- What is real-time risk monitoring in payments?

- Where AI fits in the real-time payment lifecycle

- Reference architecture for AI risk monitoring

- The controls matrix (non-negotiable)

- Real-time actions that actually move the needle

- Real-time payments rails and why risk is harder now

- MLOps and governance: how to ship safely

- Metrics and measurement framework

- Conclusion

- FAQ

Modern payment systems operate under extreme pressure: every transaction must be approved or declined in milliseconds, yet every wrong decision directly impacts revenue, fraud losses, or customer experience.

The rapid growth of instant payment rails and increasingly sophisticated fraud and scam patterns has made this challenge even sharper. Decisions can no longer rely on static rules or delayed analysis. Instead, platforms must evaluate risk continuously and act immediately.

This is where AI enhancing real-time risk monitoring in payments becomes essential. At the same time, AI in real-time payments risk assessment is not just about detecting fraud—it is about balancing risk, approvals, and user friction in real time.

In practice, modern systems follow a continuous loop: signals are streamed, enriched with context, scored using machine learning models, and passed into a decision engine that triggers specific actions such as approval, step-up authentication, rerouting, or retries.

In this article, you will get a practical blueprint of how this works in real systems: architecture, controls, actions, and measurement.

What is real-time risk monitoring in payments?

Real-time risk monitoring is the continuous evaluation of transactions and user behavior at the exact moment a payment is initiated, allowing platforms to make immediate decisions before funds move or settle.

It differs from traditional fraud systems in both timing and scope. Monitoring is about collecting and analyzing signals, while decisioning is about choosing what to do with that information. Post-event processes, such as investigations, chargebacks, or compliance reviews, happen later and should not be confused with real-time controls.

In practice, risk checks are distributed across the payment lifecycle. Before authorization, systems may apply pre-authorization scoring based on user history and device signals. During authorization, the system must decide instantly whether to approve, decline, or challenge the transaction. After authorization, monitoring continues through AML processes and anomaly detection.

Real-time transaction monitoring plays a key role here, as it enables systems to track patterns across transactions, detect abnormal behavior, and feed that intelligence back into decisioning.

Where AI fits in the real-time payment lifecycle

AI is not a standalone module; it is embedded throughout the payment flow, supporting decisions at every stage.

Before a transaction even begins, AI helps assess onboarding risk, set limits, and evaluate identity using device intelligence and historical patterns. During the authorization phase, which is the most critical moment, machine learning models generate risk scoring outputs in milliseconds. These scores influence whether the transaction is approved, declined, or routed through additional authentication such as 3D Secure.

After the transaction, AI continues to provide value through AML monitoring, scam detection, and identification of suspicious behavioral patterns that may indicate account takeover or coordinated fraud.

Operationally, AI also improves internal workflows. It prioritizes alerts, reduces noise, and supports analysts through structured case management workflows. Instead of reviewing everything, teams focus only on high-risk cases with contextual insights.

This layered approach allows platforms to combine behavioral signals, velocity controls, and anomaly detection into a unified risk view.

Reference architecture for AI risk monitoring

A practical implementation of real-time risk monitoring relies on a modular, event-driven architecture designed for low latency and high throughput.

Everything starts with data sources. Payment gateways, issuers, merchants, and device-level signals continuously generate events. These events are ingested into a streaming data pipeline, where they are processed in real time. The system enriches each event with additional context, such as geolocation, prior transaction history, or merchant risk profiles.

A feature store plays a central role by ensuring that both training and inference use consistent, up-to-date data. This is critical for avoiding discrepancies between model behavior in development and production.

Model serving components then generate predictions in milliseconds. These predictions typically include fraud probability, behavioral anomaly scores, or scam likelihood indicators.

The outputs are passed into a payment decisioning engine, which combines machine learning signals with business rules, compliance requirements, and risk thresholds. This is where final decisions are made.

What makes this architecture powerful is the action layer that follows. Decisions are not just logged—they trigger real actions such as approvals, declines, authentication steps, or orchestration logic like routing and retries.

Finally, observability and governance layers ensure that every decision is traceable. Audit trails, explainability tools, and feedback loops allow teams to understand outcomes and continuously improve models through MLOps practices.

The controls matrix (non-negotiable)

Even the most advanced AI models cannot replace foundational controls. A robust system combines machine learning with deterministic safeguards.

Velocity controls and spending limits protect against rapid transaction bursts and high-value fraud attempts. Allowlists and denylists provide immediate filtering based on known entities such as risky geographies, merchants, or accounts.

Step-up authentication triggers ensure that high-risk transactions require additional verification, while retry caps prevent systems from unintentionally amplifying fraud through repeated attempts.

Equally important are fail-safe mechanisms. If a model becomes unavailable or behaves unexpectedly, the system must fall back to predefined rules to maintain stability.

Finally, audit trail requirements are critical in regulated environments. Every decision must be recorded with sufficient detail to support compliance, dispute resolution, and internal reviews.

Real-time actions that actually move the needle

The true value of AI in payments comes not from detecting risk, but from acting on it correctly.

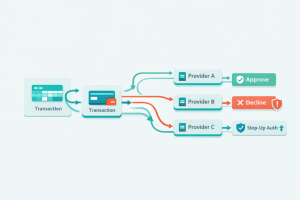

Routing optimization allows platforms to dynamically select the best payment route based on both performance and risk signals. This means avoiding routes with high fraud exposure while maximizing approval rates through issuer and BIN-level insights.

Retry logic adds another layer of intelligence. Instead of blindly retrying failed transactions, systems can identify which declines are recoverable and apply timing strategies that increase the chance of success without introducing additional risk.

Cascading payments extend this concept by enabling controlled failover between providers. If one route fails due to technical or risk-related issues, the system can seamlessly switch to another, preserving both revenue and user experience. More about it read here.

Step-up authentication decisions must also be carefully balanced. Overusing 3D Secure introduces friction and harms conversion, while underusing it increases fraud exposure. AI helps determine when authentication is necessary.

In some cases, the best action is to pause the transaction and trigger a manual review. This is especially relevant for complex scenarios such as scam detection or ambiguous behavioral patterns.

If you operate multi-provider payments, orchestration becomes the practical layer that translates risk signals into measurable business outcomes.

Real-time payments rails and why risk is harder now

Instant payment systems fundamentally change how risk must be managed.

Unlike traditional card payments, where settlement delays provide a buffer for review and intervention, instant payments operate continuously and settle almost immediately. This eliminates the window for manual checks and increases reliance on automated decisioning.

As a result, scam detection becomes significantly more important. Many fraud scenarios in instant payments involve authorized push payments, where users are manipulated into sending funds. Detecting these patterns requires behavioral analysis rather than simple rule-based checks.

This shift makes real-time architecture and pre-transaction controls essential components of any modern payment system.

MLOps and governance: how to ship safely

Deploying AI in payment systems requires careful governance to avoid unintended consequences.

One of the most effective approaches is shadow mode, where new models run alongside existing systems without affecting decisions. This allows teams to compare performance and validate improvements before full rollout. Champion-challenger strategies extend this idea by continuously testing alternative models.

Drift monitoring is another critical component. As fraud patterns evolve, models can become less effective. Continuous monitoring ensures that performance degradation is detected early and addressed through retraining or rollback.

Explainability and auditability are not optional in regulated environments. Systems must be able to explain why a decision was made and provide a complete history of inputs and outputs.

Success should not be measured by accuracy alone. The real goal is to increase fraud capture while reducing false declines and maintaining a high approval rate.

Metrics and measurement framework

A strong measurement framework connects risk decisions to business outcomes.

Approval rate reflects the system’s ability to process legitimate transactions successfully. False decline rate shows how often good customers are blocked, directly impacting revenue and user experience.

Fraud capture rate measures how effectively the system detects and prevents fraudulent activity, while alert-to-case time indicates operational efficiency in handling risk signals.

Recovery rate is particularly important in orchestration-driven systems. It shows how many failed transactions are successfully recovered through retries and cascading strategies.

Operational metrics such as analyst productivity and time-to-close cases provide additional insight into system performance beyond automated decisioning.

Latency must also be monitored closely, as real-time systems depend on strict timing constraints to function effectively.

Conclusion

AI in payments is not just about smarter detection—it is about building systems that can act instantly and intelligently.

When real-time architecture, machine learning, and orchestration are combined, payment platforms can reduce fraud, minimize false declines, and improve approval rates simultaneously.

This is what transforms risk management from a cost center into a growth driver.

FAQ

What is real-time risk monitoring in payments?

It is the process of evaluating transactions and behaviors at the moment they occur, allowing systems to make immediate decisions before funds are transferred or settled.

How does AI reduce false declines without increasing fraud?

AI analyzes a broader set of signals simultaneously, including behavioral, contextual, and historical data. This improves decision precision, allowing legitimate transactions to pass while still identifying fraudulent ones.

What latency budget is realistic for real-time risk scoring?

There is no universal number, but systems operate under very tight latency constraints. This requires optimized pipelines, efficient model serving, and minimal data transfer between components.

What is the difference between fraud prevention and AML monitoring?

Fraud prevention focuses on stopping unauthorized or risky transactions in real time. AML monitoring, on the other hand, analyzes transaction patterns over time to detect suspicious behavior related to financial crime and regulatory compliance.

Where do routing, retries, and cascading fit into risk assessment?

They are part of the execution layer. Once a risk decision is made, orchestration mechanisms such as routing, retries, and cascading determine how the payment is processed to maximize success while minimizing risk.

How should payment teams govern AI models?

Effective governance includes continuous monitoring for model drift, maintaining explainability, ensuring full audit trails, and using controlled rollout strategies such as shadow mode and champion-challenger testing.

What is different about instant payments risk?

Instant payments eliminate the delay between authorization and settlement, which removes the opportunity for manual intervention. This increases reliance on real-time decisioning and makes behavioral and scam detection much more important.

What is a payment decisioning engine?

It is the component that combines machine learning outputs, business rules, and compliance requirements to produce a final decision such as approve, decline, or step-up authentication.

How does a feature store improve risk scoring?

A feature store ensures that models use consistent and up-to-date data, reducing errors caused by mismatched or stale inputs and improving overall prediction quality.

What role does anomaly detection play in payments?

Anomaly detection helps identify unusual patterns that may indicate fraud or scams, especially in cases where predefined rules are insufficient.