- What does payment orchestration mean in 2026?

- What is open-source payment orchestration?

- What is white-label payment orchestration?

- Open source vs white-label payment orchestration: core differences

- When does open source make sense?

- When is white-label orchestration the better choice?

- Hidden costs to evaluate before choosing

- Decision framework for payment providers and fintech infrastructure teams

- Open source vs white-label: which is better by business stage?

- Common mistakes when evaluating payment orchestration infrastructure

- Conclusion

Payment orchestration is no longer just a technical way to connect several payment providers. In 2026, it has become a strategic infrastructure decision for payment providers, PayFacs, and fintech companies that need to manage provider connectivity, merchant configuration, routing, fraud controls, payment methods, settlement, reconciliation, and reporting through one operational layer.

The main question is not whether payment orchestration is useful. For many payment businesses, that question has already been answered. The real question is how much of the infrastructure your company should build, own, maintain, certify, and support internally.

This is where the comparison between open-source and white-label payment orchestration becomes important. Open source can offer deeper technical control and flexibility. White-label payment orchestration can reduce development workload, shorten time to market, and give payment companies ready-made infrastructure that can still be branded and configured around their business model.

This guide compares both approaches from a practical payment infrastructure perspective, with a focus on payment providers, PayFacs, acquirers, and fintech teams evaluating how to launch, upgrade, or scale their own payment platform in 2026.

What does payment orchestration mean in 2026?

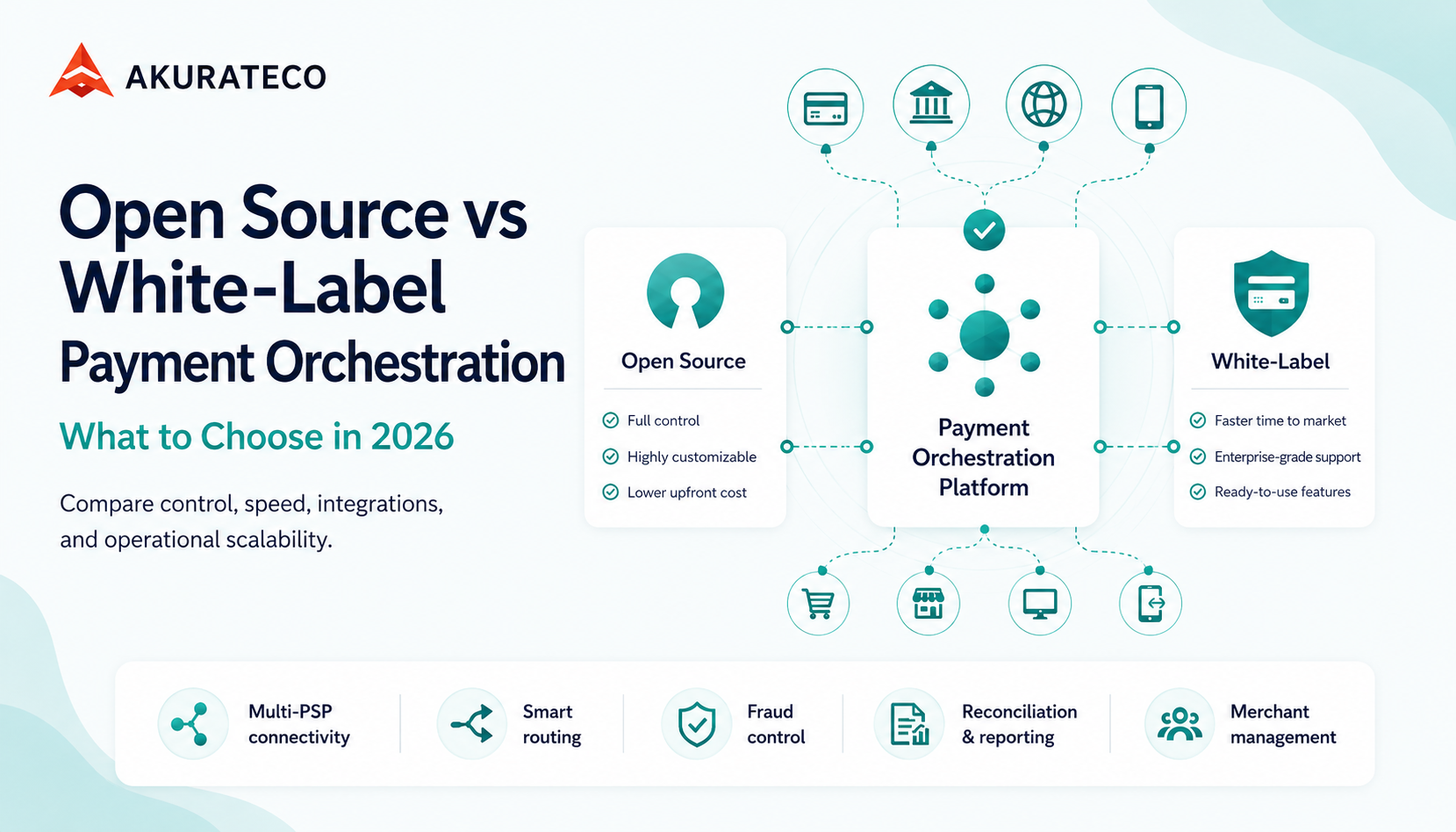

Payment orchestration is a centralized infrastructure layer that connects payment providers, acquirers, gateways, payment methods, fraud tools, routing rules, and reporting workflows in one system.

In practice, a payment orchestration platform helps payment teams manage the full transaction lifecycle across multiple providers instead of building and maintaining separate integrations for every PSP, acquirer, local payment method, or fraud service. This matters because payment operations rarely stay simple for long. A company may start with one gateway, then add more providers, more regions, more currencies, more payment methods, more reporting needs, and more risk controls.

A modern orchestration layer is expected to support multi-PSP connectivity, smart routing, cascading, payment method management, tokenization, fraud and risk controls, transaction monitoring, merchant management, settlement visibility, and reconciliation reporting. For payment companies, this layer often becomes the operational center of the business.

That is why the choice between open source and white label is not only a technical preference. It affects how quickly the company can launch, how much engineering capacity it needs, how easily it can add new providers, and how much operational responsibility it wants to keep in-house.

What is open-source payment orchestration?

Open-source payment orchestration refers to payment infrastructure where the source code is publicly available or self-hostable, allowing companies to inspect, modify, deploy, and extend the system themselves.

The main attraction is control. A company can work directly with the codebase, adapt workflows, build custom modules, and reduce dependency on a closed vendor roadmap. For engineering-led teams, this can be appealing because it gives them more freedom to shape the infrastructure around their own architecture, deployment preferences, and product logic.

Open source can be especially useful when the company has a strong internal engineering team, clear DevOps ownership, and enough payment domain knowledge to maintain the system over time. It may also be a good fit for experimentation, technical proof of concept, or highly specific payment flows that require unusual customization.

However, open source should not be confused with free infrastructure. The absence of a traditional software license does not remove the cost of implementation, provider maintenance, uptime monitoring, security reviews, compliance preparation, documentation, or support. In many cases, the largest cost of open source appears after the first launch, when the company has to maintain connectors, monitor provider changes, fix issues, upgrade dependencies, and support payment operations at scale.

For companies that want to own payment infrastructure as a core engineering asset, this trade-off may be acceptable. For companies that need faster commercial deployment, the operational burden can become a serious limitation.

What is white-label payment orchestration?

White-label payment orchestration is ready-made payment infrastructure that can be branded, configured, and operated under your company’s name while the technology provider maintains the core platform.

For PSPs, fintech companies, and enterprise merchants, the main value is speed and operational leverage. Instead of building a payment gateway, orchestration engine, routing layer, merchant dashboard, reporting tools, reconciliation logic, fraud modules, and provider integrations from scratch, the company starts with an existing infrastructure layer and adapts it to its business model.

This approach is especially relevant when payment infrastructure is commercially important but not something the company wants to build entirely in-house. A PSP may want to launch a branded payment platform. A fintech company may want to embed payment capabilities into its product. An enterprise merchant may want to reduce dependency on one PSP and manage several providers through one control layer.

White-label payment orchestration does not mean giving up control. The control is different. Instead of controlling every line of code, the company controls branding, configuration, merchant setup, routing logic, provider usage, reporting workflows, and operational processes. The provider is responsible for maintaining the core platform, supporting updates, and helping the company scale the infrastructure.

For many payment businesses, this becomes a practical middle ground between building everything internally and relying on a basic third-party gateway that cannot support complex payment operations.

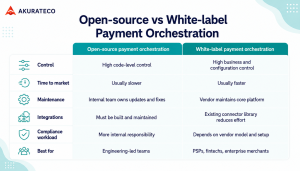

Open source vs white-label payment orchestration: core differences

Both models can support payment orchestration, but they solve different problems. Open source is mainly about technical ownership. White label is mainly about operational acceleration.

| Criteria | Open-source payment orchestration | White-label payment orchestration |

| Control | High code-level control | High business and configuration control |

| Time to market | Usually slower unless the team is already experienced | Usually faster because the core infrastructure already exists |

| Upfront cost | Lower software cost, higher implementation effort | Higher vendor cost, lower internal build effort |

| Maintenance | Internal team owns updates, fixes, monitoring, and scaling | Vendor maintains the core platform |

| Customization | Deep technical customization | Business-level configuration plus vendor-supported customization |

| Compliance workload | More internal responsibility | Depends on deployment model and vendor support |

| Integrations | Must be implemented, tested, and maintained | Existing connector library reduces integration workload |

| Support | Community or internal support | Vendor support and service commitments |

| Best for | Engineering-led teams with strong infrastructure ownership | PSPs, fintechs, and merchants that need faster scalable infrastructure |

The simplest way to frame the decision is this: open source gives you more technical ownership, while white label gives you more operational acceleration.

Neither option is universally better. The right choice depends on your business model, launch timeline, internal engineering capacity, regulatory exposure, provider complexity, and long-term payment strategy.

When does open source make sense?

Open source makes sense when payment infrastructure is a strategic engineering asset and your company is prepared to own it deeply.

This usually applies to companies with experienced payment engineers, strong DevOps resources, and a clear understanding of how payment infrastructure will be maintained after launch. If your team can manage provider integrations, monitor uptime, handle incidents, review security requirements, and build the surrounding operational tools, open source can give you meaningful flexibility.

For example, a fintech company building a specialized payment flow for a narrow region may use open-source infrastructure to prototype provider connections, routing logic, and internal workflows. This can work well when transaction volumes are still manageable and the team has enough control over the technical environment.

Open source can also be attractive when the company has unusual requirements that a vendor cannot support. If the orchestration logic is tightly connected to proprietary infrastructure or internal product logic, having code-level access may be valuable.

The challenge appears as the business scales. Every new provider, payment method, country, currency, fraud rule, reporting need, and compliance requirement adds maintenance work. What starts as a flexible technical choice can become a long-term operational responsibility.

When is white-label orchestration the better choice?

White-label orchestration is usually the better choice when the business priority is launching, scaling, or modernizing payment infrastructure without turning every infrastructure layer into an internal engineering project.

This is especially relevant for PSPs, PayFacs, fintech companies, banks, acquirers, and enterprise merchants that need commercial payment capabilities quickly but still want branding, flexibility, and operational control.

A PSP launching a new payment product, for example, may need merchant onboarding, payment pages, transaction monitoring, routing, cascading, reporting, settlement visibility, and provider management from the beginning. Building all of this internally can take significant time and resources. With a white-label payment orchestration platform, the company can focus more on commercial strategy, merchant acquisition, pricing, support, and market expansion.

For enterprise merchants, white-label orchestration can help unify fragmented provider relationships. Instead of managing each PSP separately, payment teams can use one orchestration layer to configure routing, monitor performance, analyze declines, and improve operational visibility.

A payment orchestration platform such as Akurateco fits this model by giving payment companies access to white-label payment software, provider connectivity, smart routing, cascading, merchant management, reporting, and reconciliation tools in one infrastructure layer. The value is not only in the technology itself, but in reducing the amount of infrastructure the company needs to build and maintain alone.

Hidden costs to evaluate before choosing

The cheapest-looking option is not always the lowest-cost option. Payment infrastructure creates costs across engineering, compliance, operations, support, provider maintenance, downtime, finance workflows, and internal process management.

| Cost area | Open-source risk | White-label risk | What to evaluate |

| Engineering | More internal build and maintenance | Less code ownership | Internal engineering capacity |

| Integrations | Connector maintenance stays internal | Connector coverage depends on vendor | Required PSPs, acquirers, payment methods, and fraud tools |

| Compliance | More internal documentation and control ownership | Vendor scope must be reviewed carefully | PCI DSS, data handling, hosting, and responsibilities |

| Uptime | Internal team owns monitoring and incidents | Vendor SLA must be reviewed | SLA, alerting, incident process |

| Reporting | May require custom dashboards | Built-in tools may need adaptation | Finance, settlement, and reconciliation workflows |

| Merchant operations | Often must be built around the core system | Usually included or configurable | Onboarding, roles, permissions, merchant data |

| Roadmap | Fully internal responsibility | Vendor roadmap dependency | Feature priorities and customization process |

For open-source infrastructure, the most underestimated cost is usually maintenance. Provider APIs change, payment methods evolve, fraud patterns shift, and operational teams need better dashboards as the business grows. All of this requires internal capacity.

For white-label infrastructure, the main evaluation point is vendor fit. The company should review deployment options, provider coverage, customization flexibility, support model, security responsibilities, and how well the platform fits its payment roadmap.

Compliance is also important. A white-label provider can reduce technical and operational burden, but it does not automatically remove the company’s compliance responsibilities. The exact scope depends on the deployment model, data flows, payment roles, hosting setup, and contractual responsibilities.

Decision framework for payment providers and fintech infrastructure teams

The right model depends on what your company is trying to become.

If your company wants to own payment infrastructure as a deep technical asset, open source may be a logical route. This applies when you have strong internal engineering, longer implementation timelines, DevOps capacity, security expertise, and a clear reason to control the codebase.

If your company wants to launch or scale payment infrastructure faster, white label is usually more practical. This applies when you need branded infrastructure, merchant-facing tools, provider connectivity, smart routing, reporting, reconciliation, and operational dashboards without building each layer internally.

For PSPs and PayFacs, white-label orchestration is often the stronger fit because the business usually needs more than transaction processing. It needs merchant management, pricing logic, onboarding workflows, reporting, transaction monitoring, provider configuration, and support tools. These are operational requirements, not just technical integrations.

For fintech companies, the answer depends on whether payments are the core engineering product or an embedded capability. If payments are the product’s deepest infrastructure layer, open source or hybrid models may be worth considering. If payments support the broader product experience, white-label orchestration can reduce distraction and speed up delivery.

For enterprise merchants, white-label orchestration is often more useful because the goal is usually not to become a payment infrastructure company. The goal is to improve approval rates, reduce provider dependency, improve reporting, and manage multiple PSPs more efficiently.

Open source vs white-label: which is better by business stage?

| Business stage | Better fit | Reason |

| Prototype or technical proof of concept | Open source | Lower initial software barrier and high code flexibility |

| Early PSP launch | White label | Faster go-live and fewer infrastructure layers to build |

| Scaling fintech | Depends | Open source if payments are core engineering IP; white label if speed matters more |

| Enterprise merchant with many PSPs | White label | Faster consolidation of routing, reporting, and reconciliation |

| Regulated payment company | White label or hybrid | Vendor support can reduce operational burden, but compliance scope must be reviewed |

| Large payment company with mature engineering | Hybrid or open source | Internal teams may justify deeper infrastructure ownership |

The practical question is not only which model gives more flexibility. The better question is which model gives your company the right level of control without slowing down commercial growth.

A company with a large technical team may be comfortable with the responsibility of open source. A company trying to enter the market quickly may benefit more from a white-label platform that already includes the core infrastructure needed to operate.

Common mistakes when evaluating payment orchestration infrastructure

Many companies compare open-source and white-label payment orchestration too narrowly. They focus on software cost, API flexibility, or the number of available integrations, while underestimating operational complexity.

One common mistake is treating open source as free infrastructure. The software may be open, but implementation, maintenance, security, monitoring, compliance preparation, and support still require people, time, and budget.

Another mistake is evaluating orchestration only through provider connections. Connections are important, but they are not enough. A payment team also needs to understand how routing rules are managed, how failed transactions are retried, how settlements are reconciled, how fraud controls interact with transaction flows, and how finance and operations teams access reliable reporting.

Companies also often underestimate merchant operations. For PSPs and PayFacs, the platform must support onboarding, merchant configuration, permissions, transaction visibility, support workflows, and reporting. Without these layers, the orchestration system may process transactions but still fail to support the business model.

A better evaluation process starts with the operating model. Before choosing software, the company should define who will manage providers, configure routing, review fraud, onboard merchants, investigate failed transactions, reconcile settlements, and support customers when issues appear.

Conclusion

The choice between open-source and white-label payment orchestration depends on what your company wants to own.

Open source is attractive when your engineering team wants deep technical control and is ready to maintain the infrastructure over time. It can work well for prototypes, specialized payment flows, and companies with strong internal payment engineering resources.

White-label orchestration is stronger when the business needs faster time to market, branded infrastructure, multi-provider connectivity, operational tools, merchant management, reporting, and scalability without building every layer internally.

For PSPs, fintech companies, and enterprise merchants managing complex payment infrastructure, Akurateco can act as a technology partner that helps simplify orchestration, routing, provider connectivity, reporting, reconciliation, and scalability without requiring a full infrastructure rebuild.

FAQ

What is payment orchestration?

Payment orchestration is a centralized infrastructure layer that connects payment providers, acquirers, gateways, payment methods, routing rules, fraud tools, and reporting workflows in one system. It helps payment teams manage transactions across multiple providers instead of maintaining separate integrations for every payment flow.

What is the difference between open-source and white-label payment orchestration?

Open-source payment orchestration gives companies code-level access and self-hosting flexibility, but requires internal teams to manage implementation, maintenance, security, scaling, and support. White-label payment orchestration provides ready-made infrastructure that can be branded and configured while the vendor maintains the core platform.

Is open-source payment orchestration cheaper?

Open source can reduce software licensing costs, but it is not automatically cheaper. Companies still need engineers, DevOps resources, security reviews, compliance preparation, integration testing, monitoring, and ongoing maintenance. The real cost depends on payment complexity, provider coverage, transaction volume, and internal capacity.

When should a PSP choose white-label payment orchestration?

A PSP should consider white-label payment orchestration when it needs to launch faster, support merchants, connect multiple providers, manage routing and cascading, offer reporting, and reduce development overhead. It is especially useful when the business needs branded infrastructure without building every system component internally.

How does payment orchestration help with routing and cascading?

Payment orchestration helps route each transaction to the most suitable provider based on rules such as geography, currency, cost, card type, or provider performance. If a transaction fails, cascading can retry it through another provider, improving the chance of approval without requiring manual intervention.

Is white-label payment software the same as a payment gateway?

No. A payment gateway mainly processes transaction data between the merchant, customer, acquirer, and issuer. White-label payment software can include gateway functionality, but usually covers a broader operating layer, including merchant management, routing, cascading, fraud tools, reporting, reconciliation, dashboards, and branded payment infrastructure.