As global e-commerce continues to grow, enterprise merchants are facing a new kind of payment challenge. It is no longer enough to simply accept cards, add a few local payment methods, and negotiate processing fees once a year. At enterprise scale, payments become a performance system.

Every failed authorization, poorly routed transaction, provider outage, fragmented report, or missing local payment option can affect revenue, customer experience, finance operations, and market expansion. A payment setup that worked well in one region or at one stage of growth can quickly become difficult to manage when the business starts adding more countries, more entities, more providers, more currencies, and more customer journeys. That is why more enterprise teams are paying attention to payment orchestration.

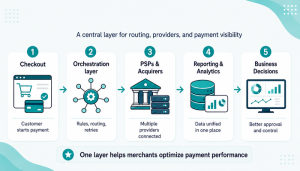

A payment orchestration platform gives merchants a centralized layer for managing payment providers, payment methods, routing logic, retries, fraud tools, tokenization, reporting, reconciliation, and operational workflows. Instead of maintaining separate integrations with every provider, merchants can manage more of their payment stack from one place.

In 2026, the payment orchestration market is becoming more competitive. Many platforms promise broader connectivity, smarter routing, easier provider switching, and better visibility. But the real question is not only which provider has the longest connector list. The more important question is which platform gives your business the right balance of flexibility, control, operational depth, and scalability.

This overview looks at 10 payment orchestration platforms enterprise merchants may compare in 2026. The goal is not to declare one universal winner, but to help payment, product, finance, and operations teams understand what each platform is likely to be good at and what they should validate before making a decision.

What to Look for in a Payment Orchestration Platform

Choosing a payment orchestration provider is not only a technical decision. It affects revenue performance, operational workload, compliance exposure, market expansion, and the way payment teams work day to day.

Here are the main areas enterprise merchants should compare first.

- Routing and Decisioning

Routing is one of the most important parts of payment orchestration. It decides where each transaction goes, when a fallback should happen, which provider should be tried first, and how different markets, currencies, BINs, card types, risk scores, transaction values, or customer segments should be handled.

At enterprise scale, basic routing is rarely enough. Merchants need logic that can support real business goals: improving approval rates, reducing unnecessary costs, avoiding provider downtime, supporting local acquiring strategies, and keeping payment performance stable across regions. The strongest platforms make routing transparent. Payment teams should be able to understand why a transaction was routed in a certain way, adjust rules safely, and monitor the impact of those changes. A good payment orchestration platform should not turn routing into a black box. It should give teams practical control over how payments move through the stack.

- Connector Coverage and Integration Depth

Most orchestration platforms promote the number of providers, acquirers, gateways, payment methods, and fraud tools they support. That number matters, but it is not the full story. A connector can be technically available but still limited in practice. It may not support all transaction types, currencies, refunds, recurring payments, chargebacks, 3DS flows, tokenization, reporting, or settlement formats in the way your business needs. For enterprise merchants, connector depth is often more important than connector count. Before choosing a platform, teams should validate their exact payment flows, not just the logo list.

- Scalability and Resilience

For enterprise merchants, payment infrastructure must remain stable during traffic peaks, provider outages, regional volume spikes, new product launches, and seasonal demand. A good orchestration platform should help reduce dependency on one provider and give teams more ways to keep payments running when something breaks. This includes failover logic, retries, provider health monitoring, and the ability to route around operational issues. The platform should also support the business as it expands into new markets, legal entities, currencies, and payment methods.

- Reporting and Operational Visibility

Payment performance is difficult to improve when data is fragmented across different providers and systems. Enterprise teams need one place to understand transaction performance, approval rates, declines, chargebacks, settlements, reconciliation issues, and provider-level behavior. Strong reporting is not only useful for payment teams. It also helps finance, risk, customer support, product, and leadership teams make better decisions. The best orchestration platforms do not simply process transactions. They help teams understand what is happening inside the payment stack and where performance is leaking.

- Tokenization and Credential Strategy

Tokenization is a major part of payment orchestration, especially for businesses with recurring payments, subscriptions, marketplaces, stored cards, or multi-provider strategies. Merchants should understand where payment credentials are stored, how portable tokens are, how provider switching works, and what happens if the business wants to migrate away from the platform later. A strong tokenization strategy can reduce lock-in and give merchants more flexibility. A poorly planned one can create future migration problems.

- Governance and Control

As payment operations become more complex, governance becomes essential. Enterprise teams need role-based access, audit logs, approval flows, safe rule changes, versioning, and rollback options. Without these controls, routing rules can become messy, production changes can create unexpected issues, and teams may lose confidence in the payment setup. Payment orchestration should make operations more flexible, but not uncontrolled.

- Deployment and Compliance Flexibility

Some merchants are comfortable with a SaaS-only model. Others need more control because of internal compliance requirements, data residency rules, enterprise procurement policies, or regional infrastructure needs. This is where deployment flexibility can become a major differentiator. For enterprise merchants, the best platform is not always the one with the most features. It is the one that fits the company’s technical, legal, operational, and commercial reality.

10 Top Payment Orchestration Platforms in 2026

The platforms below approach payment orchestration from different angles. Some focus strongly on routing and provider management. Others are more focused on tokenization, global acquiring, travel payments, low-code configuration, payment operations, or full payment infrastructure.

1. Akurateco

Akurateco is a white-label payment gateway and payment orchestration platform used by payment providers, fintech companies, acquirers, banks, and enterprise merchants. For merchants that want more than simple provider connectivity, Akurateco offers a broad infrastructure layer that combines orchestration, routing, cascading, risk tools, reporting, onboarding, and operational support.

Akurateco is especially relevant for enterprise merchants that want centralized payment control without building and maintaining the full infrastructure internally. It is also a strong fit for companies that need flexibility across markets, entities, providers, and deployment models.

While many orchestration platforms focus on one specific layer of the payment stack, Akurateco’s value is in combining several layers into one operating environment. For enterprise merchants, this can reduce the need to connect separate tools for routing, provider management, reporting, fraud control, merchant management, and payment operations.

Key capabilities

Akurateco offers a PCI DSS-compliant payment infrastructure with a large connector ecosystem, smart routing, cascading, transaction management, anti-fraud capabilities, tokenization, analytics, merchant management tools, and API access.

The platform supports payment orchestration across multiple providers and payment methods, helping merchants reduce dependency on a single PSP and create more flexible payment flows.

Akurateco also supports SaaS and more controlled deployment options, which can be important for enterprise merchants with stricter compliance, hosting, or data requirements.

Another important part of Akurateco’s positioning is operational support. The platform is not only software. It also gives businesses access to payment expertise, integration support, and infrastructure maintenance, which can be valuable for companies that do not want to expand internal payment engineering teams too aggressively.

Strengths

Akurateco stands out because it combines payment orchestration with a broader white-label payment infrastructure. For enterprise merchants, this can reduce the need to stitch together separate systems for routing, reporting, fraud, onboarding, and provider management.

Its smart routing and cascading capabilities are useful for merchants that want to improve approval rates, reduce failed transactions, and avoid dependency on a single PSP or acquirer.

The platform is also practical for businesses that need to launch or expand payment operations quickly while keeping more control over payment logic and provider strategy.

Akurateco can be especially useful for merchants that want:

- A centralized payment management layer

- More control over routing and cascading

- Multi-provider and multi-market flexibility

- A broad connector ecosystem

- White-label payment infrastructure

- Stronger visibility across transactions and providers

- Fraud and risk tools inside the same environment

- Operational support beyond basic software access

- Flexible deployment models

For enterprise merchants, Akurateco’s main advantage is that it can support both payment optimization and infrastructure ownership. This makes it relevant for companies that see payments not only as a processing function, but as a strategic part of revenue growth and operational control.

Considerations

As with any orchestration provider, merchants should validate the exact providers, regions, payment methods, and flows they need. Connector availability is important, but connector depth is what determines real production fit.

Akurateco may also be broader than what smaller merchants need. Its strongest value appears when payment complexity is already significant or when the business has clear plans to scale across providers, regions, and payment methods.

2. IXOPAY

IXOPAY is a payment orchestration platform focused on smart routing, tokenization, reconciliation, and payment intelligence for global businesses. It is often considered by merchants that want to centralize a complex payment stack while keeping provider flexibility.

IXOPAY is positioned around helping merchants manage multiple providers through one orchestration layer. It is especially relevant for businesses that want to reduce provider lock-in, standardize payment operations, and turn fragmented payment data into something more useful.

Key capabilities

IXOPAY offers payment orchestration through one API, with support for multiple acquirers, payment methods, routing logic, tokenization, reconciliation, and payment analytics.

The platform includes smart routing, automated reconciliation, payment method management, and tokenization capabilities. It also emphasizes payment intelligence, helping merchants analyze provider performance and make more informed payment decisions.

Strengths

IXOPAY is strong for businesses that want routing, tokenization, and reconciliation in one orchestration layer. Its focus on automated reconciliation and provider data normalization can be valuable for finance and operations teams.

It is also a good fit for merchants that already work with multiple providers and need a more structured way to manage them.

For enterprise teams, IXOPAY can be useful when the main goal is to bring order to a fragmented payment setup and create more consistent payment operations across providers.

Considerations

The implementation experience may depend on the merchant’s provider mix and the depth of specific connectors. Teams should also review how tokenization, data ownership, and migration would work in practice.

As with other enterprise-grade orchestration platforms, the most important validation step is not whether the platform supports a provider in general, but whether it supports the exact use cases, transaction flows, and reporting requirements the merchant needs.

3. Primer

Primer is a payment orchestration platform built around configurable payment workflows, routing, and optimization. It is often attractive to teams that want to change payment logic faster without relying on constant engineering releases.

Primer’s approach is especially appealing for product-led teams that want more control over the payment experience. Its workflow-based model helps teams configure payment logic, add services, and test new flows with less development effort.

Key capabilities

Primer provides a central layer for payment integrations, routing logic, workflow configuration, fraud tools, 3DS-related flows, tokenization, and payment optimization.

Its no-code workflow capabilities allow teams to configure payment flows, apply conditions, route to secondary processors, manage credentials, and gain visibility across payment providers.

Strengths

Primer is useful for product and payment teams that want more control over payment flows through configuration. Its workflow-first approach can help teams test and adjust payment logic faster.

For merchants with strong product teams, this can reduce the friction between payment strategy and engineering delivery.

Primer may be a good fit for businesses that want to experiment more actively with payment flows, payment services, 3DS logic, and checkout optimization.

Considerations

Primer’s value depends on how well its supported processors, payment methods, and operational tools match the merchant’s actual markets.

Enterprise teams should test monitoring, debugging, reporting, and governance controls before relying on it for critical payment flows. No-code payment configuration is powerful, but larger businesses still need strong control over who can change what, when, and how those changes are approved.

4. Spreedly

Spreedly is one of the more established platforms in the payment orchestration space, with a strong focus on vaulting, tokenization, and connecting merchants to multiple gateways and payment services.

Spreedly is often considered by businesses that want to reduce provider-specific logic and create more payment flexibility through a centralized platform.

Key capabilities

Spreedly helps businesses store payment credentials securely, connect to different providers, manage payment flows through a unified infrastructure layer, and gain a more holistic view of payment operations.

Its core value is often linked to payment method portability, tokenization, and reducing direct dependency on individual gateways.

Strengths

Spreedly is a strong option for merchants that care deeply about tokenization and gateway independence. It can help businesses reduce provider-specific code and create more flexibility when adding or switching payment providers.

It is especially relevant for merchants with stored payment credentials, recurring transactions, subscriptions, or long-term plans to diversify providers. For businesses that already have a payment strategy but need a better abstraction layer across providers, Spreedly can be a practical option.

Considerations

Spreedly may be less suitable for teams that want a highly opinionated, routing-first orchestration platform with deep operational tooling out of the box. Merchants should evaluate how much routing, reporting, reconciliation, and provider optimization logic they need beyond tokenization and provider abstraction.

5. Gr4vy

Gr4vy is a cloud-native payment orchestration platform designed to help merchants connect PSPs, payment methods, and fraud tools through one orchestration layer. It emphasizes configuration, speed, and operational flexibility.

Gr4vy is built for teams that want to add or change payment providers without rebuilding the checkout or creating new integrations each time.

Key capabilities

Gr4vy supports payment provider connectivity, payment method management, routing, anti-fraud provider activation, dashboard-based configuration, and payment flow optimization.

The platform is positioned as infrastructure-as-a-service for payments, giving merchants a universal integration to manage multiple PSPs and services.

Strengths

Gr4vy is useful for merchants that want faster payment configuration and less engineering dependency. Its dashboard-driven approach can be valuable when payment teams need to react quickly to provider performance, market needs, or payment method changes.

It is also relevant for businesses that prefer a modern cloud-native orchestration layer and want to keep control over provider strategy.

Considerations

A cloud-first model may not fit every enterprise requirement. Merchants with strict data residency, procurement, or deployment constraints should validate whether the architecture fits their internal policies.

Finance and operations teams should also test reporting, reconciliation, and transaction-level visibility to make sure the platform supports not only configuration, but also day-to-day operational control.

6. BR-DGE

BR-DGE is a payment orchestration platform that helps merchants, payment providers, and platforms connect payment providers, alternative payment methods, wallets, and fraud services through a single orchestration layer.

Its focus is on flexibility, modularity, and access to a broader payment ecosystem.

Key capabilities

BR-DGE offers payment orchestration, provider connectivity, access to payment services, reporting, payment method management, and modular orchestration capabilities.

The platform is positioned as a way for businesses to upgrade payment infrastructure through a single integration while keeping flexibility over the payment services they use.

Strengths

BR-DGE is a good fit for merchants that want a modular orchestration setup and prefer to choose the payment services they need rather than adopt a fully bundled payment stack.

Its ecosystem approach can be useful for businesses that want to experiment with different PSPs, wallets, alternative payment methods, and fraud tools while keeping a central control layer.

For merchants that want to avoid being locked into one provider strategy, BR-DGE can be an interesting option to evaluate.

Considerations

Merchants should validate the depth of the connections they need, especially for complex flows such as refunds, chargebacks, recurring payments, settlement reporting, and region-specific payment methods.

Because BR-DGE is modular, teams should also assess how much configuration and internal payment expertise they will need to get the most value from the platform.

7. CellPoint Digital

CellPoint Digital is a payment orchestration provider with a strong focus on travel, airlines, hospitality, and other complex enterprise payment environments.

It is designed for businesses that operate across regions, currencies, customer journeys, and multi-party payment flows.

Key capabilities

CellPoint Digital offers payment orchestration, intelligent routing, fraud logic, support for multiple payment methods, PSPs and acquirers, settlement-related capabilities, and architecture aimed at global enterprise operations.

Its platform is especially positioned around travel payment complexity, including offer, order, settle, and deliver flows.

Strengths

CellPoint Digital is particularly relevant for enterprise merchants in travel and hospitality, where payment flows are often more complex than standard e-commerce checkout.

It can be useful for businesses that need to optimize authorization, support many local payment options, and manage payments across different parts of the customer journey.

For travel companies, airlines, and hospitality businesses, this industry focus can be a major advantage.

Considerations

Merchants outside travel and adjacent verticals should validate how well the platform fits their use case. Its industry focus can be a strength, but companies in other sectors may want to compare whether a more general-purpose orchestration platform offers a better fit.

Teams should also test how well the reporting, reconciliation, routing, and provider integrations match their internal finance and payment operations.

8. Paydock

Paydock is a low-code, API-first payment orchestration platform that connects payments, fraud, and identity services through a unified layer.

It is positioned for businesses that want to reduce payment complexity without taking on heavy development work.

Key capabilities

Paydock offers payment orchestration, gateway and acquiring connections, fraud and identity service integration, white-label payment capabilities, routing functionality, and centralized payment management.

Its low-code approach is designed to make payment connectivity and service management more accessible for both business and technical teams.

Strengths

Paydock can be useful for merchants, platforms, and financial institutions that want a unified way to manage payment services without building everything from scratch.

Its combination of payments, fraud, and identity orchestration may appeal to businesses that want to simplify vendor management and reduce technical overhead.

Paydock may also be attractive for teams that want a more accessible orchestration layer rather than a heavily engineering-driven payment infrastructure project.

Considerations

As with other low-code platforms, merchants should evaluate how much flexibility they have when handling complex custom payment logic.

Enterprise teams should also test reporting, reconciliation, provider-specific capabilities, governance controls, and how easily the platform can support more advanced payment operations over time.

9. BlueSnap

BlueSnap offers a global payment orchestration platform that combines payment processing, routing, fraud prevention, global coverage, and embedded payment capabilities.

Unlike pure orchestration layers, BlueSnap is also closely tied to global payment processing and acquiring services.

Key capabilities

BlueSnap provides global payment processing, intelligent payment routing, fraud tools, local acquiring capabilities, payment method support, tokenization, encryption, 3DS, reporting, and embedded payments functionality. Its platform is designed to help businesses sell globally through a more unified payment setup.

Strengths

BlueSnap can be a strong fit for merchants that want global payment acceptance and orchestration in a more bundled model. This can be attractive for businesses that prefer fewer vendor relationships and want payment processing, routing, fraud, and global coverage under one roof.

It may also work well for software platforms or businesses interested in embedded payment capabilities.

For companies that do not want to manage too many separate PSP and acquiring relationships, BlueSnap can simplify the commercial and operational side of payments.

Considerations

BlueSnap may be less suitable for merchants that want a fully independent, provider-agnostic orchestration layer where they control many separate acquiring and PSP relationships.

Enterprise merchants should carefully assess whether they want orchestration as an independent control layer or as part of a broader processing package.

10. Payrails

Payrails is a modular payment and financial infrastructure platform built for enterprise payment operations. It focuses on helping global merchants manage payment orchestration, tokenization, chargebacks, reconciliation, analytics, and provider connectivity through one operating layer.

Unlike platforms that mainly position themselves around checkout or gateway connectivity, Payrails is more focused on the broader payment operations layer. This makes it relevant for companies that already have meaningful payment complexity and want to centralize control across PSPs, acquirers, fraud tools, and financial workflows.

Key capabilities

Payrails offers payment orchestration, dynamic routing, tokenization, chargeback management, automated reconciliation, analytics, and access to a growing ecosystem of integrations.

Its routing capabilities allow merchants to configure how payments move between PSPs, fraud providers, and other third-party services based on business rules and operational needs.

Strengths

Payrails can be a strong fit for enterprise merchants that want a modern payment operations layer rather than only a payment gateway abstraction.

Its value is especially clear for companies that need to connect multiple providers, improve payment performance, centralize payment data, and reduce operational fragmentation across payment, finance, and risk teams.

Payrails is also interesting for merchants that want to use payment data more strategically, not only for reporting but also for optimization, routing, reconciliation, and operational decision-making.

Considerations

Payrails appears to be positioned more toward larger merchants and enterprise payment teams. Smaller companies or businesses with simple payment setups may find the platform broader than they need.

As with any orchestration provider, merchants should validate the exact provider coverage, supported payment flows, reporting depth, reconciliation capabilities, and migration effort before choosing it.

Quick Comparison: Which Platform Fits Which Need?

| Platform | Best fit |

|---|---|

| Akurateco | Enterprise merchants that want broad payment infrastructure, smart routing, cascading, reporting, fraud tools, white-label capabilities, operational support, and deployment flexibility in one platform. |

| IXOPAY | Merchants that need orchestration, tokenization, reconciliation, and payment intelligence across a complex provider setup. |

| Primer | Teams that want configurable payment workflows and faster experimentation with payment logic. |

| Spreedly | Merchants that prioritize tokenization, vaulting, and gateway independence. |

| Gr4vy | Teams that want a cloud-native, dashboard-driven payment orchestration layer. |

| BR-DGE | Merchants looking for modular orchestration and flexible access to a broad payment ecosystem. |

| CellPoint Digital | Travel, airline, hospitality, and complex multi-party payment environments. |

| Paydock | Businesses looking for low-code orchestration across payments, fraud, and identity services. |

| BlueSnap | Merchants that want global payment processing and orchestration in a bundled model. |

| Payrails | Enterprise merchants that want to centralize payment operations, routing, tokenization, reconciliation, chargebacks, and payment analytics in one modern infrastructure layer. |

How Enterprise Merchants Should Make the Final Choice

There is no single best payment orchestration platform for every business. The right choice depends on the merchant’s current payment setup, provider relationships, regions, transaction volume, compliance requirements, internal technical resources, and long-term payment strategy.

Before choosing a provider, enterprise merchants should ask practical questions:

- Can the platform support our current PSPs, acquirers, payment methods, and markets?

- Does it support the exact transaction flows we need, including refunds, recurring payments, 3DS, chargebacks, settlement reporting, and reconciliation?

- Can our team safely change routing rules without creating production risk?

- Does the platform give us enough visibility into approval rates, declines, provider performance, and operational issues?

- How does tokenization work, and how portable are payment credentials?

- Can the platform scale with our traffic, regions, and business entities?

- Does the deployment model match our compliance and procurement requirements?

- Will we receive enough operational and technical support after integration?

These questions matter because payment orchestration is not only about connecting more providers. It is about building a payment infrastructure that can improve performance, reduce operational complexity, and support growth.

Why Akurateco Deserves Close Attention

For enterprise merchants that want more control over payments without building the full stack internally, Akurateco is one of the more complete options to evaluate.

Its value is not only in orchestration. It brings together routing, cascading, provider connectivity, fraud tools, reporting, tokenization, merchant management, white-label infrastructure, and operational support. This makes it especially relevant for businesses that see payments as a strategic function rather than a back-office utility.

Akurateco can be a strong choice for merchants that want to:

- Reduce dependency on a single PSP

- Improve payment approval performance

- Expand into new regions and payment methods

- Centralize transaction management

- Gain better visibility across providers

- Keep more control over payment infrastructure

- Avoid building and maintaining complex payment technology in-house

For enterprise teams, that combination can be the difference between simply processing payments and actively optimizing payment performance.

This is where Akurateco’s positioning becomes especially practical. Some platforms solve one part of the payment challenge: routing, tokenization, checkout configuration, or provider abstraction. Akurateco is designed as a broader infrastructure layer, which can be valuable for merchants that want fewer disconnected systems and more operational control.

Conclusion

In 2026, payment orchestration is becoming a core part of enterprise payment strategy. It helps merchants manage provider complexity, improve transaction performance, reduce operational friction, and build more resilient payment infrastructure.

The best platform is not necessarily the one with the longest list of connectors. It is the one that fits your business model, payment flows, regions, compliance needs, team structure, and growth plans.

For some merchants, the priority will be tokenization and provider independence. For others, it will be low-code configuration, travel-specific payment flows, global acquiring, modular access to payment services, or a wider payment operations layer.

For enterprise merchants looking for a broader infrastructure layer with orchestration, routing, reporting, fraud tools, white-label capabilities, operational support, and deployment flexibility, Akurateco is a platform worth serious consideration.

The right payment orchestration platform should not only help you connect more providers. It should help your business turn payments into a more controlled, measurable, and scalable part of growth.

FAQ

What is a payment orchestration platform?

A payment orchestration platform is a centralized layer that lets merchants manage multiple payment providers, methods, routing logic, retries, fraud tools, tokenization, reporting, and reconciliation from one place instead of maintaining separate provider integrations.

What should you look for when choosing a payment orchestration platform?

Key areas to compare are routing and decisioning, connector coverage and integration depth, scalability and resilience, reporting and visibility, tokenization strategy, governance and access controls, and deployment/compliance flexibility.

Which payment orchestration platform is best in 2026?

There is no single universal winner. The best platform depends on your provider mix, regions, transaction volume, compliance needs, and long-term strategy — the goal is the right balance of flexibility, control, operational depth, and scalability for your business.

Why does connector depth matter more than connector count?

A connector can be technically available but still limited in practice — it may not support every transaction type, currency, refund, recurring flow, chargeback, 3DS flow, or reporting format you need. Validating your exact payment flows matters more than the length of the logo list.

Does Akurateco support on-premises deployment?

Yes. Akurateco supports both SaaS and more controlled deployment options, which can be important for enterprise merchants with stricter compliance, hosting, or data-residency requirements.