The digital payments market is growing fast, and startup payment providers entering this increasingly competitive space are under pressure to differentiate. Owning the payment stack is becoming a strategic advantage because it gives payment businesses more control over merchant experience, provider connectivity, reporting, and pricing. That’s why the question of how to make your own payment processor has become a key priority for startup PSPs and other entrepreneurs looking to tap into the growing market.

Still, developing a payment processor is far from easy. Aside from development itself, regulations, security requirements, and mounting maintenance and support costs can quickly slow a project down. That’s why many payment teams choose white-label gateway solutions like Akurateco’s, which help them launch fully branded payment processing systems faster while staying compliant, without having to start from scratch.

This guide explains how to make your own payment processor, from architecture and stack to compliance and integrations. In addition, we make comparisons to white-label solutions, which can be a smarter, faster alternative to creating your own.

What a Payment Processor Is and How It Works

Before diving into how to make your own payment processor, it helps to clarify what a payment processor is and a few core terms in the payment flow, especially since industry players use them differently.

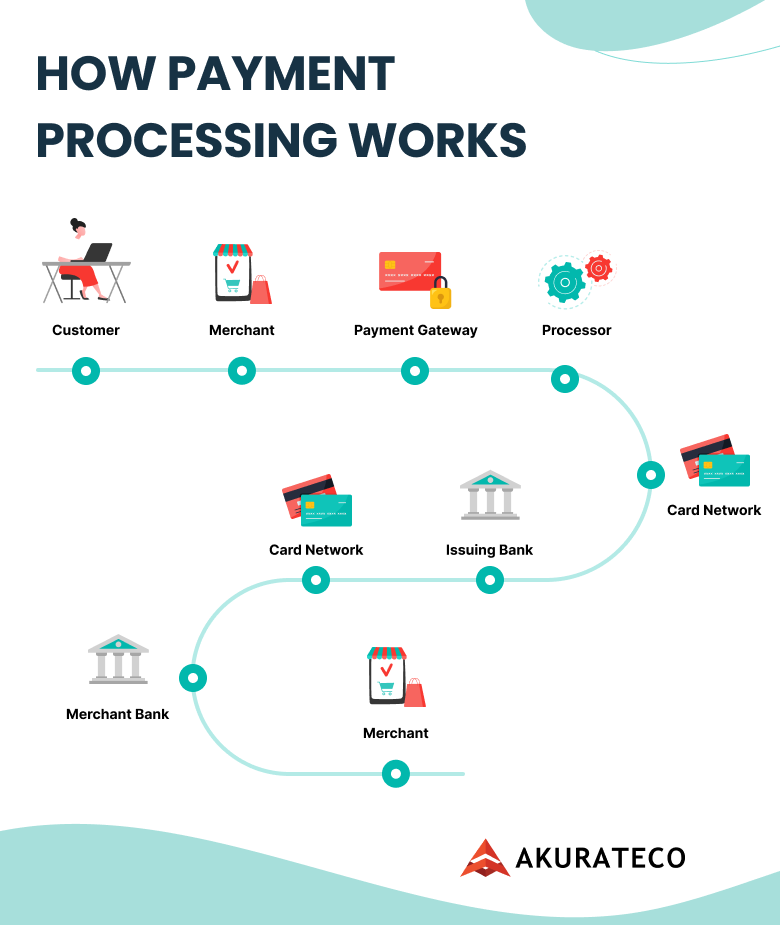

In a classic card-payments context, payment processor is the link between the merchant’s acquiring bank, the card networks (like Visa or Mastercard), and the customer’s issuing bank. This connection approves and completes the transaction. Its main mission is to manage authorization, settlement, and fund transfers, helping businesses accept payments quickly and securely.

However, in the PSP ecosystem, the term payment processor is often used more broadly. Here, it refers to the technical backbone a PSP operates on — typically a platform that includes a payment gateway, connections with acquiring banks and payment providers, and the ability to process transactions under the PSP’s financial license.

In the payment workflow, a credit card payment processor interacts with the other parties in the following way:

- The customer initiates payment on the merchant’s website.

- The payment gateway captures and encrypts the payment information and passes the authorization request to the payment processor.

- The processor sends the request via the card network to the issuing bank (the customer’s bank) to verify the funds.

- Once approved, the merchant receives the authorization confirmation and delivers the goods or services.

- The payment processor initiates the settlement process, sending data through the card network to move the approved funds from the issuing bank to the acquiring bank (the merchant’s bank).

In simple terms, a payment processor is the “engine” that enables the payment transfer behind the scenes. The payment gateway is what captures and transmits customer payment data. A PSP brings these components together in one unified solution for easier payment management.

It’s easy to mix up the terms in the payment process. To learn more about the differences between a payment processor, PSP, and a gateway, check out our guide about creating a payment gateway, where we break down each in detail.

Core Components of a Payment Processing System

Businesses exploring how to create a payment processor should first understand what components it consists of. Every layer, from the gateway to transaction monitoring, plays a role in keeping payments secure, fast, and compliant.

Here’s a quick look at the core elements that make a modern payment processor work.

Gateway and API integration

The payment gateway is where each transaction begins. It encrypts customer data and, through APIs, sends it securely to the processor. Platforms like Akurateco include these integrations from the start, so businesses can connect faster and stay compliant without extra development work.

Merchant onboarding and KYC/KYB

Merchant onboarding is the first checkpoint in payment processing. This is the stage where new merchants are verified and activated. In practice, automation makes this faster and safer. Within Akurateco’s white-label platform, the system runs KYC (Know Your Customer) and KYB (Know Your Business) checks automatically through built-in verification tools. That way, every merchant is confirmed as legitimate before going live.

Fraud prevention and PCI DSS compliance

Every reliable payment system starts with strong security. To operate legally and securely, compliance is the number one requirement. With PCI DSS Level 1 certification, merchants can process transactions securely and build customer trust.

In payments, spotting suspicious activity early is equally important. It’s key to avoid losses. Fraud prevention tools ensure ongoing monitoring. They check transactions in real time and spot anything that looks unusual. Akurateco provides these protections in its infrastructure, so businesses stay secure without additional security and compliance work on their end.

Routing and orchestration

In processing, payment routing is the technology that decides where each transaction goes for approval. In simple terms, it’s the logic that directs payments through the most reliable and cost-efficient channel. Orchestration builds on that idea. It provides multi-currency support, coordinates multiple providers, payment methods, and currencies in a single system. Together, routing and orchestration create the flexibility businesses need as their operations expand. Akurateco offers a payment orchestration solution with built-in smart routing logic that adapts to business goals in real time.

Transaction monitoring and reporting

As a core part of any payment processing system, monitoring and reporting bring visibility and control to every transaction. Real-time transaction monitoring helps detect irregularities early, reducing the risk of failed or delayed payments. In its turn, reporting tools translate transaction data into insights that let businesses adjust routing and maintain smooth operations. In Akurateco, the key tools for visibility are built in, offering businesses a centralized dashboard in a single solution.

How to Make Your Own Payment Processor: Step-by-Step

Building a payment processor involves several key steps, each comprising a number of additional layers.

1. Define your business model and licensing requirements

Before designing a payment processor architecture, decide what role it will play. It may be a full-service PSP, a white-label solution, or an internal processing hub. That choice alone determines your technical stack and compliance scope.

Study the markets you plan to work with. Rules differ everywhere. PCI DSS is mandatory worldwide. In most cases, a payment processing company must obtain a Money Transmitter License (MTL), EMI or PI License, MSB Registration, and AML/KYC. Getting the necessary frameworks right early will save you from the chaos of rebuilding later and keep your licensing, tech, and business processes moving in sync.

2. Choose the right technology stack and hosting

Once the vision is clear, decide how you plan to host your processor: on your own servers or with a third-party provider. The technologies and infrastructure you choose must match your scalability goals. Both have cost, speed, and control trade-offs.

If your system handles cardholder data, PCI DSS compliance is mandatory in both cases. Hosting in-house makes you fully responsible for annual audits. At the same time, these solutions ensure data ownership and security, though they’re slower to scale and cost more to maintain.

On the contrary, cloud environments deliver agility and speed but limit control over infrastructure. In addition, they don’t remove compliance duties entirely. So, it’s wise to think carefully beforehand.

After that, design the core payment processor architecture and select programming languages and frameworks that meet your performance requirements.

3. Decide between building from scratch or using a white-label platform

Building a payment processor from scratch based on your unique business goals gives you full control. Every part of the stack, data flow, and logic is yours to shape. However, it requires time, money, and a team that understands both technology and regulation.

Another option is a white label payment processor. With this smart approach, you can brand a ready-made software solution as your own and get started in no time. No investing time and significant budgets on development, maintenance, compliance, and integrations.

4. Integrate acquirers and payment methods via APIs

APIs are the backbone of your processor. They connect your platform with banks, acquirers, gateways, and payment methods, ensuring smooth transaction flow. When you design your API layer, think long term. It should be flexible enough to plug in new options later, but stable enough to keep existing connections running smoothly. For instance, some startups begin with a single acquirer and expand through modular APIs as volume grows.

5. Set up fraud and compliance tools

In payments, you must ensure the utmost level of security. When designing a payment processor, start with data protection. For this, use encryption, tokenization, and strong authentication to secure cardholder information. Add fraud detection with real-time monitoring, velocity checks, and behavioral analytics to flag anomalies early.

Passing one audit is just the beginning. In practice, staying compliant means keeping your tools active, running security scans, and updating documentation as systems evolve. You’ll need to review integrations, limit access rights, and train your team regularly. Add clear rules for data use and customer consent, and make sure dispute handling is fast and transparent.

6. Launch and onboard merchants

Once everything is set up and tested, you can deploy your payment processor and start bringing merchants on board. The smoother the process, the faster your processor can start generating volume. The goal here is to ensure speed and simplicity.

If onboarding feels slow or confusing, merchants drop out fast. That’s why automation matters. Let the system collect documents, run KYC/KYB checks, and open accounts without anyone stepping in manually.

Give merchants a dashboard that actually helps. This way, they can see verification status, upload files, or test sandbox payments. Real-time support is equally important, especially for high-risk or cross-border merchants, who often face more compliance friction.

Challenges and Costs to Consider

If you decide to create a payment processing platform, you can gain a few benefits, like full ownership and control. However, building a system that can compete with top rated credit card processing companies requires much more than ownership. It also means that you sign yourself up for a list of commitments and challenges along the way, some of which will be ongoing.

PCI certification costs

Compliance is hard to obtain, let alone maintain. This requires continuous scanning, auditing, and staff training to remain approved. For a payment processor, the expenditures on full audits, penetration tests, and annual renewals can push past $100K. If you miss an update, you risk delayed renewals or even losing your acquirer’s trust.

Integration maintenance

After deployment, you need to invest a lot of time and money in the maintenance of your payment processor. This is a critical stage that determines proper functioning and customer satisfaction.

You’ll need to monitor system performance, update APIs as acquirers or payment methods change, and fix bugs quickly to avoid downtime. Regular software updates, security patches, and integration checks are essential to stay compliant and compatible with banks and providers.

Development timelines

Developing a payment processor from scratch means building an entire ecosystem of interconnected integrations. In fact, even an MVP requires months of architecture design, partner integrations, and PCI DSS preparation. All of this is mandatory before you can process a single transaction.

On average, development takes if not years, then 12–18 months of continuous dedication, not counting certification or onboarding acquirers. Each new API integration or fraud system adds more time. In practice, without a dedicated, cross-functional team, projects often stall before launch.

Beyond operational drag, these drawn-out delivery timelines mean 12–18 months of lost revenue opportunities. For PSPs, it’s a full year or even of unrealized transaction volume, interchange margins, and processing fees, which could have been accumulating and strengthening their growth curve.

Support and upgrades

Uptime is non-negotiable, yet merchants value responsive, accessible support just as much. Beyond the technical side, reliable customer support should become part of your product. An expert team can directly impact merchant trust and retention by resolving issues as they arise and guiding customers along the way.

As your platform grows, continuous upgrades are equally important. You’ll need a dedicated team to add new payment methods, update the renewal logic for recurring billing flows, enhance reporting, and keep APIs optimized for performance.

Cost is the most immediate hurdle when building a payment processor. In fact, it extends far beyond development alone. Full ownership isn’t cheap. In practice, even a basic setup can cost around $500K plus maintenance and support. Enterprise-level payment systems with specific configurations typically start near $1M, depending on scope and compliance requirements.

That’s why many businesses turn to white-label payment software, where you can gain control over your infrastructure but for half the cost of custom development. The platform is already built, certified, and maintained by the provider. You control the branding, integrations, and features you want, without covering the full development cost.

Why White-Label Solutions Are the Smart Choice

Building a payment processor in-house can take years before you even process your first transaction. And when development is finally complete, the work is far from over. Ongoing security updates, PCI DSS certification, system maintenance, and round-the-clock customer support become part of your daily operations. That being said, it’s not one-time tasks. For most teams, that’s too much time and financial resources spent solving the wrong problem.

A white-label payment platform flips that model. You start with the rails already built. White-label platforms allow companies to launch in weeks instead of years with ready-made infrastructure, compliance included, and scalability opportunities. Since PCI DSS compliance, routing, and fraud tools come ready to use, you can focus on growing merchants rather than building infrastructure from zero.

In short, when going white-label, you get the freedom of ownership without the pain of development. It’s the fastest and most cost-efficient path to becoming a processor that scales.

Akurateco offers a white-label payment gateway with 700+ integrations, dedicated support, and PCI DSS certification. With a ready-made solution, you can save substantial time and costs and instead focus on scaling, not the technical side.

The Future of Payment Processors

Fintech is never about a simple build-and-use setup. Even after you complete payment processing system development, you’ll need to keep pace with an industry that changes faster than almost any other in tech. In practice, it means ensuring your processor adapts to new technologies and evolving customer expectations.

AI-based fraud prevention

Payment fraud is becoming more frequent and far more sophisticated. Traditional fraud engines simply can’t keep up with the speed and complexity of modern attacks. That’s why artificial intelligence will remain a powerful assistant in payments, able to quickly adapt to changing patterns. In particular, AI is super helpful for fraud prevention, where speed and precision are critical. It effectively reduces false declines, reduces manual reviews, and dynamically adjusts as fraudsters change tactics.

Modular payment systems and embedded finance

The payments industry evolves quickly, and so do the ways companies build their fintech payment infrastructure. One of the biggest shifts today that will remain in years to come is the move away from rebuilding entire systems every time something changes. Instead of relying on heavy, monolithic processors, more businesses are switching to modular setups. In these systems, you can add or swap payment components as needed, including new methods, risk tools, and reporting blocks, without touching the core.

This shift also fuels the rise of embedded finance, a trend that isn’t going anywhere. Industry players rely on it because it keeps payments inside the product experience. Instead of pushing users to external gateways, payments sit right inside a product, a marketplace, or an app. It feels natural, reduces friction, and usually boosts conversions and customer loyalty because the whole flow stays in one place.

Rise of multi-currency and A2A payments

If you don’t sell worldwide, you cut your business from more revenue streams. Today, merchants understand this rule and want payment options that match the customer’s region, currency, and banking habits.

Another trend to remain and gain more traction is A2A (account-to-account) payments. A2A payments skip the card networks entirely. This reduces costs and speeds up settlement, while making it harder for fraudsters to exploit stolen card data. For PSPs, that translates into better margins, higher conversion, and fewer operational headaches. That being said, if you’re building a processor today, leaving out A2A support puts you a step behind the market.

Akurateco’s PCI DSS-certified white-label solution is built to keep pace with where the industry is heading. It allows adding new custom integrations upon request, uses behavioral analytics and anomaly detection, and supports multi-currency capabilities. Altogether, it gives PSPs the flexibility to grow their merchant base and the confidence to operate efficiently as the payments landscape evolves.

Conclusion

If you decide to build a payment processor, you need to understand that it requires ongoing innovation, maintenance, and upgrades, not just initial development. In practice, every stage of the lifecycle takes time. Even if everything goes as planned, a full assembly will take months or years. Throughout that timeline, you’ll need a substantial budget, a clear roadmap, compliance certification, and a team with deep payments expertise.

When technical foundations are in place, it’s easier to focus on growing merchants, scaling your portfolio, and increasing revenue. That’s why for most businesses, choosing a white-label platform is simply faster, safer, and more strategic.

Akurateco delivers a ready-made payment gateway with 700+ pre-integrated connections, PCI DSS compliance, smart routing, cascading, advanced fraud protection, reporting, and ongoing support. It gives you a complete system out of the box, making it easier for you to start your own payment processor, reduce launch time, lower costs, and scale your business with confidence.

FAQ

How long does it take to make your own payment processor?

To create a payment gateway software, you’ll need to allocate at least 12–18 months for an MVP, while the total timeline for a fully assembled system may exceed a few years.

What licenses are required to start a payment processing company?

To start a payment processing company, you typically need a governmental license, depending on the country of operation. They are usually Money Transmitter License (MTL), EMI or PI License, MSB Registration, AML/KYC, and others. In addition, you’ll need industry compliance with PCI DSS, which is mandatory worldwide.

What’s the difference between a payment processor and a PSP?

A payment processor focuses on the technical process. It enables the authorization, routing, and settlement of payments between banks. A PSP goes further by offering the whole package: gateway, processor connections, fraud tools, and multiple payment methods in one place.

How can Akurateco help me start my own payment processing company?

Akurateco provides a ready-made infrastructure to help you start your own online payment processor in no time. You get a PCI DSS-certified white-label platform with 700+, smart routing, fraud tools, onboarding, reporting, and full technical support. So, you can focus on growing your merchant base, while the platform handles the tech and compliance.