- What are payment methods by country?

- Why do payment preferences vary so much by country?

- Payment methods by country in 2026

- Payment methods by region at a glance

- What does this mean for your payment infrastructure?

- How payment orchestration helps localize payment acceptance

- Build, integrate directly, or use orchestration?

- Common mistakes when expanding payment method coverage

- Key takeaways

- Conclusion

A checkout that works in one country can fail quietly in another. Payment methods by country matter because consumers do not choose payment options only by convenience. They follow local habits shaped by banking infrastructure, card penetration, regulation, trust, mobile adoption, and the payment networks already embedded in daily life.

For businesses selling across markets, the challenge is not only knowing that Dutch shoppers prefer iDEAL or that Brazilian shoppers expect Pix. The harder problem is accepting these methods reliably while managing provider connections, routing logic, fraud rules, reconciliation, settlement reporting, refunds, and operational support.

Digital wallets now account for 56% of global e-commerce transaction value , according to Worldpay’s 2026 Global Payments Report coverage, while cards, account-to-account payments, BNPL, and domestic schemes still dominate specific markets. The global trend is digital, but the execution is local.

What are payment methods by country?

Payment methods by country are the locally preferred ways consumers and businesses pay in a specific market, such as cards in Japan, iDEAL in the Netherlands, Pix in Brazil, UPI in India, BLIK in Poland, or M-PESA in Kenya.

For a merchant, this means payment strategy should not start with “which methods are globally popular?” It should start with “which payment methods are trusted, available, and expected in each country where we sell?”

Local payment methods can include:

- Domestic card schemes, such as Cartes Bancaires in France.

- Bank transfer schemes, such as iDEAL in the Netherlands.

- Real-time account-to-account payment systems, such as Pix and UPI.

- Mobile wallets, such as Alipay, WeChat Pay, PayPal, Apple Pay, GCash, or M-PESA.

- Buy now, pay later methods, such as Klarna, Afterpay, or local invoice-based options.

- Cash-based or voucher-style methods in markets where cash remains relevant.

The operational point is simple: a local payment method is not just another checkout button. It has its own transaction flow, status logic, settlement timing, refund process, reporting structure, and reconciliation requirements.

Why do payment preferences vary so much by country?

Payment preferences vary because every country developed its payment infrastructure differently. Markets with strong domestic bank rails often prefer bank-based payments. Markets with high card trust continue to rely on cards. Markets that leapfrogged card infrastructure through mobile adoption often run on wallets or mobile money.

This is why global payment methods do not replace local payment methods. They coexist with them.

Several factors shape local payment behavior:

| Factor | How it affects payment preference | Example |

| Banking infrastructure | Strong bank rails can make account-to-account payments mainstream | iDEAL in the Netherlands, UPI in India |

| Card penetration | High credit card trust keeps cards dominant | Japan, United States, Canada |

| Regulation | Public payment infrastructure can accelerate adoption | Pix in Brazil |

| Consumer trust | Shoppers prefer familiar and locally protected methods | Invoice and BNPL habits in Germany |

| Mobile adoption | Smartphone-first markets often adopt wallets faster | China, Kenya, Southeast Asia |

| Merchant cost pressure | Lower-cost rails can compete with card networks | Pix, iDEAL, UPI |

| Cross-border behavior | International shoppers may still need cards or global wallets | Travel, SaaS, marketplaces |

For payment teams, the problem is not only conversion. The wrong payment mix can increase costs, create settlement fragmentation, complicate refunds, and reduce approval rates.

Payment methods by country in 2026

The dominant payment methods by country in 2026 show how fragmented global payments remain. Cards still matter, but in many markets they are no longer enough.

United States

The United States remains a card-heavy market, but digital wallets have become central to online checkout. PayPal, Apple Pay, Google Pay, and card-funded wallets are now part of baseline acceptance for many merchants.

For US merchants, Visa and Mastercard remain essential. PayPal can add conversion in e-commerce, especially for returning shoppers. BNPL is relevant in categories with higher average order values, such as electronics, fashion, travel, and home goods.

Operationally, the US is not difficult because of one dominant local rail. It is difficult because payment performance depends on authorization quality, card network logic, wallet support, tokenization, fraud checks, retries, and routing across acquirers.

Canada

Canada is similar to the US in its reliance on cards, but Interac plays an important domestic role. Visa and Mastercard are widely used online and in-store, while Interac supports debit and bank-based payment flows.

For merchants entering Canada, card acceptance is usually the baseline. Interac becomes more important when targeting domestic consumers, debit-led use cases, and local payment familiarity.

The main operational priority is keeping card acceptance strong while supporting domestic debit expectations where relevant.

Germany

Germany is one of the clearest examples of why payment methods by country matter. Cash still accounted for 51% of point-of-sale transactions in 2023 , while debit cards were used in 27% of payments and mobile payments rose to 6%, according to the Deutsche Bundesbank.

Online, German consumers are more comfortable with PayPal, invoice payments, SEPA transfers, direct debit, and BNPL than many other European markets. This reflects a long-standing preference for paying after goods arrive and for bank-based payment mechanisms.

For merchants, card-only checkout is risky in Germany. A practical German payment setup should consider:

- PayPal for broad consumer familiarity.

- Klarna or invoice-style BNPL where category and risk profile allow it.

- SEPA direct debit or bank transfer for recurring, B2B, and account-based flows.

- Girocard relevance in domestic card acceptance and in-store commerce.

- Strong fraud, refund, and dispute handling because invoice and deferred payment methods change risk dynamics.

Netherlands

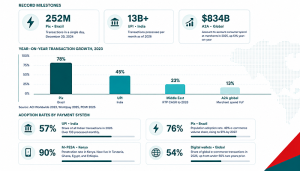

The Netherlands is a bank-transfer-first e-commerce market. iDEAL remains the standard for online payments, with the Dutch Payments Association describing it as the most widely used online payment method and estimating its online market share at around 70% .

Credit cards are relevant for travel, international purchases, and some cross-border commerce, but they are not the core domestic method. For Dutch consumers, iDEAL is familiar, trusted, and directly connected to their bank.

A merchant launching in the Netherlands without iDEAL is likely to lose conversion. The operational requirement is to support iDEAL flows correctly, including redirects, payment confirmation, status updates, reconciliation, and refunds.

France

France is a card-led market, but the local card scheme matters. Cartes Bancaires is France’s domestic card network and is widely used across French payments. J.P. Morgan described Cartes Bancaires as France’s leading payment network, processing around 15 billion CB transactions per year by card or mobile phone.

For merchants, accepting only international card rails can mean missing local optimization opportunities. Cartes Bancaires can affect cost, authorization performance, and customer familiarity.

A strong France setup should include:

- Cartes Bancaires where available.

- Visa and Mastercard for domestic and international cards.

- PayPal for online wallet preference.

- Local fraud and SCA handling aligned with European regulatory requirements.

Poland

Poland is one of Europe’s strongest mobile payment markets. BLIK has become a core domestic method across e-commerce, POS, P2P, and ATM flows. BLIK reported more than 2.4 billion transactions in 2024 , including 1.2 billion online store payments , with 18.5 million active users.

For merchants, BLIK is not just an alternative method. It is a mainstream local payment rail, especially for Polish e-commerce.

Payment teams should treat Poland as its own market rather than assuming a generic European card-and-wallet setup will perform well.

Nordic countries

The Nordic region is highly digital, but it should not be treated as one payment market. Sweden, Norway, Denmark, and Finland each have their own local habits.

A simplified view:

| Country | Important local methods | Practical implication |

| Sweden | Swish, Klarna, cards | BNPL and mobile payment familiarity matter |

| Norway | Vipps, cards | Local wallet coverage can improve domestic conversion |

| Denmark | MobilePay, Dankort, cards | Domestic card and wallet support both matter |

| Finland | Online banking, cards, mobile wallets | Bank-based payments remain relevant |

The mistake is building a “Nordics” checkout and assuming it works equally well across all four countries. Payment method display, routing, and reporting should be localized by country.

China

China is a wallet-first market. Alipay and WeChat Pay dominate consumer payments, and QR-based wallet flows are deeply embedded in both online and offline commerce. A 2026 Worldpay-based industry report states that digital wallets accounted for 89% of online transaction value and 87% of POS value in China in 2025 .

For international merchants, direct card acceptance is not enough. The practical route is usually to work through a provider or orchestration layer that can support Alipay, WeChat Pay, UnionPay, cross-border settlement, and local compliance requirements.

China is also a good example of why payment method acceptance is not only about checkout. It affects local partnerships, data requirements, currency handling, refunds, and regulatory exposure.

India

India’s primary payment rail is UPI. UPI has become a default payment method for everyday commerce, P2P payments, merchant payments, and increasingly recurring flows. UPI processed 21.63 billion transactions in December 2025 , according to reporting based on NPCI data.

For merchants selling into India, UPI support is essential for domestic reach. Cards still matter for higher-value purchases, international customers, and specific categories, but UPI is the method that reflects local payment behavior.

A serious India payment setup should consider:

- UPI intent and collect flows.

- PhonePe and Google Pay user behavior.

- Card support for premium or cross-border use cases.

- Refund and reconciliation logic for high-volume instant payments.

- UPI Autopay where recurring billing is relevant.

Japan

Japan remains unusually card-friendly compared with many other major markets. Credit cards are still highly relevant for e-commerce, while wallets, QR payments, and IC transit cards such as Suica matter in physical commerce.

For online merchants, card acceptance is the priority. For omnichannel merchants, QR and stored-value payment methods become more important.

A Japan strategy should focus on card authorization quality, JCB support, domestic acquirer performance, and localized checkout experience.

Southeast Asia

Southeast Asia is mobile-first but fragmented. A regional payment strategy needs country-by-country configuration.

| Market | Important payment methods | Practical note |

| Philippines | GCash, cards, bank transfer | Wallet support is critical for mass-market reach |

| Indonesia | DANA, OVO, GoPay, bank transfer, cards | Wallet and bank-transfer flows matter more than cards alone |

| Malaysia | Touch ‘n Go, GrabPay, FPX, cards | Bank transfer and wallets both matter |

| Singapore | Cards, PayNow, GrabPay, wallets | Cards remain strong, but real-time payments are growing |

| Thailand | PromptPay, wallets, cards | QR and account-to-account flows are important |

| Vietnam | MoMo, ZaloPay, bank transfer, cards | Wallets and bank rails both matter |

The operational challenge in Southeast Asia is provider fragmentation. Each market may require different wallet providers, bank integrations, settlement processes, and refund rules.

Brazil

Brazil’s payment story is Pix. PCMI estimates that Pix accounted for 40% of Brazil’s e-commerce volume in 2024 , ahead of domestic credit cards at 34%. PCMI also states that at least 75% of Brazil’s population actively uses Pix.

Pix also reached a major scale milestone when it recorded 252.1 million transactions in a single day on December 20, 2024, according to Brazilian coverage citing the central bank.

For merchants, Pix matters for conversion and cost. It is often cheaper than card payments, settles quickly, and is familiar to Brazilian consumers. However, it also requires correct handling of instant payment status, QR codes, expiry windows, refunds, and reconciliation.

Cards still matter in Brazil, especially because installment payments are culturally important. A practical setup should support both Pix and local card installment logic.

Mexico

Mexico remains more card- and cash-driven than Brazil. Debit and credit cards are important for online purchases, while cash-based and convenience-store payment methods still matter for parts of the population.

Digital wallets are growing, with Mercado Pago playing an important role in regional commerce. For merchants, Mexico requires a balanced setup: cards, wallet support, and cash-adjacent methods depending on category and customer segment.

Fraud prevention and authorization performance are especially important because card transactions remain central to online commerce.

Saudi Arabia

Saudi Arabia is moving quickly toward digital payments. The Saudi Central Bank reported that electronic payments accounted for 85% of total retail payments in 2025 , up from 79% in 2024, with electronic transactions reaching 14.6 billion.

For merchants, the key local considerations are mada, cards, Apple Pay, STC Pay, and the broader shift away from cash. Card and wallet acceptance both matter, especially for e-commerce and mobile-first experiences.

Payment teams should also account for local acquiring, Arabic checkout localization, compliance, and settlement reporting.

Kenya

Kenya is a mobile money market, and M-PESA remains the central method for domestic digital payments. Communications Authority data reported by TechCabal showed M-PESA with 90.8% mobile money market share in Q1 2025 , while mobile money subscriptions reached 45.4 million and penetration hit 86.6%.

For merchants entering Kenya, M-PESA is the priority. Cards are useful for travel, international commerce, and higher-income segments, but domestic reach depends heavily on mobile money.

A Kenyan payment setup should support M-PESA payments, payouts where relevant, clear status handling, and mobile-first checkout UX.

Payment methods by region at a glance

The table below simplifies the most important payment methods by country and region. It should be used as a planning view, not as a final integration checklist.

| Country / region | Dominant payment behavior | Key local methods | Card relevance | Infrastructure implication |

| United States | Cards and wallets | PayPal, Apple Pay, Google Pay | High | Optimize authorization, wallets, tokens, BNPL |

| Canada | Cards and domestic debit | Interac, Visa, Mastercard | High | Add domestic debit where relevant |

| Germany | Debit, PayPal, invoice, bank transfer | Girocard, PayPal, Klarna, SEPA | Medium | Support non-card payment preferences |

| Netherlands | Bank-based online payments | iDEAL | Low to medium | iDEAL is required for local conversion |

| France | Domestic card scheme | Cartes Bancaires | High | Local card routing can affect cost and performance |

| Poland | Mobile payment | BLIK | Medium | BLIK should be treated as core e-commerce method |

| Nordics | Local wallets, cards, BNPL, bank payments | Swish, Vipps, MobilePay, Klarna | Medium to high | Avoid one-size-fits-all Nordic setup |

| China | Mobile wallets | Alipay, WeChat Pay, UnionPay | Low direct card use | Local partner and wallet support are essential |

| India | Real-time payments | UPI, PhonePe, Google Pay | Medium | UPI is required for domestic scale |

| Japan | Credit cards | JCB, Visa, Mastercard | High | Card performance and JCB support matter |

| Southeast Asia | Wallets and bank transfers | GCash, DANA, OVO, GrabPay, FPX, PromptPay | Medium | Market-by-market wallet coverage |

| Brazil | Instant payments and installments | Pix, local cards, boleto | Medium | Pix plus installment card logic |

| Mexico | Cards, cash, wallets | Mercado Pago, OXXO-style cash flows, cards | High | Balance cards, wallets, and cash-based options |

| Saudi Arabia | Cards and digital payments | mada, STC Pay, Apple Pay | High | Local acquiring and wallet support |

| Kenya | Mobile money | M-PESA | Low to medium | M-PESA is essential for domestic reach |

What does this mean for your payment infrastructure?

Accepting local payment methods is not just a checkout project. It affects every layer of payment infrastructure, including routing, reconciliation, settlement, fraud, reporting, customer support, and provider management.

The more countries you enter, the more payment method complexity compounds.

A simple example:

- iDEAL may use redirect-based bank authorization.

- Pix may use QR code or copy-paste payment flows.

- UPI may use app-based intent or collect requests.

- BLIK may use a code-based mobile confirmation.

- BNPL may introduce delayed settlement and credit-risk rules.

- Cards may require 3DS, tokenization, retries, and acquirer routing.

Each method creates different operational questions:

| Operational area | Why it becomes harder with more local methods |

| Checkout | Customers must see the right methods by country, device, currency, and basket size |

| Routing | Transactions need to be routed by provider availability, cost, performance, and risk |

| Fraud management | Risk signals differ between cards, wallets, bank transfers, and BNPL |

| Reconciliation | Settlement files and statuses vary by provider and method |

| Refunds | Refund timing and refund rails differ by scheme |

| Reporting | Finance teams need consistent reporting across fragmented methods |

| Support | Customer-facing payment statuses must be clear and localized |

| Compliance | Local regulations, SCA, data handling, and KYC rules may apply |

This is where many merchants underestimate the cost of expansion. The visible cost is the integration. The hidden cost is maintaining every method after launch.

How payment orchestration helps localize payment acceptance

Payment orchestration helps merchants, PSPs, and fintech companies manage multiple payment methods, PSPs, acquirers, and routing rules through one infrastructure layer. Instead of integrating every method separately, companies can connect through an orchestration platform and control availability, routing, cascading, reporting, and provider logic centrally.

For a merchant, this means the checkout can show iDEAL to Dutch shoppers, Pix to Brazilian shoppers, UPI to Indian shoppers, Klarna or PayPal to German shoppers, and cards to Japanese shoppers without rebuilding the payment stack for every market.

For PSPs and fintech companies, orchestration is even more strategic. It supports:

- Faster launch of new local payment methods.

- Multi-PSP and multi-acquirer connectivity.

- Smart routing based on cost, approval rate, geography, currency, or provider status.

- Cascading when a transaction fails with one provider.

- Unified merchant management.

- Centralized transaction monitoring.

- Reconciliation and reporting across providers.

- More flexible payment method configuration by merchant or market.

A payment orchestration platform such as Akurateco can help companies manage this infrastructure layer without building every integration, routing tool, dashboard, and reporting module from scratch. The value is not only “more payment methods”. The value is operational control over a fragmented payment environment.

Build, integrate directly, or use orchestration?

There are three main ways to expand payment method coverage: build in-house, integrate directly with providers, or use a payment orchestration platform. The right choice depends on scale, technical resources, compliance exposure, and how many markets you plan to support.

| Approach | Pros | Cons | Best for |

| Build in-house | Maximum control, custom architecture, direct provider relationships | High cost, long timelines, ongoing maintenance, compliance burden | Large enterprises with mature payment engineering teams |

| Direct provider integrations | Faster than building everything, good for limited market coverage | Integration sprawl, fragmented reporting, harder routing, provider lock-in | Merchants operating in a small number of markets |

| Payment orchestration platform | Single infrastructure layer, faster method rollout, centralized routing and reporting | Requires platform evaluation and migration planning | PSPs, fintechs, marketplaces, and merchants scaling across markets |

For many scaling companies, direct integrations work at first. The problem appears later, when the payment stack includes multiple PSPs, acquirers, local methods, currencies, fraud tools, and reporting formats.

At that stage, orchestration becomes a way to reduce complexity while preserving flexibility.

Common mistakes when expanding payment method coverage

Most payment method mistakes are not caused by choosing the wrong provider. They happen because companies treat payment method expansion as a checklist instead of an operating model.

Offering every method to every customer

Showing all payment methods to all customers creates noise and can reduce conversion. A Brazilian customer should see Pix prominently. A Dutch customer should see iDEAL. A Japanese customer should see cards first.

Payment method display should be dynamic by country, currency, device, customer segment, and basket value.

Treating cards as the universal fallback

Cards are still essential, but they are not a universal solution. In markets such as the Netherlands, Brazil, India, China, Poland, and Kenya, local methods can be the default consumer expectation.

Card-only acceptance can limit conversion and increase processing costs.

Ignoring reconciliation before launch

Payment teams often test authorization flows but underinvest in reconciliation. This creates problems for finance teams once multiple providers, settlement files, refund statuses, and currencies enter the stack.

A new payment method should not go live until reporting and settlement workflows are clear.

Not planning routing logic

Adding a payment method is useful. Knowing when to route a transaction through one provider versus another is where performance improves.

Routing logic should account for:

- Country.

- Currency.

- Card type.

- Payment method.

- Provider uptime.

- Approval rate.

- Cost.

- Risk profile.

- Merchant configuration.

Underestimating maintenance

Payment methods change. APIs change. Regulations change. Providers change reporting formats. New versions of local schemes appear. A payment stack needs ongoing ownership, not one-time integration work.

This is one reason PSPs and fintech companies evaluate white-label payment software and orchestration platforms: the goal is to reduce internal maintenance while keeping control over the payment experience.

Key takeaways

- Payment methods by country should guide payment infrastructure decisions, not only checkout design.

- Card acceptance remains essential, but it is not enough in markets such as Brazil, India, the Netherlands, China, Poland, and Kenya.

- Local payment methods can improve conversion and reduce costs, but they add operational complexity across routing, settlement, reconciliation, and reporting.

- Payment orchestration is most valuable when a company manages multiple PSPs, acquirers, markets, currencies, and payment methods.

- PSPs and fintech companies should treat local payment method coverage as part of product infrastructure, not as a one-off integration task.

- Enterprise merchants should prioritize payment methods by market size, customer preference, cost impact, and operational readiness.

- The best payment stack is flexible enough to add, remove, route, and monitor payment methods without constant engineering work.

Conclusion

Payment method strategy in 2026 is a market-by-market infrastructure decision. The question is not simply whether your checkout supports cards, wallets, or bank transfers. The question is whether your payment stack can present the right method to the right customer, route the transaction effectively, reconcile it cleanly, and scale the setup across new markets.

For PSPs, fintech companies, marketplaces, and enterprise merchants, the practical framework is clear: prioritize local relevance, measure cost and approval impact, plan reconciliation before launch, and avoid building a fragmented stack that becomes difficult to maintain.

For companies managing complex payment infrastructure, Akurateco can act as a technology partner that helps simplify orchestration, routing, provider connectivity, reporting, and scalability without requiring a full infrastructure rebuild.

FAQ

What are payment methods by country?

Payment methods by country are the payment options consumers prefer in specific markets. Examples include iDEAL in the Netherlands, Pix in Brazil, UPI in India, BLIK in Poland, M-PESA in Kenya, and Cartes Bancaires in France. Merchants use this insight to localize checkout and improve payment performance.

Why are local payment methods important for merchants?

Local payment methods matter because customers are more likely to complete checkout when they see familiar and trusted options. They can also reduce processing costs, improve authorization performance, and support market expansion. However, they require proper handling of settlement, refunds, reporting, and reconciliation.

Is card acceptance enough for international merchants?

Card acceptance is necessary but not always enough. Cards remain strong in markets such as the US, Canada, Japan, and France, but many high-growth markets rely heavily on local methods. Pix, UPI, iDEAL, BLIK, Alipay, WeChat Pay, and M-PESA can be essential for domestic conversion.

How does payment orchestration help with local payment methods?

Payment orchestration connects multiple PSPs, acquirers, and local payment methods through one infrastructure layer. It helps companies configure checkout availability, route transactions, cascade failed payments, centralize reporting, and manage provider performance without building separate integrations for every method.

What is the difference between local payment methods and alternative payment methods?

Local payment methods are payment options strongly preferred in a specific country or region. Alternative payment methods is a broader category that includes non-card options such as wallets, bank transfers, BNPL, and mobile money. In many markets, these methods are no longer alternative; they are the default.

Should PSPs build payment method integrations in-house or use white-label payment software?

Building in-house gives control but increases development, maintenance, compliance, and integration costs. White-label payment software can help PSPs launch faster with existing gateway infrastructure, payment method connectivity, merchant management, routing, reporting, and risk tools while preserving brand control.