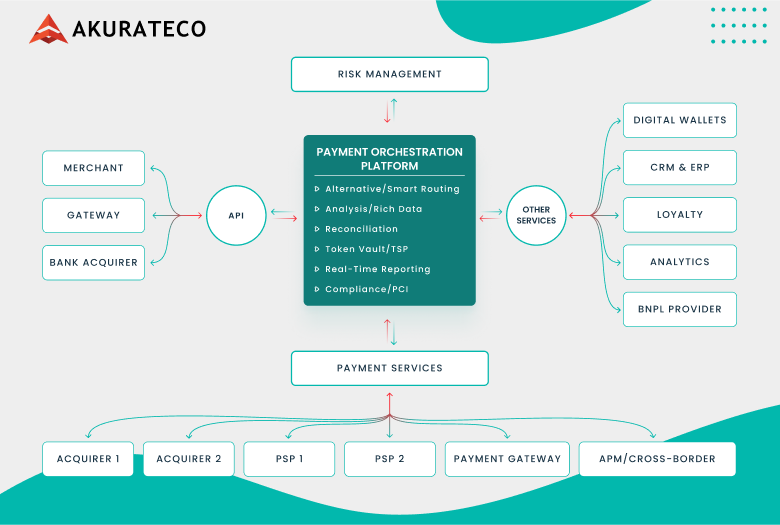

A payment hub is a central software layer that manages multiple PSPs, acquirers, and payment methods, providing unified reporting and operational control. It helps payment teams manage routing, retries, cascading, reconciliation, and provider performance without hardcoding every payment decision into the product.

Top payment hub platforms and solutions in 2026 should be compared by fit, not generic popularity. Some buyers need enterprise payment orchestration. Others need a PSP-led setup with one primary processor. PSPs and fintech operators may need a white-label payment hub they can brand and operate as their own. Akurateco’s payment orchestration platform fits into the payment hub category for businesses that need routing, retries, cascading, multi-provider control, and centralized reporting in one operational layer.

This guide gives you a shortlist by category of the top payment hub platforms and solutions in 2026, a practical comparison table, and a selection checklist. Save it to use later when comparing platforms for your business needs and requirements.

What to Look for in a Payment Hub

A strong payment hub should give you more control over providers, routing, retries, reporting, compliance workflows, and deployment choices.

Use these criteria when comparing the top payment hub platforms and solutions in 2026:

- Multi-PSP connectivity and connector roadmap. Check whether the platform supports the PSPs, acquirers, APMs, and local payment methods you need today, plus the markets you may enter in the next 12 months.

- Routing optimization. Look for smart routing by BIN, geography, payment method, amount, currency, transaction type, provider performance, and business rules.

- Retry logic and stop conditions. Strong payment hub software should provide intelligent retry and let you control retry timing, retry limits, decline-code logic, and stop rules to avoid unnecessary or risky payment attempts.

- Cascading and failover. Cascading should help recover eligible failed transactions by sending them to another provider route. Failover should support continuity when a provider is unavailable.

- Reporting, settlement visibility, and reconciliation support. The platform should normalize transaction data and help finance teams track payment statuses, settlements, provider performance, and reconciliation gaps.

- RBAC, approvals, and audit logs. Enterprise teams need role-based access control, approval flows, and audit logs so that routing rules and payment settings are changed with clear accountability.

- Compliance posture and PCI shared responsibility. Review the vendor’s PCI DSS status, security documentation, audit readiness, and how compliance responsibilities are split between the vendor and your team.

- Deployment options. Compare SaaS, on-prem, cloud hosting, data residency, and infrastructure ownership requirements before choosing a payment hub platform.

Top Payment Hub Platforms and Solutions in 2026: Shortlist by Category

The right payment hub is not the most popular vendor; it is the platform type that matches how your business manages providers, routing, reporting, compliance, and infrastructure ownership.

Payment hub software usually falls into three practical categories: independent orchestration platforms, PSP-led hub offerings, and white-label payment hubs. Each solves a different buyer problem. Enterprise merchants usually care about multi-provider control and payment performance. Smaller or less complex businesses may prefer one primary processor with some hub-like features. PSPs, fintechs, and acquirers often need branded infrastructure they can operate as their own payment platform.

Enterprise orchestration and payment hub platforms

Enterprise orchestration and payment hub platforms help payment teams manage several PSPs, acquirers, payment methods, regions, and business entities from one place. They sit between the merchant platform and the provider network, giving teams more control over routing, retries, cascading, reporting, reconciliation, and provider performance.

Best for: Enterprise merchants, marketplaces, platforms, and payment teams that already work with several PSPs or plan to expand payment processing across markets.

Strengths: The main advantage is control. Instead of sending transactions through one fixed route, teams can route payments based on BIN, geography, payment method, amount, currency, issuer behavior, risk signals, provider performance, or cost.

Trade-offs: Enterprise orchestration needs clear ownership. Your team still has to define routing rules, retry limits, fallback logic, reporting needs, approval workflows, and compliance responsibilities.

The table below is not a ranking. It lists relevant brands buyers may compare when evaluating enterprise payment orchestration, payment hub software, routing, provider connectivity, reporting, and multi-PSP control.

Brand | Why buyers may compare it | Best-fit context |

Akurateco | Payment orchestration platform with 650+ integrations, smart routing, cascading, provider connectivity, and automated reporting/reconciliation features. | Businesses that need a payment hub plus orchestration layer for multi-provider control, routing, retries, cascading, and centralized reporting. |

IXOPAY | Payment orchestration, tokenization, and payments intelligence platform with smart routing, automated reconciliation, and broad acquirer/payment method connectivity. | Enterprise merchants and platforms that need orchestration, tokenization, reporting, and reconciliation across multiple providers. |

ACI Worldwide | Payments orchestration platform positioned around centralized merchant payments, acquirer-agnostic processing, smart routing, fraud prevention, and enterprise-grade scalability. | Large enterprises, financial institutions, and merchants that need mission-critical payment software and broad payment ecosystem coverage. |

Spreedly | Open payments platform with orchestration pillars for connectivity, vaulting, optimization, fraud/authentication, and centralized management/reporting. | Merchants, marketplaces, and platforms that want flexible payment connectivity, vaulting, routing, and payment operations visibility. |

paytech | White-label gateway and payment orchestration technology with one unified API, intelligent routing, centralized management, and hundreds of PSP/payment technology integrations. | PSPs, fintechs, and payment businesses that need orchestration plus white-label or financial management capabilities. |

Gr4vy | Payment orchestration platform with routing, tokenization, workflows, analytics, fraud prevention, and payment method connectivity. | Enterprise merchants and platforms that want cloud-based orchestration, no-code workflow control, and provider-agnostic payment infrastructure. |

DECTA | Payment orchestration capability built into DECTA’s white-label payment gateway, with provider management, intelligent routing, failover, retries, fraud management, and reporting. | PSPs, ISOs, marketplaces, and enterprise merchants using or considering a gateway-centered orchestration model. |

Solidgate | Payment platform with orchestration, intelligent payment routing, provider-agnostic vault, multiple connectors, analytics, reconciliation, and payment infrastructure tools. | Fast-scaling digital businesses that want orchestration combined with payment infrastructure, routing, analytics, and recovery tools. |

White-label payment hub platforms

White-label payment hub platforms are designed for companies that want to offer payment services under their own brand. Instead of only optimizing merchant-side payments, they provide the operational control plane behind a branded payment business.

Best for: PSPs, fintech companies, acquirers, banks, merchant referral partners, and payment businesses that need branded infrastructure for merchant management, transaction monitoring, routing, reporting, onboarding, and payment operations.

Strengths: The main strength is faster infrastructure launch. A white-label payment hub can support merchant onboarding, transaction management, payment pages, routing, retries, cascading, reporting, and administrative controls without requiring the business to build every component internally.

Trade-offs: White-label infrastructure still requires business responsibility. The buyer needs to manage the commercial model, provider contracts, merchant support, risk workflows, and compliance obligations.

This table is meant to guide category comparison, not rank providers. It highlights platforms that enable companies to build, brand, and run their own payment services with capabilities such as merchant management, provider connectivity, routing, reporting, and gateway infrastructure.

Brand | Why buyers may compare it | Best-fit context |

Adyen | Global payments platform with optimization tools such as intelligent routing and auto retries | Enterprises that want one major global processor with strong acceptance optimization |

Stripe | Payments platform with optimized checkout, adaptive acceptance, retries, and broad developer tooling | Digital businesses that value developer experience and fast payment method rollout |

Checkout.com | Modular payment platform with Intelligent Acceptance, dynamic routing, smart authentication, and retries | Enterprise merchants that need processor-led performance optimization |

Worldpay | Global payment provider with payment optimization and dynamic routing capabilities | Large merchants that need global processing plus routing and optimization support |

PayPal Braintree | End-to-end payment platform supporting cards, wallets, PayPal, local methods, and vaulting | Businesses that want PayPal network reach plus card and wallet acceptance |

Fiserv Carat | Omnichannel commerce platform with payment optimization, control center, and payment engine features | Large retailers and enterprises with omnichannel commerce needs |

Nuvei | Payment platform with smart routing, cascading, retries, monitoring, and global payment coverage | Businesses that need processing plus optimization across regions and payment methods |

Rapyd | Global payment acceptance platform focused on local payment methods and cross-border commerce | Companies expanding into international or alternative payment method-heavy markets |

dLocal | Payment platform for emerging markets with local payment methods, local processing, and reporting | Businesses entering Africa, Asia, and LATAM markets |

PayU | Global payment provider with regional payment acceptance and local market coverage | Merchants that want processor-led access to selected high-growth markets |

Where Akurateco Fits

Akurateco fits companies that need a payment hub and an orchestration layer with white-label capabilities for routing, retries, cascading, and centralized reporting.

Akurateco is relevant for buyers comparing top payment hub platforms and solutions in 2026 because it sits in the payment hub and payment orchestration category. It is designed for companies that need multi-provider control, payment routing, retries, cascading, transaction monitoring, and centralized reporting in one operational layer.

For PSPs, fintechs, and payment businesses, Akurateco can also support a white-label payment hub model with a branded control plane. For merchants and platforms, it can help centralize payment operations across providers and payment methods.

For compliance, Akurateco’s FAQ states that its system is PCI DSS Level 1 certified. SaaS clients are covered by Akurateco’s certification. For on-prem deployments, clients need their own PCI DSS certification, and Akurateco can assist with documentation and instructions for the QSA. Note that PCI DSS should be treated as a shared responsibility, not as a burden that disappears automatically.

Selection Checklist for Top Payment Hub Platforms and Solutions in 2026

The right payment hub should match your provider roadmap, routing needs, reporting requirements, deployment model, and compliance responsibilities.

A payment hub decision should start with operating requirements, not vendor demos. Before comparing platforms, define how your business needs to manage providers, payment methods, routing logic, data visibility, compliance ownership, and deployment constraints.

The questions below can help your team separate must-have capabilities from features that only look useful during evaluation:

- What providers and payment methods do we need now and in the next 12 months?

- Do we need multi-entity support across brands, business units, or geographies?

- What routing inputs do we need, such as BIN, amount, method, risk, geography, currency, or provider performance?

- How are retries and cascades governed, including limits, decline-code logic, timing, and stop rules?

- Can we export normalized transaction and settlement data for reconciliation?

- Do finance and operations teams get clear settlement visibility?

- What deployment model do we need: SaaS, on-prem, or cloud-specific hosting?

- What are the data residency requirements?

- What audit artifacts, logs, approval controls, and change history are available?

- What PCI DSS responsibilities stay with us, and what is covered by the vendor?

- How quickly can new PSPs, acquirers, and payment methods be added?

- Who owns the routing strategy internally: payments, product, risk, finance, or engineering?

Use this checklist as a practical filter before shortlisting vendors. A strong payment hub platform should not only connect providers; it should also give your team reliable control over routing, retries, settlement visibility, reconciliation, compliance workflows, and long-term payment infrastructure growth.

Key Takeaways

- A payment hub is the control layer for PSPs, acquirers, payment methods, routing, retries, cascading, and reporting.

- Enterprise orchestration platforms are best when the buyer needs multi-PSP control and advanced routing governance.

- PSP-led hub offerings are practical when the buyer wants one main processor and fewer vendor relationships.

- White-label payment hubs fit PSPs, fintechs, banks, and payment businesses that need a branded payment control plane.

- PCI DSS, audit logs, RBAC, deployment model, and data residency should be reviewed before commercial selection.

Conclusion

Top payment hub platforms and solutions in 2026 should be selected by operational fit, not by name recognition alone. The right choice depends on how your business manages providers, routing logic, reporting, compliance responsibilities, and deployment requirements.

If you need a payment hub with an orchestration layer and white-label capabilities for multi-provider control, retries, cascading, centralized reporting, and flexible deployment planning, Akurateco is a practical option to include in your evaluation.

FAQ

What is a payment hub?

A payment hub is a central software layer that manages multiple PSPs, acquirers, and payment methods, providing unified reporting and operational control over routing, retries, cascading, reconciliation, and provider performance.

What should you look for in a payment hub platform?

Compare multi-PSP connectivity and connector roadmap, routing optimization, retry and stop-condition logic, cascading and failover, reporting and reconciliation, role-based access and audit logs, PCI DSS posture, and deployment options.

What are the main types of payment hub platforms?

They generally fall into three categories: independent orchestration platforms, PSP-led hub offerings, and white-label payment hubs — each solving a different buyer problem.

What's the difference between a payment hub and a payment orchestration platform?

The terms overlap heavily; a payment hub is the control layer for managing PSPs, acquirers, methods, routing, retries, cascading, and reporting, and many orchestration platforms function as a payment hub with added white-label capabilities.

Is Akurateco PCI DSS compliant?

Yes. Akurateco's system is PCI DSS Level 1 certified. SaaS clients are covered by Akurateco's certification; on-premises clients need their own certification, and Akurateco can assist with documentation for the QSA.