- What Is Payment Reversal?

- The 3 Types of Payment Reversals Explained

- The Comparison of Authorization Reversal, Refund, and Chargeback

- Where Reversals Happen in the Card Flow: The Timeline

- Reversals and Reconciliation: Why Your Payouts Don’t Match Sales

- How to Reduce Avoidable Payment Reversals: Practical Prevention Playbook

- Costly Mistakes Merchants Make With Payment Reversals

- Conclusion

- FAQ

As much as merchants would rather avoid them, payment reversals are a normal part of running a business. How they are handled can affect cash flow, customer experience, support workload, dispute exposure, and reporting accuracy.

In practice, the term payment reversal covers several different situations where a transaction is canceled or funds move back to the customer. Merchants usually deal with three main paths: authorization reversal, refund, and chargeback. The real challenge is not just understanding the term itself, but knowing which action applies at which stage of the payment flow.

In this guide, enterprise merchant payment teams will learn how each reversal type works, where it happens in the payment flow, how to choose the right response, and how to reduce avoidable issues such as payout mismatches and unnecessary operational friction. If your merchant team is already juggling multiple PSPs or acquirers, Akurateco’s payment orchestration platform with a payment monitoring system is the next logical step to centralize visibility before these issues turn into finance noise.

What Is Payment Reversal?

A payment reversal is the broad term for canceling a card-payment outcome or sending funds back through the payment flow. The important part is not just that money goes back. The important part is when it happens and who initiates it.

The same word “reversal” is often used loosely, so this article uses the three-type framework that matches what readers usually look for: authorization reversals, refunds, and chargebacks.

That distinction matters because each path creates a different operational outcome. One releases an authorization hold. One sends money back after processing. One starts with a dispute raised through the customer’s bank and can pull money plus fees back through the scheme flow. For product, ops, and finance teams, those are three very different workflows.

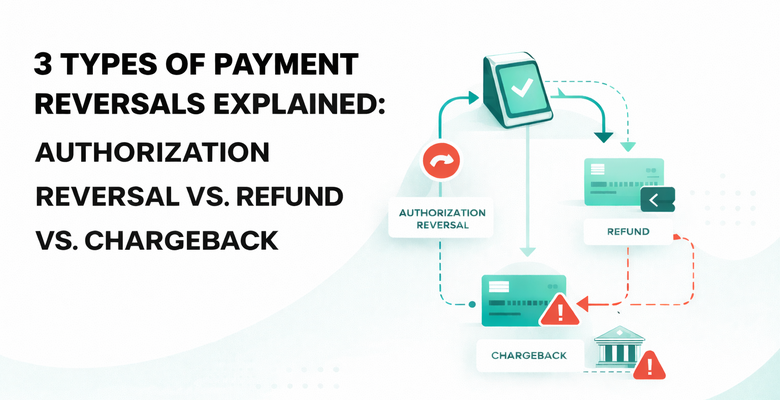

The 3 Types of Payment Reversals Explained

Not all payment reversals work the same way, even if they all seem to lead to the same outcome: money going back or a transaction being undone. The key difference is when the action happens and who initiates it.

Some reversals happen before the payment is fully completed, some after the transaction has already been processed, and others begin when the customer raises a dispute through the bank.

Understanding these three paths helps merchants choose the right response, reduce unnecessary costs, and avoid added friction for both customers and internal teams.

Authorization reversal (void transaction)

An authorization reversal is the right action when the payment was approved, but should not proceed to completion. Stripe describes it as canceling a pending transaction before it finalizes, with the business sending a reversal request to the issuer through the acquirer so the hold can be released. Visa is even more direct: authorization reversals notify the issuer that all or part of a sale was canceled and that the authorization hold should be released. This usually happens after authorization and before capture or later stages, such as clearing and settlement.

Common examples are out-of-stock orders, duplicate approvals, corrected amounts, customer cancellations caught early, and partial captures where the unused amount should be released rather than left hanging on the customer’s card.

This is also where teams need to remember that partial reversals exist. Visa notes that an authorization reversal can release all or part of the original hold. That matters when only part of the order ships or when the final amount is lower than the original authorization. If the reversal is not sent correctly, Visa says the hold can remain outstanding for 1 to 8 days, which is exactly the kind of avoidable customer friction support teams hate.

Refund

A refund is what you issue after the payment has already been processed. At this point, you are no longer just releasing a hold. You are returning funds after the charge has gone past the pending stage.

This is the right path when the customer has returned the goods, canceled the service after billing, or when the merchant agrees that the money should go back after the transaction has succeeded. It can be a full refund or a partial refund.

Timing varies by provider, payment method, and banking rails, so it is safer to describe refund timing as provider- and method-dependent rather than promise exact windows unless a specific provider flow is being documented.

Operationally, refunds are still cheaper and cleaner than disputes because the merchant remains in control. But they still affect downstream reporting because the refund often appears later than the original sale and may offset a later deposit rather than cleanly net against the original transaction date. That is one reason finance teams end up asking why today’s payout doesn’t match yesterday’s sales report.

Chargeback

A chargeback is the most expensive path operationally because it starts with a bank-side dispute, not a merchant action. Stripe’s disputes documentation explains that the issuer creates a formal dispute on the card network, which immediately reverses the payment and pulls the funds back, along with one or more dispute fees. Visa’s chargeback materials add the operational side: businesses then face extra fees, wasted time, more resources spent fighting disputes, and potentially reputational damage.

This is why a chargeback should never be treated as “just another refund.” With a refund, the merchant decides to return the money. With a chargeback, the bank-side process forces the issue, and the merchant moves into deadlines, evidence collection, case handling, and risk review. That is also where your chargeback ratio becomes important, especially for high-volume e-commerce and subscription businesses.

Along with this topic, it’s also useful to mention two related concepts briefly. One is friendly fraud, where a valid transaction is disputed by the cardholder anyway. The other is a retrieval request, which can arrive before or instead of a formal dispute in some flows and signals that more transaction information may be needed. These are early warning signs that your team needs standardized case handling, not ad hoc responses.

The Comparison of Authorization Reversal, Refund, and Chargeback

The three core payment reversals differ in who initiates them, when they happen, and how much work they create for support, product, and finance teams.

The table below follows the same source-backed distinction throughout this article: authorization reversals release a hold before completion, refunds return processed funds, and chargebacks reverse the payment through the issuer-led dispute process.

| Type | Who initiates | Timing in flow | Customer impact | Operational workload | The best next step |

| Authorization reversal (void) | Merchant side via acquirer to issuer | After approval, before capture/settlement | Hold is released faster; least friction | Low | Best when order is canceled early, amount is wrong, or auth is duplicate |

| Refund | Merchant | After capture and usually after settlement | Customer gets money back to original method | Medium | Best when merchant agrees money should be returned after the sale posted |

| Chargeback | Cardholder via issuer / bank-led process | After the sale is posted; often later than settlement and sometimes after payout | Customer may get temporary or final credit during dispute | High | Move immediately into dispute workflow, evidence gathering, and case tracking |

A simple rule of thumb works well for product teams and finance ops alike:

- Order canceled before it posts? Use an authorization reversal.

- Payment already posted, and you agree the customer should get money back? Use a refund.

- Customer went to the bank, or a formal dispute was filed? Treat it as chargeback handling, not as routine refund processing.

That logic becomes easier to enforce when routing, monitoring, and case management are centralized.

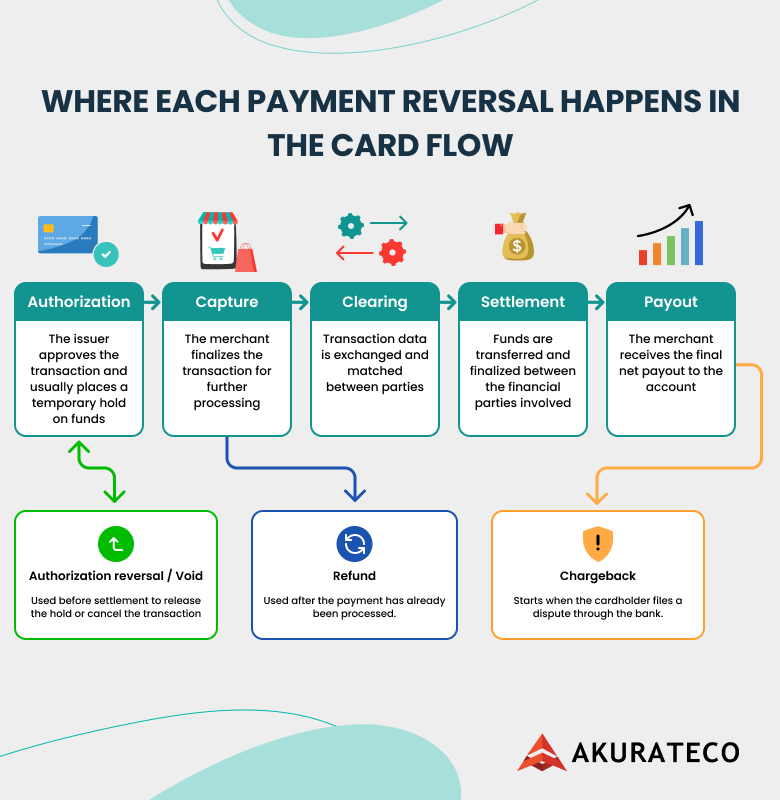

Where Reversals Happen in the Card Flow: The Timeline

Overlay the three reversal types on that timeline, and the logic becomes much easier to implement correctly.

- An authorization reversal sits after authorization but before capture/settlement are completed.

- A refund sits after the payment has been processed.

- A chargeback happens later, after the customer raises a dispute through the issuer, and the network-side workflow begins.

For teams that want the full background, learning how the payment settlement process works will help them understand the sequence cleanly: authorization is the approval stage and often only a hold, capture finalizes the charge, clearing matches transaction records between parties, settlement is the transfer of funds between institutions, and funding or payout is the actual deposit to the merchant bank account.

Reversals and Reconciliation: Why Your Payouts Don’t Match Sales

Refunds and chargebacks often appear later than the original transaction, which is why payouts don’t always match sales reports. A payment may be settled first, while the refund or chargeback shows up later as a negative adjustment in a future payout. That is where reconciliation becomes important.

To reconcile properly, merchants need to match the original transaction ID to the related refund or chargeback reference, segment the data by provider because each PSP may structure reports differently, and keep a separate reversal ledger with the payment ID, reversal type, amount, reason, and status. This makes it easier to trace adjustments, explain payout differences, and keep reporting accurate data across providers.

For a deeper look at how this works in practice, read Akurateco’s guides on payment reconciliation to fully understand the process.

How to Reduce Avoidable Payment Reversals: Practical Prevention Playbook

Not every payment reversal is a problem. Some are the correct outcome when an order is canceled, a return is approved, or a genuine dispute needs to be resolved.

The goal is not to eliminate reversals at all costs. The goal is to reduce the avoidable ones. These are the cases caused by operational gaps, poor communication, weak controls, or slow response. In practice, that means tightening the payment flow before issues happen, resolving customer friction earlier, and giving teams better visibility into where reversals, refunds, and disputes are coming from.

Reduce authorization reversals

Authorization reversals are often a symptom of something going wrong early in the order flow. They may happen because stock availability was inaccurate, the customer submitted the payment twice, the final amount changed after authorization, or the merchant approved a transaction that should not have moved forward. Some reversals are expected, but a high volume usually points to weak pre-fulfillment controls.

To reduce avoidable authorization reversals, merchants should improve inventory accuracy, add duplicate-payment prevention, and define clearer rules for when authorization should turn into capture. It also helps to review checkout and order-confirmation logic so payments are not approved too early in flows where cancellation is still likely.

Just as important, if a transaction is canceled, the reversal should be sent correctly and promptly rather than left to expire on its own. That reduces customer confusion and helps avoid unnecessary support contacts about funds that still appear blocked.

Reduce refunds

Refunds often start long before the refund request itself. In many cases, they are triggered by expectation gaps rather than payment failures: unclear product descriptions, unexpected delivery timelines, poor shipping visibility, confusing cancellation terms, or slow customer support. When customers do not understand what is happening, asking for money back becomes the easiest next step.

The best way to reduce avoidable refunds is to improve the customer journey before frustration builds up. Clearer product and pricing information, accurate delivery estimates, proactive order updates, and simple self-service cancellation or return flows all make a difference. Internally, merchants should also review refund patterns by product, provider, region, and support reason.

That helps identify where refunds are being driven by operational issues rather than genuine returns. Refunds will always remain part of doing business, but they should not become the default fix for poor communication or broken post-purchase processes.

Reduce chargebacks

Chargebacks require the strongest prevention strategy because they are the most expensive and disruptive outcome. Unlike refunds, they are no longer fully under the merchant’s control. Once the customer goes through the bank, the issue becomes a formal dispute that can bring added fees, evidence deadlines, extra workload, and pressure on chargeback ratios.

Reducing chargebacks starts with the basics: clear product information, recognizable billing descriptors, accessible customer support, and faster resolution when a customer raises a complaint. But strong prevention also depends on monitoring and process discipline. Merchants should track dispute patterns by provider, payment method, region, and reason code to spot recurring problems early. They should also use alerts, monitoring tools, and structured dispute workflows so teams can respond faster and more consistently.

Akurateco’s chargeback management service helps merchants move from reactive dispute handling to earlier issue detection. With better visibility across providers, teams can spot anomalies sooner, understand what is driving them, and stop more payment issues before they become chargebacks.

Another tool worth mentioning in this context is Chargeblast, a chargeback management platform that aggregates Ethoca and Verifi alerts to give merchants early warning of incoming disputes. When an alert comes in, merchants can issue a refund or cancel the order before it escalates into a formal chargeback, which keeps ratios down without requiring manual monitoring across separate alert programs.

For disputes that do go through, Chargeblast’s Recovery service handles the representment process end-to-end, building and submitting evidence packages on the merchant’s behalf to win back revenue from illegitimate chargebacks. It’s a practical option for subscription businesses and high-volume e-commerce operators where chargeback exposure is an ongoing operational concern rather than an occasional edge case.

Costly Mistakes Merchants Make With Payment Reversals

Payment reversals are not difficult only because there are several types. They become difficult when teams apply the wrong action, delay the correct one, or try to manage everything across disconnected systems. The most common mistakes usually come from timing, process gaps, and lack of visibility.

- Refunding when a void would have been cleaner. If the transaction is still authorized but not captured, a void or authorization reversal is usually cleaner than refunding later. Using a refund when an early reversal was still possible can create unnecessary accounting noise and a worse customer experience.

- Not sending authorization reversals. Leaving holds to expire naturally can tie up customer funds for days. Visa specifically says incomplete or mismatched reversal data can stop the issuer from matching the reversal to the original authorization, leaving the funds outstanding for 1 to 8 days.

- Treating chargebacks as just another refund. A refund is a merchant’s decision. A chargeback is an issuer-led dispute process that can reverse the payment and add dispute fees. The difference matters because the second path escalates into evidence handling, deadlines, and ratio risks.

- No single source of truth across PSPs. When refunds, disputes, and payout adjustments are split across multiple dashboards, reconciliation turns into manual detective work. That is exactly why orchestration and centralized monitoring matter in multi-provider setups.

Avoiding these mistakes starts with understanding where the transaction sits in the payment flow and making sure the right action, data, and visibility are in place before a simple issue turns into a larger operational problem.

Conclusion

Authorization reversals, refunds, and chargebacks are often grouped under the same broad topic, but they should never be treated as the same merchant action.

- Authorization reversal is the cleanest option when a transaction is still pending, and the hold needs to be released.

- Refund is the correct path once the payment has already been processed and funds need to be returned.

- Chargeback is a bank-led dispute workflow that brings the highest operational cost, from evidence collection to dispute fees and chargeback ratio exposure.

For merchants, the difference between these three paths affects far more than whether money goes back to the customer. It affects cash flow, reporting accuracy, support workload, settlement visibility, and financial control. The better your team understands when to use each option, the easier it becomes to reduce avoidable friction and manage payment operations more efficiently.

If your team handles reversals across several providers, Akurateco helps bring structure and visibility into the process. Instead of tracking refunds, disputes, and payout adjustments across separate PSP dashboards and reports, merchants get a more centralized view of payment activity, issue patterns, and operational impact. This makes it easier to investigate reversal drivers, follow disputes more consistently, and support reconciliation with less manual effort.

FAQ

What are the three types of payment reversals?

They are authorization reversals, refunds, and chargebacks. That is the framework used by major payment education content, and it maps cleanly to the real operational question teams face: do we release a hold, return processed funds, or handle a bank-led dispute?

What’s the difference between authorization reversal and refund?

An authorization reversal happens before the payment is fully completed and releases the authorization hold. A refund happens after the payment has already been processed and sends money back after the fact. Visa and Checkout.com both draw that line clearly.

Can customers initiate an authorization reversal?

Typically, no. The customer can ask to cancel the order, but the actual reversal is usually sent by the merchant through the acquirer to the issuer. That is why this is best treated as an ops and payment-flow decision, not a customer self-service dispute action.

Why are chargebacks more costly than refunds?

Because chargebacks add bank-side dispute handling on top of the funds reversal. That can include pulled-back funds, dispute fees, evidence collection, staff time, and pressure on your chargeback metrics. Visa also highlights the additional operational burden and reputational risk.

How do payment reversals affect reconciliation and reporting?

They often arrive later than the original sale and can appear as negative adjustments against later payouts, which is why payout totals stop matching gross sales reports. Akurateco’s settlement and reconciliation content explains that settlement, payout timing, and downstream adjustments need to be matched carefully across provider reports and bank deposits.

When should a merchant issue a refund to avoid a dispute or chargeback?

As soon as the payment has been processed and the merchant agrees, the customer should get the money back. Early, clear merchant-side resolution is often cheaper and less disruptive than letting the issue escalate into a formal dispute. This is also where chargeback alerts and a standardized dispute resolution cycle help teams act faster.