- What is the merchant onboarding process?

- Manual merchant onboarding VS automated merchant onboarding: Best practices

- Step-by-step: How merchant onboarding works

- What documents are required for a merchant onboarding?

- Compliance and fraud prevention in merchant onboarding

- Manual vs Automated Merchant Onboarding: When Each Approach Works

- How Akurateco Supports Merchant Onboarding

- FAQ

With online payments solidifying themselves as a vital part of our everyday lives, merchants are quickly adopting financial technology services. A crucial process that cannot be overlooked when searching for a payment solution is merchant onboarding. This process verifies merchants’ security and aims to allow them to accept payments for goods and services as quickly as possible. While this procedure is well known to every merchant who has partnered with a payment solution, there are various nuances affecting its efficiency.

In this article, we’ll explain what merchant onboarding is, how the process works, which documents businesses usually need to prepare, and how KYC, KYB, AML, and PCI DSS checks fit into the onboarding workflow.

What is the merchant onboarding process?

Merchant onboarding is the process through which payment software providers set up businesses to accept payments. It refers to the series of actions taken to register a merchant with a payment processor or acquirer.

When a merchant wants to accept payments for goods and services online by partnering with a particular payment system vendor, they need to undergo an onboarding process to ensure they are trustworthy and eligible to receive payments.

Manual merchant onboarding VS automated merchant onboarding: Best practices

There are two ways payment service providers (PSPs) and other fintech solutions handle merchant onboarding – manually or automatically. As your business scales and the number of merchants you work with grows, choosing between manual and automated onboarding becomes increasingly important.

Below, we break down the challenges of manual onboarding and explain how automation can streamline operations, improve efficiency, and elevate the merchant experience.

The pitfalls of manual merchant onboarding

There are several things you should take into account when onboarding merchants manually:

- Operational bottlenecks and resource strain.

Manual merchant onboarding requires merchants to send documents one by one to an account manager. As onboarding requests increase, your team either needs to scale, which is costly, or face delays that slow down operations and increase overhead.

- Slow approvals and poor merchant experience

High workloads, time zone differences, and limited availability often result in long wait times before merchants can start accepting payments. These delays harm the first impression and may cause merchants to lose confidence in your service early on.

- Scattered communication and disorganized data

With files shared across emails and messengers, onboarding data becomes fragmented. Your team must manually collect and input everything into your system, a process that’s inefficient and prone to errors, especially when dealing with multiple merchants at once.

The case for automated merchant onboarding

Now that we’ve covered the manual merchant onboarding process, let’s move on to automated merchant onboarding.

What is automated merchant onboarding?

Automated merchant onboarding allows merchants to fill in application forms and upload all required documents directly within a vendor’s platform, at their own pace and convenience. This significantly cuts down on unnecessary communication and accelerates the entire onboarding process. The goal? To reduce friction, save time, and help merchants start accepting payments faster.

Here’s how it helps payment service providers:

- Merchants onboard themselves

With automation, merchants can begin the process directly from your website and follow step-by-step instructions without waiting for a representative. In many automated onboarding systems, merchants can also access documentation, track progress, and complete technical setup steps without waiting for every action to be handled manually.

- Operational efficiency for PSPs

Your team’s role shifts from performing manual tasks to monitoring merchant progress, reviewing submitted data, and supporting where needed. With automation, a task that used to require a dedicated team of three can now be handled by one employee. Notifications help your team stay updated on merchant status without constant follow-up.

- All data in one place — no CRM needed

Automated platforms consolidate all onboarding information into one centralized system, such as a Merchant Card. This removes the need for external CRM tools and ensures all required data is easily accessible in one place.

- Customization and scalability

Advanced systems also allow PSPs to tailor onboarding forms based on the merchant’s country of incorporation or business model. For example, onboarding forms can be adjusted based on the merchant’s country, business model, risk profile, or required compliance checks.

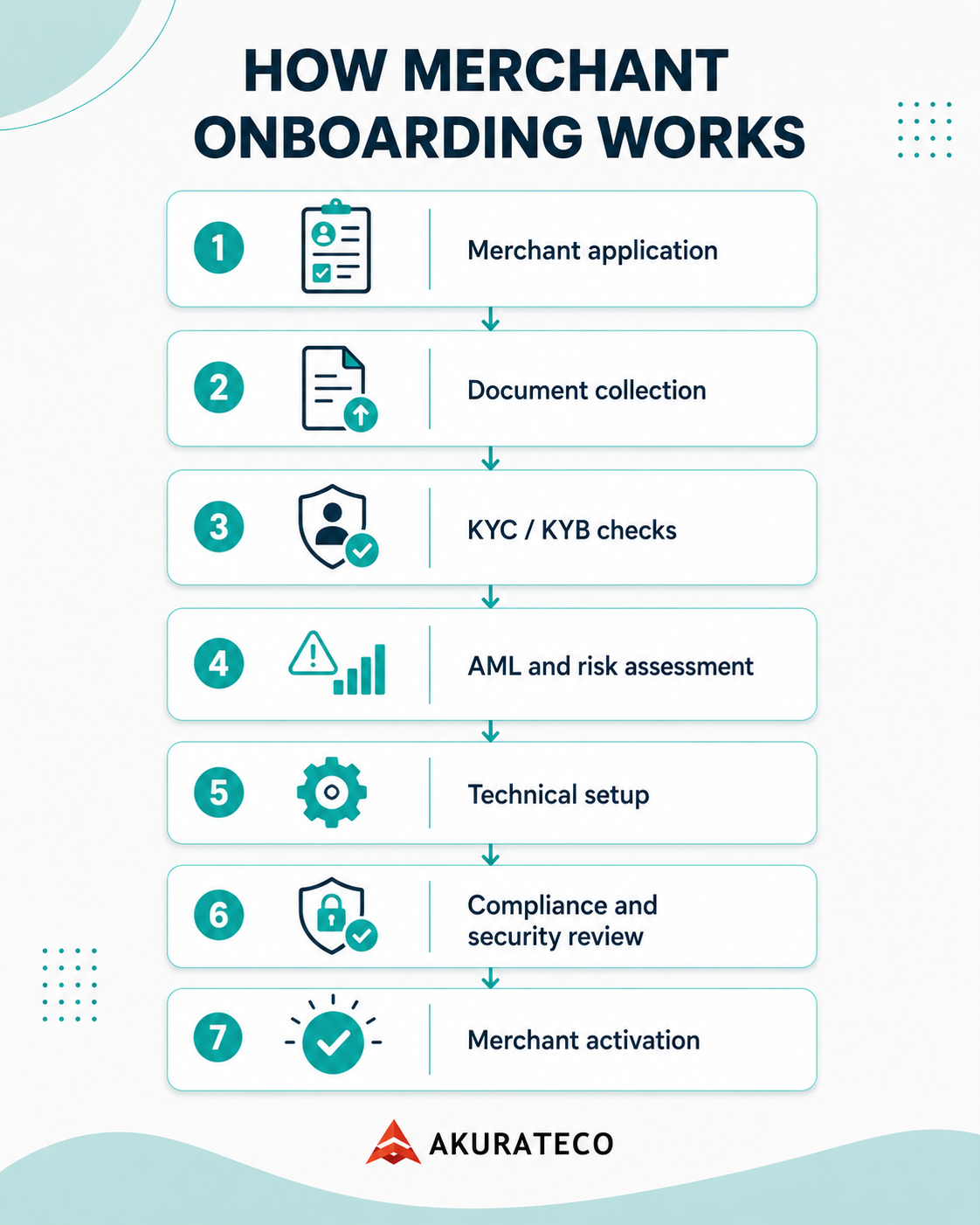

Step-by-step: How merchant onboarding works

The merchant onboarding process may vary by region, provider, business model, and risk level. However, most payment providers follow a similar workflow.

Step 1. Merchant application

The merchant submits an application with basic business information, including company name, registration details, website, business model, expected transaction volume, and payment processing needs.

Step 2. Document collection

The provider collects the documents required to verify the merchant. These may include business registration documents, proof of identity, proof of address, bank account details, ownership information, financial statements, and previous processing history.

Step 3. KYC and KYB verification

The provider verifies the identity of business owners and checks whether the company is legally registered and legitimate. KYC focuses on the people behind the business, while KYB focuses on the business itself.

Step 4. AML and sanctions screening

The merchant, beneficial owners, and related entities may be checked against anti-money laundering, sanctions, politically exposed persons, and adverse media databases.

Step 5. Risk assessment

The provider evaluates the merchant’s risk level based on industry, geography, transaction volume, chargeback history, business model, products or services, and expected payment behavior.

Step 6. Technical setup

The merchant receives the required payment setup, which may include API credentials, hosted payment page access, plugin configuration, test environment access, or other integration options.

Step 7. Compliance and security review

The provider checks whether the merchant meets relevant compliance and security requirements. For online card payments, this may include PCI DSS-related checks, website review, checkout security, refund policies, and terms and conditions.

Step 8. Approval and activation

Once verification, risk review, technical setup, and compliance checks are complete, the merchant account is approved and activated. The merchant can then start accepting payments.

What documents are required for a merchant onboarding?

Having all the necessary documentation in advance will save businesses a lot of time during the merchant onboarding process.

Here’s what to prepare:

- Business license – proves that the business is legally registered.

- Tax Identification Number (TIN) – for tax purposes.

- Bank account information – connects the merchant’s bank account to the payment processing system.

- Proof of identity – a government-issued identification number (ID) of the business owner.

- Proof of address – utility bills or other documents showing the business’s physical address.

- Financial statements – recent bank statements or financial records confirming business financial health.

- Ownership information – details about business ownership.

- Payment processing history – if businesses switch providers, previous payment processing statements may be required.

- Compliance certificate – any relevant compliance certifications, such as PCI DSS (if necessary).

You might also like:

Compliance and fraud prevention in merchant onboarding

As one of the main goals of merchant onboarding is to ensure businesses’ security, maintaining compliance with security standards and regulations is vital. In addition to PCI DSS compliance, companies must also adhere to KYC and KYB requirements. If you need a deeper explanation of payment security requirements, read our guide to PCI DSS compliant payment gateways.

Let’s explore KYC and KYB requirements in detail.

Know Your Customer

KYC is a regulation requiring businesses to verify their customers’ identities. It is used by Payment Service Providers (PSP), payment software vendors, banks, and other financial institutions. The main purpose of KYC is to prevent payment fraud, including money laundering, terrorist financing, and other illegal activities. Based on the KYC check results, the company’s application will be either approved or declined. However, legitimate businesses have no need to worry. They will pass the KYC check, which they should become accustomed to, as it will be conducted not only during merchant onboarding but also regularly after.

Know Your Business

Know Your Business (KYB) deals with the same issue but for businesses. It aims to secure financial technology and financial services companies from merchant-initiated fraud. As a part of KYB, they need to confirm the legitimacy of businesses, their registration licenses, proof of stakeholders’ identities, and compliance with anti-money laundering legislation.

A basic KYC/KYB review usually includes:

- Verifying the legal business name and registration number.

- Checking the company’s country of incorporation and operating address.

- Identifying directors, shareholders, and ultimate beneficial owners.

- Collecting proof of identity and proof of address for relevant individuals.

- Reviewing the merchant’s website, products, services, pricing, refund policy, and terms and conditions.

- Screening the business and related individuals against AML, sanctions, and high-risk databases.

- Assessing the merchant’s industry, geography, transaction volume, and chargeback risk.

- Deciding whether the merchant can be approved, rejected, or sent for enhanced due diligence.

After conducting the necessary due diligence, payment providers and financial institutions can assess the risks associated with partnering with particular businesses and make an informed decision.

Manual vs Automated Merchant Onboarding: When Each Approach Works

Manual onboarding may work for small teams that onboard only a limited number of merchants and can review every application individually. However, it becomes harder to manage as application volume grows, documents arrive through different channels, and compliance checks become more complex.

Automated merchant onboarding is usually more suitable for PSPs, payment platforms, acquirers, and fintech companies that need a structured, repeatable process. It helps centralize applications, documents, KYC/KYB data, risk checks, and approval statuses in one workflow.

How Akurateco Supports Merchant Onboarding

Akurateco helps PSPs and payment businesses manage merchant onboarding as part of a broader white-label payment infrastructure. Instead of handling every application manually, teams can centralize merchant data, documents, verification steps, and approval workflows in one system.

To learn more about Akurateco’s product capabilities for merchant management and onboarding, visit the Admin Panel page.

FAQ

What is the merchant onboarding process?

Merchant onboarding definition is a procedure through which PSPs, payment software vendors, banks, and other financial institutions set up merchants to accept payments.

What is the purpose of merchant onboarding?

Merchant onboarding aims to verify the legitimacy and security of businesses with which payment solution providers are about to partner. Without it, vendors cannot activate merchants in their systems, and they will not be able to accept payments for goods and services.

What are KYC and KYB, and their roles in merchant onboarding?

Know Your Customer (KYC) is a verification process that ensures the customers behind the business are trustworthy. Know Your Business (KYB) confirms the business’s legitimacy and compliance with regulations. Verifying customers and businesses through KYC and KYB helps prevent fraud, money laundering, and other illicit activities.

Do merchant onboarding processes differ for high-risk and low-risk businesses?

Yes. High-risk businesses typically face more rigorous examinations. This may include additional documentation and enhanced due diligence checks to mitigate potential risks. Low-risk businesses usually face a simpler, faster onboarding process with fewer requirements.

How long does the merchant onboarding take?

The merchant onboarding process duration varies from one payment solution provider to another. Typically, it takes from a few days to a couple of weeks. The exact time depends on whether the onboarding is handled manually or automatically, the complexity of the business itself, the thoroughness of the verification checks, etc.

How to streamline merchant onboarding?

To streamline merchant onboarding, businesses can partner with payment software providers offering automated merchant onboarding technology. Designed to speed up time-consuming merchant onboarding, it allows businesses to onboard on their own terms and on their own schedule.