- What does payment performance mean?

- Why does payment performance drop?

- Which KPIs should payment teams track?

- How can payment teams increase payment performance?

- Payment performance framework for enterprise merchants

- Build vs buy: should you optimize payments in-house or use orchestration?

- Common mistakes that reduce payment performance

- Where Akurateco fits into payment performance optimization

- Conclusion

Payment performance is not only about whether a transaction is approved or declined. It is the combined result of checkout design, payment methods, authorization data quality, routing logic, fraud controls, provider uptime, settlement visibility, and operational decision-making.

For merchant-side payment teams, better payment performance means more successful transactions, fewer false declines, lower processing costs, less revenue leakage at checkout, and clearer control over PSPs, acquirers, fraud tools, reports, and payment methods.

The practical challenge is that payments rarely fail for one reason. A transaction can be declined because of issuer risk rules, poor routing, missing authentication data, unavailable payment methods, PSP downtime, fraud settings, expired credentials, or avoidable customer friction. Improving performance requires a structured operating model, not a one-time checkout fix.

What does payment performance mean?

Payment performance measures how effectively your payment setup converts payment attempts into successful, profitable, and compliant transactions. It should be measured across approval rate, cost, fraud, checkout conversion, retry recovery, and reporting accuracy.

In a simple setup, teams often define payment performance as the approval rate or authorization rate . That is useful, but incomplete. A high approval rate can still be expensive if transactions are routed through costly providers. A low fraud rate can still hurt revenue if the fraud engine blocks too many legitimate customers. A polished checkout can still underperform if the PSP or acquirer route is weak for a specific market.

A stronger definition includes:

- Payment approval rate: the percentage of authorization attempts approved.

- Payment success rate: the percentage of payment attempts that result in completed payment.

- Payment conversion rate: the percentage of checkout users who successfully pay.

- False decline rate: legitimate payments incorrectly rejected.

- Retry recovery rate: failed transactions recovered through retry or cascading.

- Cost per successful transaction: total processing cost divided by successful payments.

- Chargeback and fraud ratio: risk exposure after authorization.

- Settlement and reconciliation accuracy: whether finance teams can match transactions, fees, refunds, and payouts.

For multi-brand businesses, marketplaces, and platform merchants, payment performance also includes account-level visibility. One region may need better local acquiring. Another may need stricter fraud rules. A third may need payment method localization. A payment team cannot optimize every flow with a single global rule.

Why does payment performance drop?

Payment performance drops when payment infrastructure becomes more complex than the team’s ability to monitor and control it. The most common causes are poor payment method fit, weak routing, missing transaction data, over-aggressive fraud rules, provider issues, and fragmented reporting.

Most payment teams start with a provider that works well enough. Then the business expands. New markets, currencies, customer segments, card types, wallets, APMs, subscriptions, refunds, chargebacks, and settlement timelines appear. What looked like a simple payment stack becomes a performance system with many hidden failure points.

Common causes include:

| Cause | How it hurts performance | Example |

| Poor local payment coverage | Customers abandon checkout or use less efficient methods | A Dutch customer does not see iDEAL |

| Single-provider dependency | No fallback when one PSP or acquirer underperforms | PSP outage causes avoidable failed payments |

| Weak routing logic | Transactions go to the wrong provider | High-value cards routed to a low-performing acquirer |

| Missing or inconsistent data | Issuers lack confidence in the transaction | Incorrect billing, device, or authentication data |

| Overly strict fraud rules | Legitimate customers are blocked | Returning customers challenged unnecessarily |

| No cascading logic | Soft declines become final failures | Temporary issuer issue is not retried elsewhere |

| Fragmented reports | Teams cannot see what to improve | Declines are tracked in one system, fees in another |

This is why payment optimization is increasingly treated as a dedicated discipline. Competitor content from Checkout.com and Primer both frames optimization around acceptance, fraud, customer experience, authorization, and cost control rather than only checkout design.

Which KPIs should payment teams track?

Track payment KPIs at route, provider, market, card type, issuer, payment method, and merchant level. Aggregate numbers hide the exact failure points that payment teams need to fix.

A global approval rate can look stable while one market is leaking revenue. A PSP can show acceptable total performance while a specific merchant category is struggling with issuer declines. A fraud tool can reduce chargebacks while silently increasing false declines.

The core KPI model should include:

| KPI | Why it matters | Best segmentation |

| Authorization rate | Shows issuer approval performance | Provider, acquirer, issuer BIN, country, card type |

| Payment success rate | Shows full payment completion | Checkout, provider, payment method, market |

| Decline rate by reason | Identifies fixable failure patterns | Hard decline, soft decline, fraud, technical, insufficient funds |

| Retry recovery rate | Measures cascading and retry effectiveness | Decline reason, provider, card type, subscription cohort |

| Checkout abandonment rate | Shows UX and payment method friction | Device, country, payment method, page step |

| Cost per approved transaction | Connects performance to margin | Provider, scheme, acquirer, payment method |

| Fraud and chargeback rate | Protects revenue after approval | Merchant, product type, region, fraud rule |

| Settlement mismatch rate | Measures finance accuracy | Provider, merchant, currency, settlement batch |

Payment analytics should not only answer “what happened?” It should help your team decide what to change. Akurateco’s payment analytics positioning is built around giving PSPs and merchants transaction status, financial data, merchant-level reports, decline visibility, and exportable data for further analysis.

How can payment teams increase payment performance?

Increase payment performance by improving the full payment lifecycle: checkout, payment method relevance, authorization quality, routing, cascading, fraud controls, cost visibility, and reporting. Each layer should feed data back into the next optimization cycle.

Payment performance improves when teams stop treating payments as a static integration. The goal is to create a feedback loop: measure performance, identify weak points, adjust rules, test results, and repeat.

1. Improve checkout and payment method relevance

Checkout is the first performance layer. If customers cannot find their preferred payment method, do not trust the page, face unnecessary redirects, or struggle on mobile, the transaction may never reach authorization.

For merchants, this means adapting payment methods by market, device, currency, and customer type. For PSPs, it means giving merchants configurable checkout options without custom engineering for every account.

Useful actions include:

- Display local methods where they matter.

- Prioritize wallets, bank payments, cards, or APMs based on user location.

- Reduce unnecessary form fields.

- Use clear error messages instead of generic failure messages.

- Support mobile-first checkout and fast page loading.

- Localize language and currency where relevant.

Payment method optimization is not only a UX issue. It also affects cost and approval probability. A local method may convert better and cost less than a cross-border card transaction.

2. Improve authorization data quality

Authorization performance depends partly on what the issuer receives. Incomplete, inconsistent, or poorly formatted transaction data can increase issuer suspicion or lead to avoidable declines.

Payment teams should review:

- Billing and shipping data quality.

- Device and IP information where appropriate.

- Merchant category and descriptor consistency.

- 3DS data quality.

- Stored credential indicators for recurring payments.

- Tokenization and account updater logic for cards on file.

- Correct handling of MIT/CIT transaction types.

This is especially important for subscriptions, marketplaces, travel, gaming, digital services, and cross-border merchants where issuer risk models may be more sensitive.

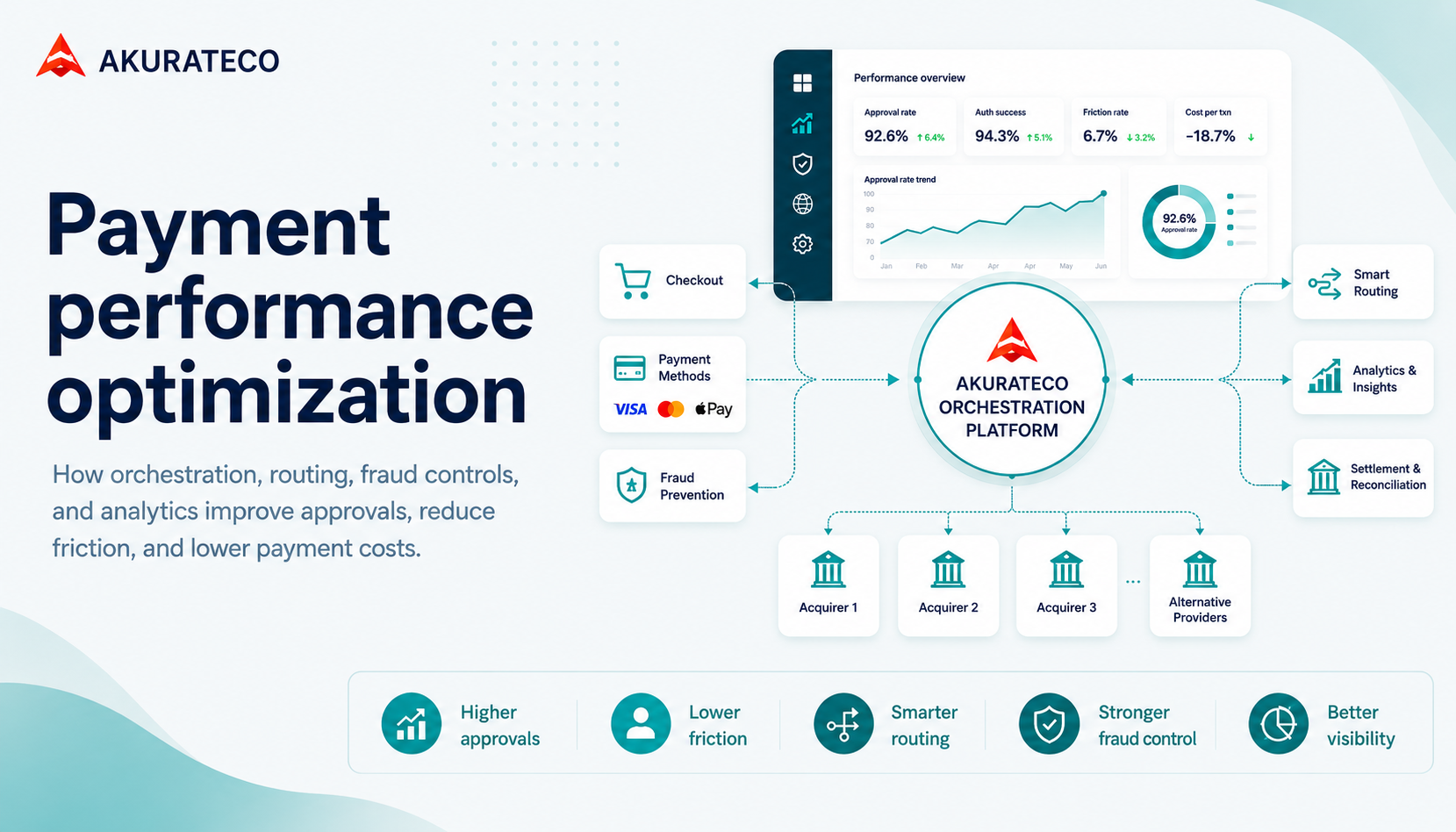

3. Use smart routing across PSPs and acquirers

Smart routing sends each transaction through the provider or acquirer most likely to produce the best outcome. “Best” does not always mean cheapest. It can mean highest approval probability, lowest cost, fastest settlement, local coverage, lower fraud exposure, or a rule-based balance between these factors.

A strong routing model can use parameters such as:

- Country.

- Currency.

- Card brand.

- BIN / issuer.

- Transaction amount.

- Merchant ID.

- Payment method.

- Customer segment.

- Provider uptime.

- Historical approval rate.

- Processing cost.

- Risk score.

This is where a payment orchestration platform becomes operationally useful. Akurateco’s orchestration page describes a single platform for connecting providers, optimizing transactions, using smart routing and cascading, and centralizing payment management. Its routing page also highlights route logic based on parameters such as card brand, BIN, currency, transaction amount, region, and card type.

4. Apply cascading and retry logic carefully

Cascading means retrying a failed transaction through an alternative payment channel. It is most useful for soft declines, technical failures, PSP downtime, temporary issuer issues, or route-specific failures.

It should not be applied blindly. Retrying every decline can increase cost, duplicate authorization attempts, trigger issuer suspicion, and create a poor customer experience.

A practical retry framework:

| Decline type | Retry approach | Risk |

| Technical timeout | Retry quickly, possibly through another provider | Duplicate attempts if not controlled |

| PSP/acquirer unavailable | Cascade to backup provider | Higher cost if fallback route is expensive |

| Suspected fraud | Do not auto-retry without risk review | Increased fraud exposure |

| Insufficient funds | Retry later, especially for subscriptions | Customer frustration if too frequent |

| Authentication required | Trigger appropriate authentication flow | Added friction |

| Hard decline | Do not retry automatically | Scheme or issuer rule violations |

For PSPs, cascading is especially valuable when supporting many merchants with different processing needs. The PSP can offer fallback logic as an infrastructure capability rather than forcing each merchant to build its own retry system.

5. Balance fraud prevention and approval rates

Fraud controls protect revenue, but over-aggressive fraud rules can damage payment performance. The goal is not to approve everything. The goal is to approve more legitimate transactions while blocking real risk.

Payment teams should review fraud rules by:

- Merchant category.

- Transaction value.

- Customer history.

- Geography.

- Device behavior.

- Velocity patterns.

- Chargeback history.

- 3DS outcome.

- Risk scoring provider.

A good fraud setup should support whitelists, blacklists, risk scoring, custom filters, manual review flows, and rule-level reporting. Akurateco’s fraud prevention page describes in-house and external scoring models, whitelists, blacklists, customizable filters, real-time fraud reporting, and chargeback-related tools.

6. Reduce processing costs without hurting conversion

Cost optimization should not be isolated from approval performance. The cheapest route can become expensive if it creates more failed payments. The right question is: which route produces the best net outcome after approval rate, fees, fraud, refunds, and operational effort?

Cost levers include:

- Local acquiring where relevant.

- Routing by card type or region.

- Using lower-cost payment methods in markets where customers accept them.

- Reducing unnecessary retries.

- Monitoring scheme, acquirer, and PSP fees.

- Managing cross-border and currency conversion costs.

- Segmenting high-cost card types.

- Improving reconciliation to find fee leakage.

Worldpay’s optimization page similarly frames payment optimization around revenue, efficiency, credential management, and dynamic routing to reduce cost of acceptance.

7. Use reporting and reconciliation as performance feedback

Reporting is not back-office administration only. It is the diagnostic layer for payment performance. Without clean reporting, payment teams cannot see whether a provider is underperforming, whether a decline pattern is issuer-specific, whether routing changes improved margin, or whether settlements match expected amounts.

A practical reporting setup should show:

- Approval and decline rates by route.

- Decline reason trends.

- Provider and acquirer performance.

- Retry and cascading recovery.

- Payment method conversion.

- Fraud rule impact.

- Fees by provider and method.

- Settlement status.

- Refund and chargeback patterns.

- Merchant-level performance for PSPs.

For PSPs, merchant-facing reporting can also become a product differentiator. Merchants want visibility into what is happening, not only monthly settlement files.

Payment performance framework for enterprise merchants

Merchants usually optimize their own payment conversion, cost, and market coverage. PSPs need to optimize performance across many merchants, MIDs, providers, risk profiles, and reporting needs.

| Area | Merchant focus | PSP focus |

| Checkout | Improve customer conversion | Offer configurable checkout tools to merchants |

| Payment methods | Add relevant local and global methods | Maintain broad connector and method coverage |

| Routing | Route own traffic by cost and approval rate | Manage routing logic across merchant portfolios |

| Cascading | Recover failed transactions | Provide fallback logic as infrastructure |

| Fraud | Balance risk and conversion | Support merchant-level and MID-level risk rules |

| Reporting | Track own payment KPIs | Give merchants transparent dashboards and exports |

| Reconciliation | Match transactions and settlements | Support multi-merchant settlement and fee reporting |

| Scalability | Expand markets efficiently | Onboard merchants, providers, and acquirers faster |

For merchants, the main question is: How do we make more customer payments succeed profitably?

For PSPs, the question is broader: How do we give every merchant better performance without rebuilding custom infrastructure for each one?

That difference matters. PSPs need merchant management, routing controls, provider integrations, fraud tooling, settlement logic, reporting, and support workflows. A merchant can sometimes solve a narrow performance issue with one provider. A PSP needs a system.

Build vs buy: should you optimize payments in-house or use orchestration?

In-house development gives control, but it increases maintenance, integration, compliance, and reporting complexity. Payment orchestration is usually more practical when the business needs multiple PSPs, routing, cascading, fraud controls, and unified analytics.

| Approach | Pros | Cons | Best for |

| Single PSP setup | Simple to launch, less engineering | Limited routing, limited fallback, provider dependency | Early-stage merchants with simple needs |

| In-house payment optimization | Full control, custom logic | High engineering cost, ongoing maintenance, compliance burden | Large enterprises with mature payment teams |

| Multiple direct PSP integrations | More provider choice | Fragmented reporting, duplicated integrations, harder reconciliation | Scaling merchants with strong engineering resources |

| Payment orchestration platform | Unified control, routing, cascading, reporting, faster provider expansion | Requires platform selection and operating discipline | PSPs, fintechs, marketplaces, enterprise merchants |

| White-label payment software | Faster PSP launch, brand control, built-in infrastructure | Less custom than full internal build | PSPs, PayFacs, banks, fintech infrastructure teams |

A payment orchestration platform such as Akurateco can help when a company needs to connect multiple providers, set routing and cascading rules, manage fraud tools, centralize reports, and scale payment operations without building every layer from scratch. Akurateco’s platform messaging specifically covers multi-provider orchestration, smart routing, cascading, payment analytics, automatic reconciliation, and provider connectivity.

Common mistakes that reduce payment performance

Payment performance usually suffers when teams optimize one metric in isolation. Higher approval rates, lower costs, and lower fraud must be managed together.

Avoid these mistakes:

- Optimizing only for approval rate. More approvals are not useful if fraud and chargebacks rise faster than revenue.

- Choosing the cheapest route by default. A low-cost provider with weak approval performance can reduce net revenue.

- Retrying every failed payment. Retry logic should respect decline reason, scheme rules, cost, and customer experience.

- Using one fraud rule set for every merchant or market. Risk patterns differ by geography, vertical, ticket size, and customer type.

- Ignoring issuer and BIN-level patterns. Aggregate approval rates hide valuable optimization opportunities.

- Treating reporting as a finance-only function. Payment operations, product, fraud, and finance teams all need the same source of truth.

- Adding PSPs without orchestration. More providers do not automatically improve performance if routing, monitoring, and reconciliation stay manual.

Where Akurateco fits into payment performance optimization

Akurateco fits best when merchants, PSPs, fintech companies, or banks need an orchestration-first infrastructure layer for routing, cascading, provider connectivity, fraud controls, analytics, and merchant management.

Akurateco should not be positioned as a generic “better checkout” tool. The stronger positioning is infrastructure-led: Akurateco helps companies manage payment complexity when one PSP, one acquirer, or one static integration is no longer enough.

Relevant use cases include:

- A merchant wants to improve payment performance across multiple countries.

- A PSP wants to offer merchants better approval rates and transparent reporting.

- A fintech company wants to add payment functionality without building every component internally.

- A bank or acquirer wants merchant management, payment routing, risk controls, and analytics.

- A marketplace needs multiple payment methods, merchant onboarding, recurring payments, and settlement visibility.

- A company already has several PSPs but lacks orchestration, reporting, and fallback logic.

Akurateco’s white-label payment gateway page also positions the platform for PSPs, merchants, marketplaces, banks, and acquirers, with connectors, reporting, merchant management, routing, risk management, recurring payments, and integration options.

Conclusion

Increasing payment performance requires a structured framework. Start by defining the right KPIs, then identify where revenue is leaking: checkout, payment method coverage, authorization quality, provider performance, fraud rules, routing, retries, costs, or reconciliation.

For merchants, the goal is to make more customer payments succeed with less friction and better margins. For PSPs and fintech companies, the goal is to provide that performance across many merchants, markets, providers, and risk profiles without creating operational chaos.

For companies managing complex payment infrastructure, Akurateco can act as a technology partner that helps simplify orchestration, routing, provider connectivity, fraud controls, reporting, and scalability without requiring a full infrastructure rebuild.

FAQ

What is payment performance?

Payment performance measures how effectively a payment setup turns payment attempts into successful, profitable, and compliant transactions. It includes approval rate, payment success rate, checkout conversion, fraud rate, retry recovery, cost per transaction, and settlement accuracy. A strong payment performance model looks beyond approvals and connects payments to revenue, margin, and operations.

How can enterprise merchants increase payment performance?

Merchants can increase payment performance by offering relevant payment methods, improving checkout UX, submitting better authorization data, using local acquiring where useful, applying smart routing, recovering soft declines through controlled retries, and adjusting fraud rules to reduce false declines. The best results come from continuous monitoring rather than one-time optimization.

Why do legitimate payments get declined?

Legitimate payments can be declined because of issuer risk rules, missing transaction data, expired credentials, insufficient funds, PSP downtime, authentication issues, fraud filters, or poor routing. Some declines are hard declines and should not be retried. Others are soft declines that may be recovered through authentication, retry scheduling, or cascading.

What is the difference between payment routing and payment cascading?

Payment routing selects the best provider, acquirer, or payment path before sending a transaction. Payment cascading happens after a failed attempt, retrying the transaction through an alternative route when appropriate. Routing is proactive optimization, while cascading is recovery logic for eligible failed transactions.

How does payment orchestration improve payment performance?

Payment orchestration improves payment performance by adding a unified control layer across PSPs, acquirers, payment methods, fraud tools, routing rules, cascading, analytics, and reporting. It helps payment teams compare providers, automate routing decisions, recover eligible failed transactions, and manage payment operations from one system.

Should PSPs build payment optimization tools in-house?

PSPs can build optimization tools in-house if they have strong engineering, compliance, payment operations, and support capacity. However, building routing, cascading, merchant management, analytics, reporting, and provider integrations requires ongoing maintenance. A white-label or orchestration platform can reduce time to market while preserving control over payment operations.