- What is Payment Infrastructure?

- Payment System Infrastructure: Key Components

- Current State of Payments Infrastructure

- Legacy and Modern Payment Infrastructure Difference

- Five benefits of modernizing your payment infrastructure

- Modernizing payment infrastructure: Build VS Lease

- Key Payment Infrastructure Trends in 2025

- Conclusion

- FAQ

Today, the global payment system infrastructure has become, without exaggeration, the cornerstone of the digital economy. Consumers want faster, safer, and more seamless payments, so the need for reliable and adaptive digital payment infrastructures is growing like never before.

The legacy payment infrastructure, which was once effective, simply cannot cope with what users and businesses expect. The main request today is practical, understandable, and scalable integration. And here, for example, cloud technologies and artificial intelligence come to the rescue, providing tools and capabilities to enhance your own products, making them more adaptive to various requests and budgets.

In this article, we will examine the current state of payment infrastructures, consider the industry’s key trends, highlight the problems, and demonstrate how Akurateco’s payment solutions allow companies to stay ahead.

What is Payment Infrastructure?

Let’s start from the beginning. Payment infrastructure is an integrated network of technologies, systems, and processes that enable modern financial transactions. It includes payment gateways, processors, and communications networks facilitating electronic payment methods like credit cards, e-wallets, and bank transfers.

Smooth and secure payment processing is key to ensuring a positive customer experience, maintaining trust and cash flow, and delivering operational efficiency. A reliable payment system requires fast transactions, minimal fraud risks, and the smooth flow of commerce that businesses need to survive in the digital economy. Today, it is slowly transferring into payments infrastructure as a service, allowing businesses to easily integrate and scale payment solutions without requiring extensive in-house development or maintenance. This shift is driving greater efficiency, flexibility, and innovation in processing payments across industries.

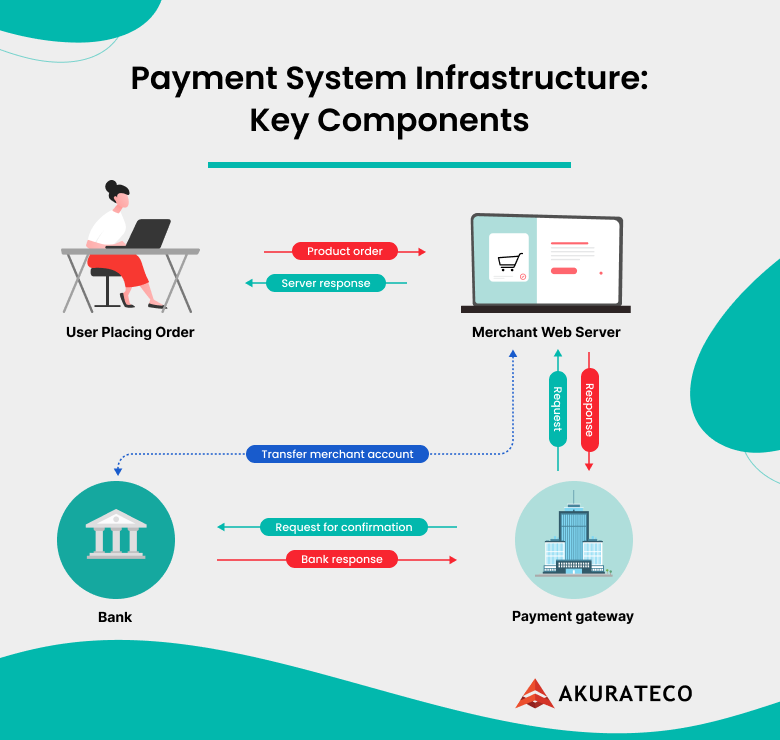

Payment System Infrastructure: Key Components

The components of a payment infrastructure include several integrated systems and processes whose primary purpose is to ensure secure and efficient transaction operations.

When talking about key components, the following should be mentioned:

- Payment Gateway bridges merchants and payment processors, ensuring secure data transfer.

- Payment Processor processes transaction data by transferring information between the merchant’s bank (the acquiring bank) and the customer’s (the issuing bank).

- The issuing bank is the financial institution that issues consumers with payment cards (credit, debit, or prepaid).

- The acquiring bank, e.g., the bank receiving the payment, receives transaction requests through the payment gateway and forwards them to the appropriate networks for processing.

- Payment networks, such as Visa, Mastercard, and American Express, greatly facilitate communication between acquiring and issuing banks, handle transaction routing, authorization, and settlement, and ensure compliance with security standards.

- The settlement system ensures funds transfer from the customer’s account to the merchant’s account, including clearing processes.

- Fraud detection and risk management tools refer to monitoring transactions for suspicious activity and ensuring compliance with regulations such as PCI DSS (Payment Card Industry Data Security Standard ).

- Digital wallets and alternative payment methods are integral to payment infrastructures, offering users a seamless experience and a variety of payment options.

- APIs (application programming interface) and integration layers are the level at which developers can integrate payment functionality into their applications or websites, allowing them to customize and scale as needed.

- Compliance and security components primarily concern PSD2 (Payment Services Directive 2) in Europe and compliance with KYC/AML (Know Your Customer/Anti-Money Laundering) policies, which are essential to maintaining the legality and security of transactions.

- Reporting and analytics provide merchants with information on transaction history, consumer behavior, and performance metrics, all of which help in decision-making and strategy formulation.

Current State of Payments Infrastructure

The global digital payments market is projected to reach $159 billion by 2025, up from $88 billion in 2023.

There is a strong argument for such a substantial jump:

- Expansion of e-commerce: there is fantastic growth here, so by 2025, global e-commerce sales are expected to reach $7.5 trillion.

- Growing adoption of digital wallets: More and more users want to have them. By the end of 2023, there were more than 4 billion digital wallet users. In 2025, with a CAGR of 16%, the number of digital wallet users is projected to be around 5.38 billion.

- Real-Time Payments (RTP): Over 360 Billion RTP Transactions Expected by 2025.

The digital payments market is booming, with e-commerce, digital wallets, and real-time payments driving unprecedented growth. Now is the perfect time to capitalize on this momentum and seize market opportunities before they pass.

Legacy and Modern Payment Infrastructure Difference

Choosing between legacy and modern payment infrastructure requires understanding the strengths and limitations of each. Let’s look at legacy and modern payment infrastructure. Understanding the differences between legacy and modern payment software is important for companies that want to future-proof their payment processes while maintaining business continuity.

Transitioning to more modern solutions can often be painful for businesses, as it entails changes at all levels. Although reliable and familiar to most businesses, legacy payment infrastructure often simply cannot meet the demands of the modern digital economy. Its main advantage is stability. Widespread adoption and a level of well-earned trust are equally valued. But the inability to scale quickly and efficiently, low processing speeds, and problems with integrating new payment methods make it inapplicable to today’s realities.

When discussing modern payment infrastructure, it is important to note its advantage immediately – it is designed for flexibility and innovation. Users have access to real-time processing, seamless integration with various platforms, and improved security features. Among the challenging things for businesses, high initial costs, complex migrations, and fairly complex training for teams are often noted here.

Understanding the trade-offs between these two approaches is important for companies that want to future-proof their payment processes while maintaining business continuity.

Five benefits of modernizing your payment infrastructure

Payment system infrastructure constantly evolves and modernizes, providing specific advantages to businesses. The user continually wants more, which is a challenge even for progressive payment organizations. Most companies are trying to modernize their payment infrastructures to be competitive and adaptive. Let’s take a closer look at what the use of more advanced technologies in the infrastructure, such as cloud solutions or AI (Artificial intellect) integrations, provides.

1. Efficient and easy scaling

Business needs can change dramatically, and you need to be able to adjust quickly to stay on top. Clouds allow you to scale up, if necessary, speedily and even automatically adjust capacity when the volume of payments changes. In addition, automation in cloud platforms and the ability to choose an infrastructure provider can reduce the cost of hosting, providing the necessary capacity to support growing payment volumes.

2. Real-time payment implementation

Implementing clearing and settlement tools in real time allows you to process payments almost instantly, which is already becoming the new norm. That is why the parallel throughput supporting real-time service is in demand today. The increased processing speed also reduces mistakes with immediate feedback when initiating a payment, creating a competitive differentiator between organizations that have invested and those that have not.

3. Rapid adaptation to new standards

Adopt new standards and comply with necessary requirements for payment organizations. These standards are changing pretty often, and if your infrastructure needs to be updated, then integrating new requirements will be really difficult or even impossible.

4. Improved financial crime prevention

The rapid growth of digital payments brings new challenges for payment organizations, particularly in meeting compliance requirements. Any change in standards or improvement in infrastructure can lead to new security issues. Therefore, combining cloud rules with the data available in ISO 20022 (ISO 20022 is a multi-part International Standard prepared by ISO Technical Committee TC68 Financial Services) can help organizations better identify potentially problematic payment transactions. These rules can also be processed efficiently using AI and ML (Machine Learning) to detect financial crimes better and reduce false positives (cases where legitimate transactions are mistakenly flagged as suspicious).

5. Optimizing Operational Efficiency

Automation in cloud-based payment platforms streamlines routine maintenance tasks, such as system monitoring, software updates, and troubleshooting. This reduces manual workload and minimizes downtime, ensuring consistent system availability. Additionally, automation tools provide actionable insights into payment performance and infrastructure efficiency, enabling businesses to make data-driven improvements and quickly identify bottlenecks or errors. Companies can enhance their competitiveness and foster growth by focusing resources on strategic innovations rather than repetitive maintenance.

Modernizing payment infrastructure: Build VS Lease

A business looking to improve its payment system always faces a key question: should it develop infrastructure from scratch or rent a ready-made solution? Each approach has advantages and limitations, which depend on the company’s goals, budget, and scale of operations.

Building your own infrastructure provides complete control over the system, allowing you to implement unique features and adapt to the business’s specific needs. However, this requires a significant investment of time and resources, as well as expertise in technology and security.

Renting a ready-made solution, on the contrary, allows you to enter the market with speed, minimizing development and maintenance costs. Such solutions often offer built-in features to meet security and regulatory requirements. However, the company may face limitations in flexibility and dependency on the supplier.

Key Payment Infrastructure Trends in 2025

At Akurateco, a trusted leader in payment solutions with over 20 years of experience in the industry, our founders have been at the forefront of shaping modern payment infrastructure. Drawing on this extensive expertise, we’ve identified several key trends that are set to define the payment landscape in the coming year.

With this foundation, let’s explore the critical shifts and innovations we anticipate in the industry for next year.

1. Rise of payment orchestration

Business globalization is driving demand for payment orchestration platforms. The best payment orchestration platforms 2026 simplify complex payment ecosystems by integrating multiple gateways and payment methods, optimizing payment acceptance rates. Akurateco is an example of this approach, with the platform offering easy integration of over 400 payment methods and providers’ payment providers to organize payments. This leads to higher transaction success rates and lower operating costs.

2. Real-time payment systems

Real-time payments are revolutionizing the way money moves around the world. We get instant transfers, improved user experience, and increased business liquidity. Next year, real-time payments will account for as much as 20% of global electronic transactions.

3. Advanced fraud prevention

The growth of digital payments is directly proportional to the threat of fraud. In our experience, AI-powered analytics for monitoring transactions, detecting anomalies, and minimizing chargebacks provide companies with peace of mind. This trend is growing in line with the modernization of payment system infrastructure, which is good news.

4. Crypto payment integration

Companies are increasingly integrating crypto payments into their systems to cater to tech-savvy consumers and expand their payment options. Cryptocurrencies offer a decentralized and secure transaction method, which appeals to users concerned about privacy and fraud prevention. Moreover, accepting crypto can open businesses to global markets by providing seamless cross-border transactions without the delays and fees often associated with traditional banking. This makes it a valuable solution for industries where speed, security, and customer trust are paramount. Additionally, adopting crypto payments positions businesses as innovative and forward-thinking, enhancing their appeal to a younger, digitally-focused demographic.

5. Cross-border payments

As payment systems evolve, cross-border payments are becoming increasingly efficient with the advent of advanced technologies such as blockchain and payment orchestration. These innovations are set to revolutionize the cross-border payment landscape, offering increased efficiency, reduced costs, and faster transaction times. Importantly, they also ensure regulatory compliance, providing a secure environment for international money transfers. By 2025, we expect a significant reduction in the cost and time of cross-border transactions due to these innovations in payment infrastructure and the growing integration of crypto payments.

Conclusion

Payment infrastructure is at the forefront of global economic growth. Continuous efforts to ensure smooth transactions are driving digital transformation to a large extent. Companies that invest in modern, scalable, and secure payment infrastructures will thrive and lead in an increasingly competitive market.

In our work, we take into account all the needs of not only businesses but also users to improve payment infrastructure in the right way. The platform simultaneously provides user comfort, allows you to simplify payment management, and has all the necessary analytical data.

If you are ready to modernize your payment infrastructure, Akurateco will be happy to take you to the future of payments. Book a meeting with our experts today and discover tailored solutions that drive results!

FAQ

What is a payment infrastructure?

A payment infrastructure is an underlying soft that refers to the systems and processes that enable the secure and efficient transfer of funds between parties. It includes a range of components, including payment gateways, processors, fraud detection systems, and compliance protocols. All of these are needed to support transactions across multiple platforms, currencies, and payment methods.

How to build a payment infrastructure?

It is a complex process that consists of a number of steps. Building a payment infrastructure involves:

- Assessing business needs: This is where you determine the volume, type of transactions, and regions that will be supported.

- Selecting payment infrastructure providers: Gateways and processors that meet your requirements.

- Integrating security measures: This is where you implement encryption, tokenization, and fraud detection tools to ensure compliance and security.

- Ensuring scalability: Designing the infrastructure to handle growing transaction volumes.

- Testing and deployment: It is imperative that you conduct extensive testing to ensure reliability before launch.

But you can save money and time by choosing the rent option.

How does the payment infrastructure work?

The payment system infrastructure facilitates the movement of funds between customers and businesses. Once a customer initiates a transaction, the payment gateway immediately encrypts and sends the payment data to the processor, which contacts the issuing and acquiring banks to verify and authorize the payment. Once approved, the funds are transferred and the customer and merchant are notified of the transaction status.