- What are A2A payments?

- How do A2A payments differ from P2P payments?

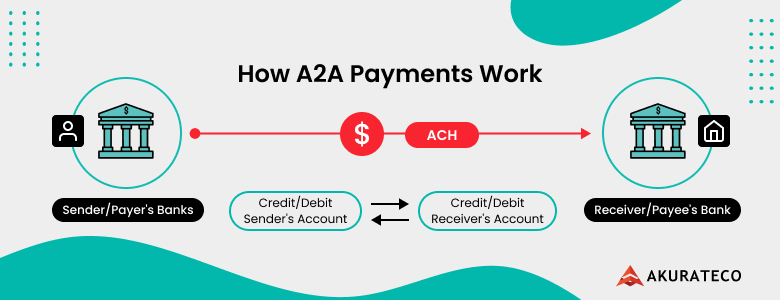

- How does Account-to-Account transfer work?

- What are instant A2A payments?

- Types of A2A payments explained

- Understanding payment rails for A2A payments

- Global examples of A2A payment rails

- Other examples of A2A payment rails

- The advantages of A2A payments

- Potential drawbacks of A2A payments

- The impact of open banking on A2A payments

- Challenges to A2A payment adoption

- What’s next? The future of A2A payments

- Discover A2A payments with Akurateco

The global finance landscape is growing dynamically. Can you imagine that just 10 years ago, such payment methods as digital wallets, Buy Now Pay Later (BNPL), and contactless payments didn’t exist at all? But with rapid technological development, the situation has changed.

One of the transformative trends in this field is the evolution of Account 2 Account (A2A) payments. Now, they are completely turning the tide in countries like India with UPI and Brazil with Pix. However, these transactions are still a secondary payment method in such major markets as China, Japan, South Korea, and the United States.

For online businesses, A2A payments can offer security, speed, checkout convenience, and lower transaction costs compared with some card-based flows. So, what is the A2A payment meaning, how do A2A payments differ from Pay by Bank and Peer-to-Peer (P2P) methods, and what is their potential for merchant payment strategy? Let’s get down to business.

What are A2A payments?

A2A payments mean direct e-transfers of funds that are made from a buyer’s bank account to a seller’s account. A2A transfers bypass standard payment systems and are instantly credited to the recipient’s account. They are already popular among individuals (P2P), businesses (B2B), users and businesses (P2B), and governments (P2G, G2P). According to FIS’s Global Payments Report 2023, 70 real-time payment systems are now contributing to the A2A transfers global growth.

A2A payments are also called Pay by Bank payments, which eliminate the need for cash or cards. By connecting bank accounts, you can send or request money directly through ACH, RTP, or FedNow rails. A2A and Pay by Bank payments operate in distinct ways. A2A payments involve a direct transfer between accounts without intermediaries. This means funds are moved directly from your account to the recipient’s, offering a more streamlined process.

In contrast, Pay by Bank functions as an online payment authorization method. When using Pay by Bank, you log in to your online banking platform to confirm a payment request. This involves a verification step through your bank, adding a layer of security but potentially extending the transaction time.

Real-time payments are another type of Pay by Bank transaction that happens instantly. Real-time payments offer immediate transfers for various purposes, including:

- Splitting bills, granting money, personal loans

- Automated bill and rent payments, invoice settlements, refunds, etc

- Tax refunds, tax payments, license fees, fines.

How do A2A payments differ from P2P payments?

Open banking-powered transactions take A2A transfers to the next level. A2A payments are based on financial technologies integrating different banks using a common Application Programming Interface (API). These technologies provide direct communication between banks, guaranteeing that transactions will be faster and safer. In this case, the funds are transferred directly, bypassing intermediaries. For payments to legal entities, details can be filled in automatically or by QR code, while for P2P transfers, a simple recipient Identification Number (ID) is sufficient. Thus, A2A payments can be used for any type of transaction, offering bright advantages and gradually replacing bank cards.

How does Account-to-Account transfer work?

For A2A payments, funds can be transferred between accounts at the same or different banks, or between a bank account and a brokerage account. For these transactions, the consumer’s financial institution must have instant payment credit.

In the case of a transfer between two bank accounts – even at different financial institutions – the A2A method is simple. The customers transfer funds from their savings account to their current account. Transfers between current accounts and digital wallets work similarly.

However, you need to remember that not every digital wallet offers this type of A2A transaction, as some of their services still rely on Automated Clearing House (ACH) transfers or card transactions.

For transfers between a standard current or savings account and a brokerage account, both financial institutions must support instant payment. For a consumer with a brokerage account, A2A payments can provide a significant advantage by immediately transferring funds from their current or savings account to their brokerage account.

What are instant A2A payments?

Instant A2A transfers boast rapid transaction speed compared to traditional A2A payments, which can take a few hours or even days to process. Instant A2A payments are usually made within seconds or minutes and are profitable for online purchases, bill payments, or even emergencies.

To achieve such swiftness, instant A2A transactions often rely on advanced technologies like Real-Time Gross Settlement (RTGS) systems that avoid intermediaries.

It’s important to note that the availability and specific features of instant A2A payments may differ depending on the region and the participating banks. Some countries have well-established RTGS systems that support instant payment, while others may be just implementing them.

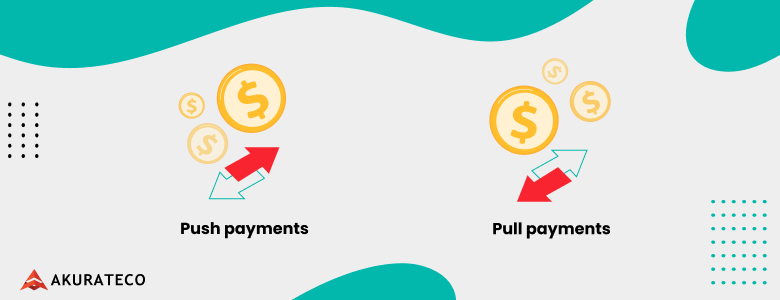

Types of A2A payments explained

A2A payments are conducted in two ways:

- Push payments (initiated by the sender, as in a normal purchase transaction).

- Pull payments (initiated by the recipient, requiring prior authorization by the sender). They are used for recurring subscription payments.

Understanding payment rails for A2A payments

Payment rails are responsible for transferring money between accounts. Think of them as hidden channels that make A2A payments work. Some of the most common ones include:

- Automated Clearing House (ACH) – is popular in the USA and deals with various types of transactions, including direct deposits, bill paying, and transfers between individuals.

- Single Euro Payments Area (SEPA) – is used in Europe and allows efficient cross-border transfers in euros, making paying more seamless.

- Electronic Funds Transfer (EFT) – covers the different electronic transfer systems used for A2A transfers worldwide.

Global examples of A2A payment rails

Below, we will navigate through A2A payment rails in various counties.

Pix

Pix was initiated by the Brazilian central bank in late 2020 and quickly gained fame as one of the most used tools for money transfers and purchasing. Its key powers are mostly free transactions with instant settlements. From the 2021 to 2022 period, the number of P2B transactions in the Pix system increased to 472 billion.

The latest Pix statistics from Marcel van Oost illustrate Pix volume surges towards other transactions.

iDEAL

In the Netherlands, iDEAL provides 65% of e-commerce pay. The system’s popularity has grown since the introduction of SEPA Credit Transfers (SCT) in 2019. iDEAL attained a market share of 72% by the end of 2022, offering the possibility of real-time payments.

SPEI

The paying system in Mexico is Sistema de Pagos Electrónicos Interbancarios (SPEI), owned and managed by Mexico’s central bank, Banco de México. Despite the country’s growing young population, of which 80% is considered urban, many people are still dependent on cash. This is associated with corruption and fraud. That is why Banco de México makes everything possible for people to abandon cash transactions. After several years of testing and a pilot project, they have finally launched large-scale retail payments with QR codes.

UPI

Unified Payment Interface (UPI) was launched in 2016 in India together with the National Payments Council of India (NPCI) and the Reserve Bank of India (RBI). The success of UPI is primarily due to its full match with widespread digital wallets – UPI payments are available both online and via QR codes. This helped to increase the share of digital wallets in Indian e-commerce to a remarkable 50% back in 2022.

Other examples of A2A payment rails

Thanks to the Yape and PLIN boom in Peru, the share of Account-to-Account transfers in the Peruvian e-commerce market has grown from 9% in 2021 to 17% in 2022. Known as private banking systems, they are projected to surpass 28% in 2026.

In Thailand, PromptPay is considered a key element of the government’s initiative to transform the country’s finance sector and has contributed to instant Account-to-Account payments. It has become the leading online payment method in the country, accounting for 42% of local e-commerce transactions as of 2022.

The BLIK paying system was established in 2015 in Poland and is now supported by 18 Polish banks, with 13 million users reaching every month. In 2021, 70% of transactions in Polish e-commerce were made with BLIK.

CoDi, short for Plataforma de Cobros Digitales, is a QR code used to pay for goods. It is generated by point-of-sale systems and directly links the QR drawing to the SPEI to utilize its real-time paying functions.

The largest paying platform in Germany using A2A is Giropay, which is based on an online interbank system for instant payments and transfers within the country. It is noted that Giropay previously handled 16% of all online transactions in the country.

In 2018, the Reserve Bank of Australia founded the New Payment Platform (NPP) – the most innovative paying infrastructure in the country. The impact of NPP on user-paying behavior in Australia has been significant. Customers use the scheme at least once a week, and real-time paying volume has grown by over 130%.

The advantages of A2A payments

A2A transactions offer advantages for both merchants and their customers. Here are a few reasons why they are earning popularity so quickly:

Accessibility

A2A payment systems can be used by anyone who has a bank account. Consumers don’t have to apply for a card based on their credit history, put up collateral, or pay upfront fees.

Lower costs

Credit and debit card transactions usually come with fees that are covered by the merchant. They generally pass these costs on to the consumer in the form of higher prices. A2A payments avoid such fees. Since they are direct transfers and not consumer loans, the customer never pays interest or late fees. For those interested in how to start a payment processing company, integrating A2A payment solutions can be an efficient way to minimize transaction fees and offer a cost-effective service to merchants.

Instant settlements

Sometimes, credit card payments and typical Automated Clearing House (ACH) transactions take a few days for funds to reach the merchant’s account. On the contrary, A2A payments are instant and utilize the Real-Time-Payment (RTP) system along with other fast-paying channels to transfer money without delay, even on holidays.

Increased sales

Customers who favor A2A payment systems are more likely to shop and spend with merchants that accept these payments.

Improved security

In the EU and other markets with a modern regulatory framework for paying, A2A typically requires strong customer authentication protocols and other security features. This significantly reduces fraud compared to paying cards, which often require third-party security solutions to be considered secure.

Potential drawbacks of A2A payments

One of the main drawbacks of A2A transfers is the need for payment processors to fully integrate them into their current portfolios and incorporate additional features to meet the standards of established payment methods.

In addition, consumers are increasingly demanding instant payment, greatly complicating the limitations of SEPA’s instant credit transfer, which will be largely overcome by the Instant Payments Regulation.

The main challenges for merchants are the multitude of existing A2A payment schemes and their lack of interoperability. Each scheme requires separate integration. Dispute resolution procedures vary widely or are nonexistent, creating confusion and adding complexity. Poor implementation of A2A transfers can degrade the user experience.

Other problems include difficulties in matching funds and the need to engage a new paying provider if the wrong strategic choice is made.

The impact of open banking on A2A payments

Open banking has turned A2A payments into more user-friendly technology. In the past, users needed to log into their bank accounts every time to pay. Repetitive paying requires filling out a long authorization form. In addition, there was no single system for initiating subscription paying, so the user experience was very different each time someone wanted to make a new subscription.

Overall, for a long time, A2A payments didn’t have any striking advantages that could beat bank card transactions, so companies had to tap into expensive card network schemes. However, open banking has completely changed the landscape, and A2A payments now offer far more benefits than ever before.

Challenges to A2A payment adoption

While the adoption of open banking is paving the way for A2A systems in many regions, the regulatory landscape is far from perfect. Every country has its level of openness and uses different rules governing financial transactions. For example, the European Union’s Second Payment Services Directive (PSD2) obliges banks to provide API access to third-party providers, which has promoted the development of A2A payment solutions. However, other regions, such as the US, have yet to implement comprehensive regulation that stimulates open banking to the same extent. This inconsistency creates barriers to the global adoption of A2A payments.

While A2A transfers are generally evaluated as secure due to strong customer authentication protocols, no system is resistant to fraud. As A2A payments become more popular, cybercriminals are now developing more sophisticated methods to exploit potential vulnerabilities.

For example, this goes to phishing attacks, where fraudsters trick users into providing their bank details. What’s more, since A2A systems often involve third-party providers, you need to ensure their adherence to robust security standards. Continued investment in security measures, fraud detection technology, and user education is a must-have to maintain the integrity of A2A payments.

Consumer behavior is another important aspect influencing the success of A2A transactions. While younger generations and tech-savvy consumers may readily adopt new payment methods, others may hesitate to abandon familiar credit card and cash transactions. Increasing consumer awareness and confidence in A2A payments is also critical to their widespread adoption.

What’s next? The future of A2A payments

According to the Global Payments Report 2023, A2A payments are projected to grow 13% by 2026, bringing the global e-commerce market to nearly $850 billion. By 2028, A2A transfers internationally will account for 17% of all e-commerce transactions by volume. A2A is currently most prevalent in smaller European countries and emerging economies, with a regional comparison of A2A transfers showing that in Latin America, applications that enable A2A payments are the focus, while Europe and Asia-Pacific focus on wire transfers or direct debit solutions.

In mature consumer markets with a deeply entrenched card culture, such as Canada, Japan, the US, and the UK, A2A has less impact as these markets have payment systems that foster consumer loyalty through successful card rewards programs.

Countries such as Australia, Mexico, the Netherlands, and Sweden have already developed regional A2A systems that have been widely adopted.

Discover A2A payments with Akurateco

Want to enhance your financial ecosystem with A2A payments? Akurateco’s payment orchestration platform serves as a connectivity tool for online merchants. By simply connecting our clients to A2A payment systems, we provide them with fast and secure access to cooperate.

Furthermore, Akurateco offers more than 370 payment methods and providers, including A2A payments and other Alternative Payment Methods (APMs), and develops new integrations on your request. As part of our integrations with various payment service providers, we also support the Pix, IDEAL, UPI, and other methods for your maximum convenience. Drop a line to our team if you want to explore more cutting-edge solutions and additional features for your business.

FAQ

What is an A2A payment?

Account-to-Account payments mean direct bank transfers between buyers and sellers in the absence of intermediaries or additional paying instruments such as cards, for example.

How do A2A payments differ from traditional payment methods?

Unlike traditional methods that involve intermediaries like banks or payment processors, A2A payments allow for direct transfers between bank accounts. This means funds can be settled much faster, often instantly or within a short period, reducing waiting times.

How quickly are A2A payments processed?

In most countries, account-to-account transfer can reach the merchant instantly, as they do not need to go through unnecessary intermediaries such as bank card networks.

What industries benefit the most from A2A payments?

Online retailers, gig economy platforms, and businesses involved in cross-border transactions can streamline processes, reduce costs, and improve customer satisfaction with A2A payments.