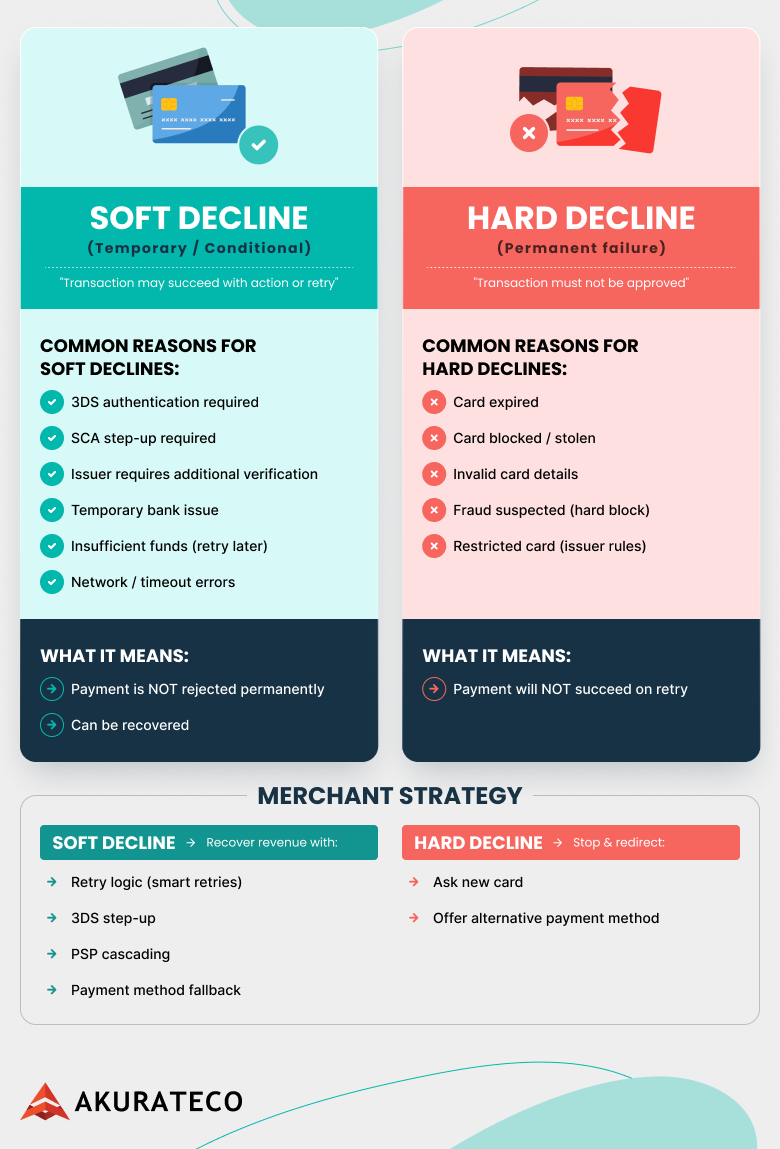

- What is a soft decline?

- Soft decline vs hard decline: what’s actually actionable

- The 5 most common soft decline buckets (and the right recovery move)

- Recovery tools: retries vs cascading vs routing

- Decline intelligence: why codes and advice matter

- How to build a soft decline recovery policy (playbook)

- Measurement: prove you’re recovering revenue (not just creating traffic)

- The Akurateco approach to soft decline recovery

- FAQ

- Conclusion: turn declines into recoverable revenue

Payment teams often assume that a declined authorization equals lost revenue. In practice, many failed transactions are temporary and recoverable when the right orchestration strategy is applied. A soft decline may indicate missing authentication, temporary issuer hesitation, or a short-lived processing issue rather than a final rejection.

The real problem is not the decline itself but how merchants respond to it. Without a structured framework, teams may launch uncontrolled retries, increase processing costs, and still fail to improve approval outcomes. Others miss recoverable transactions simply because they treat every decline the same way.

This guide explains what a soft decline is, how it differs from a hard decline, and how merchant-side payment teams can build a practical recovery playbook using retry logic, cascading payments, and payment routing. The goal is simple: help payment operations, product, and finance leaders recover revenue without increasing risk or friction.

What is a soft decline?

A soft decline is a temporary refusal from an issuer where the transaction may succeed later or under different conditions. Instead of signaling a permanent rejection, the issuer communicates that the payment could be approved if something changes such as adding authentication, adjusting timing, or routing through another provider.

The term soft decline is not standardized across all PSPs or acquirers. Some providers classify declines broadly, while others rely on specific decline codes or merchant advice codes to indicate whether a retry is recommended. Because of this variation, merchants should avoid relying solely on labels and instead analyze issuer feedback, performance data, and historical outcomes.

Common triggers include authentication requirements under PSD2 SCA, temporary issuer risk decisions, or network disruptions. In many orchestration environments, authentication-required responses are treated as recoverable events, which reinforces the idea that many declines are not final decisions.

Understanding how to interpret these signals is essential for building an effective payment recovery workflow.

Soft decline vs hard decline: what’s actually actionable

The difference between a soft decline vs hard decline determines whether a transaction should be retried, routed differently, or escalated to the customer. A hard decline usually indicates a final issuer decision, such as an invalid card, closed account, or permanent restriction. In these cases, retries rarely succeed and may even harm authorization performance.

A soft decline, by contrast, signals that a different approach may lead to approval. The challenge is identifying which actions are appropriate for each situation.

Teams that clearly distinguish between soft declines and hard declines reduce unnecessary retries and avoid additional fees that can occur when issuers detect repeated failed attempts.

The 5 most common soft decline buckets (and the right recovery move)

1. SCA or authentication required

Under PSD2 SCA, issuers may reject a non-authenticated authorization and request step-up authentication using 3D Secure (3DS). This scenario is one of the clearest examples of a recoverable soft decline.

Best action: trigger step-up authentication and retry the payment using a 3DS flow.

What not to do: repeat non-authenticated attempts, which can reduce issuer trust and lower approval probability.

2. Insufficient funds

Insufficient funds declines occur when the cardholder temporarily lacks available balance. These declines are often recoverable but require careful timing.

Best action: apply smart retries based on billing cycles, subscription schedules, or historical behavior.

What not to do: launch immediate retry loops that create unnecessary traffic and reduce conversion rate.

3. Generic issuer refusal do not honor

The “do not honor” issuer decline is one of the most ambiguous responses. While sometimes recoverable, it should not trigger automatic repeated retries without additional signals.

Best action: evaluate issuer history, adjust routing, or prompt the customer for an alternative payment method after repeated attempts.

What not to do: brute-force retries without changing authentication, routing, or timing.

4. Temporary processing issues

Temporary outages or network disruptions can result in short-term authorization failures. These situations are typically classified as recoverable events.

Best action: retry after a short delay or attempt a different route through another acquirer.

What not to do: run multiple immediate attempts that may increase processing load without improving approval rate.

5. Issuer risk or velocity limits

Issuers sometimes decline transactions due to velocity thresholds or perceived risk signals. These declines may still be recoverable when authentication or routing conditions change.

Best action: introduce step-up authentication or route through an acquirer with stronger issuer relationships for that region or BIN group.

What not to do: add unnecessary friction for trusted repeat customers or escalate to the customer too quickly.

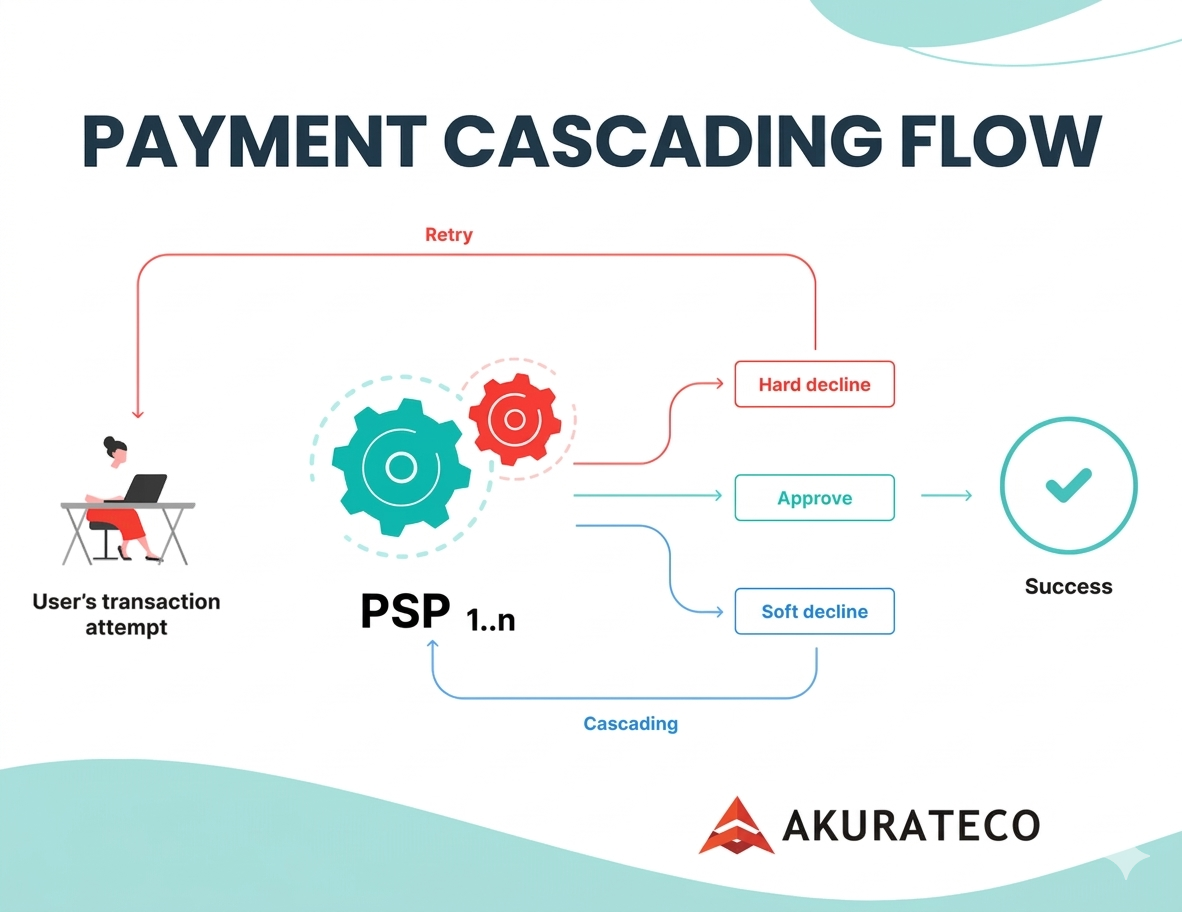

Recovery tools: retries vs cascading vs routing

Retry logic and smart retries

Retry logic works best when guided by issuer signals, decline codes, and historical performance data. Smart retries consider timing, authentication status, and route performance rather than simply repeating the same authorization request.

Payment networks and processors may impose penalties when merchants generate excessive retry traffic, so structured stop conditions are essential. Instead of relying on fixed retry counts, teams should evaluate advice codes, issuer behavior, and net revenue impact.

Cascading payments in multi-PSP environments

In a multi-PSP setup, cascading payments allow a transaction to move from one provider or acquirer to another when the initial route fails. This strategy is especially useful when declines are route-specific rather than issuer-driven.

Cascading must be used responsibly. Merchants should avoid attempting to route around a true hard decline, as this can increase costs and reduce issuer confidence.

Learn more about cascading payments and revenue growth

Payment routing and routing optimization

Payment routing determines which acquirer or provider handles an authorization attempt. Routing optimization analyzes geography, issuer behavior, provider performance, and payment method fit to improve approval outcomes.

Advanced orchestration platforms adjust routing dynamically based on performance data, which helps merchants recover declined payments without adding friction for the customer.

Explore Akurateco’s routing guide for more details

Decline intelligence: why codes and advice matter

Effective recovery starts with accurate classification. Decline codes originate from issuers, networks, or processors, and their meaning may vary between providers. Merchant advice codes, when available, offer additional guidance on whether a retry is recommended or discouraged.

Advanced payment teams rely on raw acquirer response data internally to understand issuer intent. However, these technical responses should never be exposed directly to shoppers, as they can create confusion and undermine trust.

By combining issuer signals with orchestration rules, merchants improve reason accuracy and reduce unnecessary retries that increase costs without improving approval rate.

How to build a soft decline recovery policy (playbook)

A structured payment recovery framework aligns payment operations, engineering, and finance teams around consistent decision-making. Instead of reacting to declines individually, organizations should define clear rules for when to retry, when to cascade, and when to involve the customer.

Checklist for building a recovery policy:

- Classify declines into actionable and non-actionable categories using issuer signals and analytics

- Define retry schedules tailored to each decline bucket

- Establish cascading rules for multi-PSP orchestration

- Define when to request customer action and how to communicate it clearly

- Implement centralized logging to track recovery outcomes and approval trends

Strong policies also reduce involuntary churn in subscription businesses by recovering payments before billing cycles fail.

For additional context on failed transactions and prevention strategies

Measurement: prove you’re recovering revenue (not just creating traffic)

Recovery initiatives must be evaluated through measurable business impact. Without proper analytics, merchants may generate additional authorization attempts without improving net revenue.

Key metrics to monitor include:

- Recovery rate by reason bucket

- Recovery rate by retry attempt number

- Approval lift by provider or route

- Net revenue after fees, including the impact of excessive retry fees

- Changes in conversion rate and authorization performance

Teams should also monitor issuer behavior by BIN group and track how routing adjustments influence approval outcomes over time.

The Akurateco approach to soft decline recovery

Akurateco helps payment teams orchestrate declines through configurable workflows instead of rigid rule sets. By combining retries, routing optimization, and cascading payments in one environment, merchants can adapt to issuer behavior without increasing operational complexity.

Key capabilities include:

- Configurable retry orchestration aligned with issuer signals and advice codes

- Built-in cascading logic designed for multi-acquirer strategies

- Unified analytics dashboards that reveal performance across providers and routes

For more context on PSD2 SCA and authentication flows

FAQ

What is a soft decline?

A soft decline is a temporary refusal where the transaction may succeed later, after authentication, or through another routing strategy.

Soft decline vs hard decline: can I retry?

Retries are often effective for soft declines but rarely succeed for hard declines, which typically require updated payment details or a new method.

How do I handle authentication required soft declines?

Trigger a step-up 3D Secure (3DS) flow and retry the authorization with authentication data included.

How many retries is too many?

There is no universal limit. Merchants should follow processor guidance, analyze issuer signals, and stop retries when success probability decreases or costs rise.

When should I use cascading payments vs retry logic?

Use cascading when the failure appears route-specific or provider-related. Use retries when issuer signals suggest a temporary refusal that may succeed later.

Conclusion: turn declines into recoverable revenue

Many payment failures are not permanent. By distinguishing between soft declines and hard declines and applying structured orchestration strategies, merchants can recover revenue that would otherwise be lost.

A balanced combination of retry logic, routing optimization, and cascading payments allows payment teams to improve approval rate while maintaining a smooth customer experience. Success depends on accurate decline intelligence, responsible retry strategies, and strong analytics that measure real business impact.

Ready to improve your approval performance? Request a demo with Akurateco and build a data-driven decline recovery strategy tailored to your payment flows.