 8% failure rate. If 40% of those failures are caused by outdated card details, that’s 320 declined payments. With an account updater recovering just 60% of those, nearly 200 transactions are saved.

This translates into:

- higher acceptance rates

- reduced involuntary churn

- improved customer lifetime value

- less operational effort spent on recovery flows

In essence, a card account updater doesn’t just fix failed payments—it prevents them from failing in the first place, turning what would have been lost revenue into successfully completed transactions.

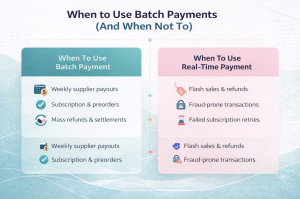

Batch vs real-time updater

Batch and real-time approaches serve different purposes in subscription billing.

Batch updates work on a schedule, refreshing large volumes of stored credentials ahead of billing cycles. This approach is efficient for predictable recurring payments and helps maintain a clean dataset over time.

A real-time account updater, on the other hand, checks and updates card details at the moment of transaction. This is especially valuable for high-value users, high-frequency billing, or situations where every transaction matters.

Most advanced setups combine both approaches—using batch updates for broad coverage and real-time updates for critical payments.

Implementation options

There are several ways to implement an account updater service, depending on your infrastructure.

You can enable it through your PSP or acquirer, which is often the simplest option but may limit visibility and flexibility across providers. Alternatively, you can integrate it via a payment orchestration platform, which provides a unified layer for managing updates, retries, and reporting across multiple PSPs.

A hybrid approach is often the most effective. In this model, batch updates maintain baseline data quality, while real-time updates are applied to high-value or high-risk transactions.

It’s important to understand that updates are not guaranteed. Issuers may not participate, cards may be closed, and customers may opt out. This makes it essential to combine the updater with broader recovery strategies.

Security and compliance considerations

A strong updater strategy should always be combined with tokenization. This ensures that updated card data is stored securely and reduces exposure of sensitive payment information.

Tokenization also helps support safer handling of stored credentials and can contribute to PCI scope reduction, depending on how your payment architecture is designed. However, this benefit should be evaluated carefully based on your specific implementation.

The acceptance playbook (updater + retries + routing)

To truly improve performance, a card account updater must be part of a broader system.

The process starts with updating credentials before billing. If a payment still fails, retry logic comes into play, using optimized timing and issuer response signals to maximize success without overloading the system.

If retries fail, routing optimization allows transactions to be sent through the best-performing acquirer. In more advanced setups, cascading payments can retry transactions across multiple providers to recover additional revenue.

Only when all automated options are exhausted should customer communication be triggered, minimizing friction while preserving revenue.

Metrics to track

Measuring performance is critical to understanding the value of an updater.

The most important metric is update hit rate, which shows how many accounts were successfully updated compared to total queries. This directly reflects the effectiveness of your updater integration.

You should also track acceptance uplift by comparing approval rates before and after implementation. Additional metrics include recovered revenue, reduction in involuntary churn, and changes in decline reasons—particularly a decrease in expired card declines.

Finally, evaluating cost versus recovered revenue helps determine the true ROI of your updater strategy.

Common mistakes

One common mistake is treating an updater as a complete solution. In reality, it only addresses credential-related issues and must be combined with retries and routing.

Another issue is failing to handle closed accounts or opt-outs correctly, which can lead to unnecessary retries and degraded performance.

Some businesses also overwrite customer-selected payment methods without proper controls, which can create trust and compliance issues.

Finally, without a clear reporting baseline, it becomes impossible to measure impact or justify investment.

Conclusion

A card account updater is a foundational component for any business relying on recurring payments. By keeping stored credentials up to date, it directly reduces failures caused by expired or replaced cards—one of the most common sources of avoidable declines.

However, its real impact is unlocked when combined with a broader payment optimization strategy.

On its own, an updater improves data accuracy. But when integrated with smart retry logic, dynamic routing, and cascading payments, it becomes part of a system designed to maximize transaction success. Together, these components ensure that payments are not only attempted with the right credentials, but also processed through the most optimal paths, with built-in recovery mechanisms in case of failure.

This shifts payments from a static process to an adaptive one—capable of responding in real time to changing conditions.

The result is clear:

higher acceptance rates, lower involuntary churn, and more predictable revenue.

In this context, a card account updater is not just a supporting feature—it’s a critical layer in building resilient, high-performing payment infrastructure.

FAQ

What is card account updater?A card account updater is a service that automatically refreshes stored card credentials when a customer’s card is updated, replaced, or expired. It works by connecting to card network programs like Visa and Mastercard, which provide updated data when available. This allows businesses to continue charging customers without requiring them to manually update their payment details.

What’s the difference between batch and real-time updater?Batch updater works on a schedule, updating large sets of stored credentials before billing cycles. Real-time updater operates during the transaction itself, checking if updated card details are available at that exact moment. In practice, most businesses benefit from combining both approaches to maximize coverage and recovery rates.

Does VAU or ABU update closed accounts or opt-outs?No, these programs do not update closed accounts or cards where the customer has opted out. Instead, they return signals indicating that the account is no longer active or eligible for updates. This helps merchants avoid unnecessary retries and adjust their recovery strategies accordingly.

Will an updater improve all payment declines?No, an updater only addresses declines caused by outdated or changed card credentials. Other types of declines, such as insufficient funds or issuer restrictions, require different strategies like retries, routing optimization, or customer intervention. That’s why it should be part of a broader payment optimization system.

How do you measure ROI for an updater program?ROI is measured by comparing recovered revenue against the cost of running the updater service. Key indicators include update hit rate, improvement in approval rates, reduction in involuntary churn, and fewer expired card declines. A proper measurement framework ensures you can clearly see the financial impact of the implementation.

How does tokenization relate to account updaters?Tokenization ensures that updated card data is stored securely without exposing sensitive information. When combined with an updater, it allows refreshed credentials to be safely reused in future transactions. This improves both security and operational efficiency in recurring billing systems.